6 Things Your Bank Needs To Wrap Up PPP

After months of being in a steady-state, the PPP world caught fire. You have the borrowers from Round 1 (2020 origination) that have not filed for forgiveness yet and are now facing principal and interest payments; you have Round 2 Forgiveness heating up, and then, as of last week, you have the new SBA Direct Forgiveness Portal (Portal) that opened to great fanfare. With all this movement, the end is in sight, and banks need to start thinking about their PPP demobilization plan. Below, we break down five tactical moves to get in a position to wrap up this historic stimulus effort.

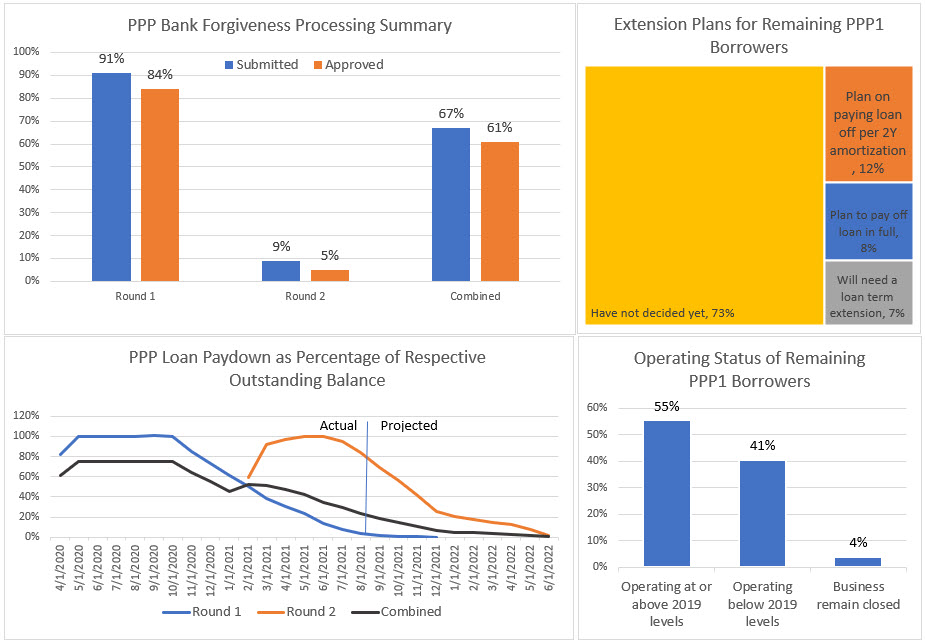

The Status of the PPP Effort

Below is data collected from a group of banks and PPP borrowers that can serve as a benchmark. The average bank has about 91% of forgiveness submitted from Round 1, with about 84% approved, and 9% submitted from Round 2 with 5% approved. On a combined basis, banks have about 61% of their total Round 1, and Round 2 outstanding balance processed and approved.

Looking at the bottom left chart below, given all the changes with PPP, including the Direct Portal, it is now estimated that most Round 1 balances will be processed and approved by year-end, while Round 2 forgiveness is accelerated compared to Round 1 and is extinguished mainly by mid-2022. Because of the lower cost of processing associated with the Portal, the higher approval rates for forgiveness, lower projected cost of funds, and the faster repayments, the return on assets for banks in the program has increased from approximately 2.4% to almost 2.7%.

6 Steps To Take To Wrap Up PPP

Step 1: Transition Borrowers to the SBA’s Direct Forgiveness Portal – Even if you already have PPP Forgiveness processing technology, the SBA’s Direct Portal is likely better. It has an array of expanded input validations built-in, saving a material amount of time error handling. Of course, the flagship improvement is the SBA’s new “Covid Revenue Reduction Score.” This score, developed in conjunction with Dun & Bradstreet, takes into account factors such as area production, foot traffic, credit card spending, employment trends, a business operation response index, and a variety of other factors. The Score determines if it is likely the PPP Round 2 borrower that received a loan for under $150,000 suffered a 25% reduction of revenue in 2020. In side-by-side testing, banks are finding that they can save approximately 20 minutes per application plus get a materially larger percentage of loans approved.

The net result of the Portal is that it is easier for the borrower, so more of them will file sooner and with a more enjoyable user experience. It was taking most banks and the SBA approximately ten days to approve PPP loans under $150,000, and now that time is reduced to about three days.

For banks, there are high costs and time savings by rechanneling PPP borrowers to the Portal. Banks can then free resources to provide better customer service to loans with problems and process borrowers with loans over $150,000.

Step 2: Increase Marketing – The Portal requires banks to update their website and send a series of emails to educate borrowers on the new process. In addition, a majority of borrowers that are eligible for forgiveness that has not filed yet are either too busy, not knowing how to file, or have been procrastinating filing for forgiveness. Instituting an email and digital add remarketing campaign can work wonders and speed up forgiveness filings by 20% or more.

Step 3: Process Term Extensions – Most banks originated the bulk of their PPP Round 1 loans with a two-year term. Now that deferment is ending, borrowers that cannot get approved for forgiveness may need help extending their loan term out from two years to five years. In a recent survey of PPP borrowers yet to be forgiven (above), 7% will need extensions, with 73% waiting on forgiveness outcomes to decide. Instead of waiting for delinquencies to occur, banks should be proactive and reach out in order to help with extensions. Many banks have created an automated or streamlined process using robotic process automation (RPA) or a platform with scripting capabilities such as Box, Salesforce, ServiceNow, or Docusign.

Step 4: Prepare To Manage Delinquencies and Claims – Approximately 4% of PPP borrowing businesses are closed and/or have already filed for bankruptcy. As the Forgiveness tide goes out, banks are going to be left with a concentration of borrowers that cannot pay, cannot achieve forgiveness, are no longer operating, and/or are fraudulent. Many banks have not taken steps to find out who these borrowers are, presenting an ever-mounting challenge as the deferment period on these loans ends. Since banks have a limited time to respond to maintain the sanctity of the SBA’s guarantee, banks should have a plan together now.

Step 5: Preparing for the End – Finally, banks need to start thinking about taking steps in creating a demobilization plan that includes how they are going to electronically store and index all the files and records associated with PPP. Banks need to make sure they document both their adverse action response and their Fair Lending support. Finally, banks are well-advised that if they have not done so already, to spend a couple of hours documenting the PPP origination and forgiveness “lessons learned” in an after action-style review in order to improve on their process for next time and to pass these lessons on to the next generation of bankers. PPP was such a success that you can bet a similar program will be used in the future.

Step 6: Provide Permanent Capital – 41% of PPP borrowers are still operating below 2019 levels, with many of those in need of permanent, longer-term capital. Banks should consider a plan to extend conventional loans to those small businesses that qualify, help them get an SBA loan under the enhanced 7(a) Program, or provide an alternative lending source.

Putting This Into Action

The PPP has been one of the Government’s and banking’s most outstanding achievements. Never before has so much debt been distributed and repaid so fast. Finishing strong is a hallmark of banking, and PPP should be no exception. Now is the time to use the slower month of August to plan and start to execute wrapping PPP up in an orderly and efficient manner. With strategic planning, budget season, and what is shaping up to be a busy fourth quarter just around the corner, now is the time to lay the groundwork to put PPP to bed.