An Early Warning For Bank Multifamily Rent Trends

One of the most underappreciated commercial real estate trends in banking is the remarkable stability of multifamily rents during this pandemic. As of last week, according to the National Multifamily Housing Council (NMHC), 77.4% of renters in an 11.4 million sample size of professionally managed apartment complexes were making their rent payment which compares to 79.7% during the same time as last year and an average of about 82% for the year (summer delinquencies are usually higher). In this article, we explore recent rent-paying trends and discuss what could happen at the end of the month when the CARESAct stimulus payments run out.

![]()

![]()

What is happening with Collections

Collections have been largely on par adjusted for seasonality and the holiday weekend. That said, there are some regional differences with some stress starting to show up in California (mostly Southern), Southern Florida, Las Vegas, and the Northeast. Offsetting that was a little better than average collection performance in Georgia, Alabama, Texas, and Colorado.

One aspect that is interesting in this analysis is the Northeast performance, New York, in particular. After a bad April, New York came back strong in June to slightly above average only to trail off sharply for the first part of July. While this might be an aberration, New York is usually on the leading edge of rent trends so this could be our first harbinger of concern.

Another interesting aspect is the performance of “C-class” assets, which are lagging more than average. This is also another potential leading indicator of stress.

Other Areas of Concern – Income Level

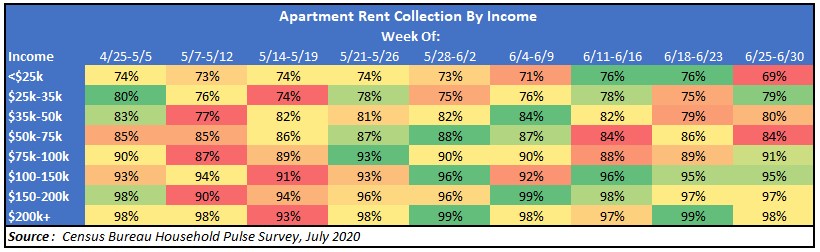

For banks looking to increase monitoring and risk management for the multifamily credit portfolio, there are some additional trends by income that stand out at the end of June. A recent (and new survey), the Household Pulse Survey by the Census Bureau, points out a focus area for banks. The survey question is “Did you pay your last month’s rent or mortgage on time?” with response options of “Yes,” “No,” or “Payment was Deferred.” Here, households that make under $25k per year and households that make between $35k and $75k are most at risk of not making rental payments. This collection rate is not surprising given the amount of pandemic-related job loss concentrated in lower-wage service jobs like those in the leisure and hospitality sector.

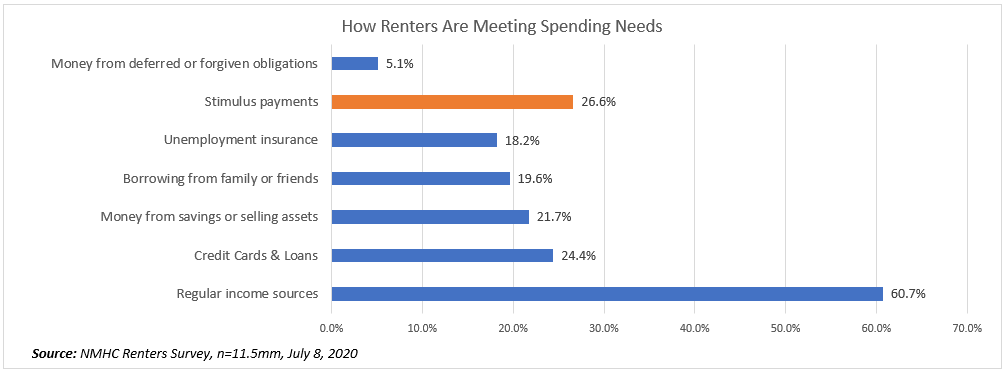

Further data (below) supports the fact that the CARES Act’s unemployment benefit of $600 per week, combined with the standard state unemployment benefits has helped and could help to keep rent collection rates from deteriorating further. This federal benefit is set to expire at the end of this month.

Last week, Treasury Secretary Mnuchin stated that any extension of this benefit could be assumed to be capped at 100% of pre-COVID-19 workers’ pay. The current total unemployment benefit more than replaced lower-income unemployed workers’ pay. Without an extension of this benefit, there is a risk for the large number of unemployed workers to lose substantial income and can potentially lead to a significant deterioration in rent collection rates, likely among lower-income households.

Source: NMHC (National Multifamily Housing Council) Rent Payment Tracker

Other Areas of Concern – Property Size

Because managing payment deferments, electronic lockbox, payment collections, sales, and property management require a certain level of technology during a pandemic, and it is no surprise that larger complexes, those over 100 units have performed relatively better than those under 100 units, particularly those below 50 units. Larger multifamily complexes tend to have either more sophisticated property management, which appears to be excelling by about five percentage points better than smaller units that tend to be managed by smaller firms.

Putting This Data into Action

The data shows that August may be a cause for concern, and banks should consider placing more credit resources around monitoring multifamily performance. Up to this point, the asset class has performed better than expected. Going forward, without stimulus and with another wave of pandemic infections, delinquencies are expected to increase by more than 10% in the third quarter. Banks would do well to focus their credit resources first on higher leveraged properties, then on C-class properties with lower income tenants (and higher leverage) and then on smaller buildings under 50 units.

Another area of concern to monitor is the reported trend of shorter lease periods. While this is more an anecdotal by us, as we talk to property managers throughout the Southwest and West Coast, more managers are reporting tenants that have had maturity extensions during the past three months, are opting to go month-to-month instead of renewing their lease agreement for a year or more.

Finally, there is another interesting aspect of these times that have not been discussed widely but merits an action plan. In many cases, management companies are unable to evict delinquent rent payers. How banks handle, this was heretofore a credit decision. Now, banks also have a moral and ethical position to take.

Assuming banks come down on the position that further leniency will be granted to their multifamily borrowers that could soon have 20% delinquencies and can no longer meet their mortgage obligations, there is one more aspect to consider. Exacerbated by the political climate, the social unrest, and the economic environment, there is a growing percentage of renters with nuisance complaints filed. Due to local ordinances preventing evictions, property managers are having a hard time removing those tenants with for non-economic violations, which in turn makes current paying renters choosing to relocate. While no survey tracks this, we hear this anecdotal evidence consistently among property managers and alert banks to monitor.