An Update to Our CRE Credit Portfolio Forecast

In past articles, we discussed a proposed Coronavirus stress test under CCAR and provided our COVID-19 probabilities of default and loss given defaults for a model bank portfolio. In this article, we update our CRE modeling and take a deeper dive into loan-level analysis in order to help banks triage and manage both individual credits and their portfolio-level reserves. Since we are in unchartered territory, this is just one of many updates that we expect to publish, so be sure to stay tuned.

Updated Cash Flow Modeling Shocks

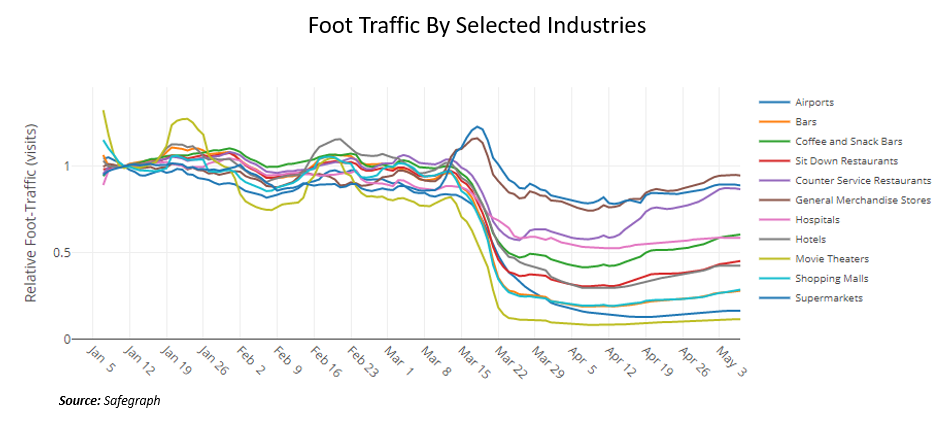

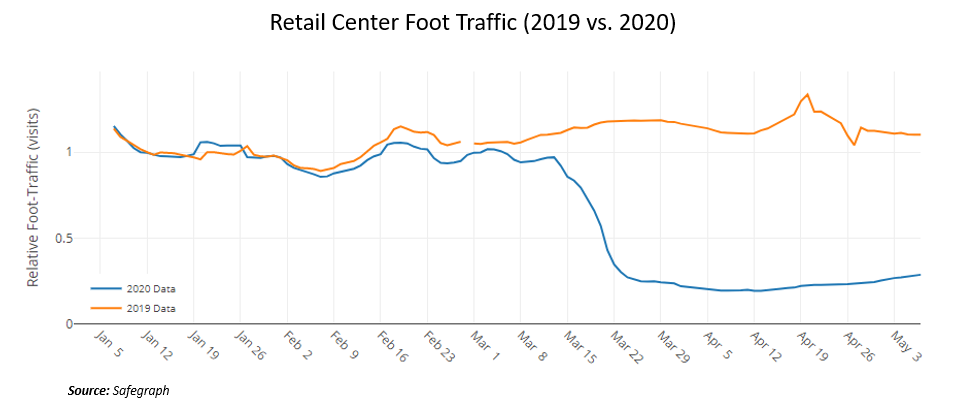

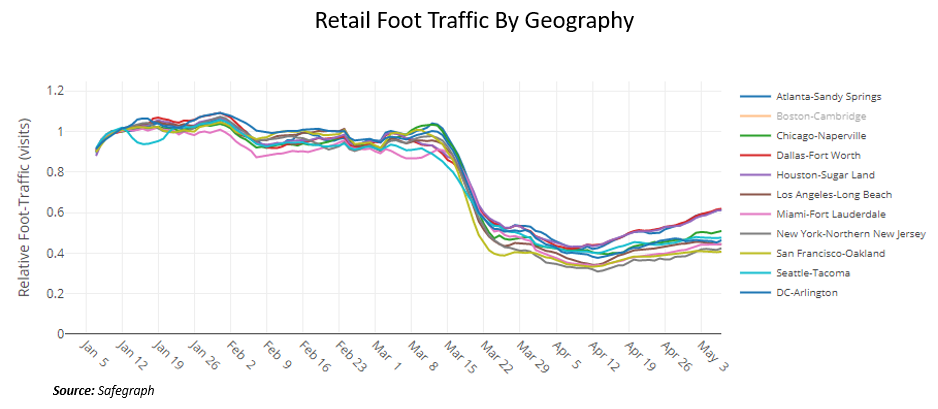

Given that the reopening of America is happening sooner than we originally expected and we initially assumed that we would have an effective COVID-19 serological test by June, which appears to also be delayed, we have increased the impact on commercial real estate net operating income modeling. We have increased our unemployment levels, the most significant driver of credit from 20% to 25% unemployment in the second quarter, and have incorporated foot traffic correlations on both a property-type and geographic-specific basis (below).

Severe cash flow shocks to property sectors most vulnerable to the COVID-19 pandemic include a 65% cash flow decline for hospitality, a 45% decline for retail, and a 20% decline for multifamily. While originally we had hoped that government properties were unchanged, we have increased the probability of default slightly on that sector composed of largely office properties. Our one-year probabilities of defaults for self-storage, industrial, and manufactured housing from our original forecast remain unchanged.

The Impact to Probabilities of Default

The result of a greater loss of net operating income (NOI) results in a higher sensitivity to default probabilities. Loans that exhibit a shocked debt service coverage ratio (DSCR) of 0.95 times and below rocket to a 75% probability of default (POD). If you reverse engineer what this means, banks want to prioritize loans that had under a 2.81x for hospitality, 1.80x for retail, and 1.25x for multifamily before March of this year for additional review.

Revisions to the Loss Given Default Model

While our forecast for the average loss given default (LGD) of a bank’s CRE portfolio moves from 30.1% to 47.6% by 2020 year-end, we received many questions on what that means for incremental and gross projected capitalization rates. This would mean that cap rates increase another 25% for hospitality, 20% for retail, 15% for multifamily, 6% for office, and remain unchanged for industrial. This would result in gross projected cap rates at year-end of: 13% for hospitality, 11% for retail, 9% for multifamily, and 7.5% for office.

Further, since our last analysis, we had time to get more granular in bank portfolios and now identify single-tenant, tenants in industries most impacted by COVID-19 and shared space office tenants more likely to default and with a higher cap rate.

Revisions Down to Multifamily

We have also had time to further monitor the pandemic’s impact on the multifamily subsector. Because of the high correlation of multifamily performance with employment, and the unemployment picture is slightly worse for 2Q than we originally expected (which was a 22% unemployment rate which we now believe will exceed 25%), we have reduced multifamily projections accordingly.

As we get more granular, hit particularly hard and driving up the average POD are student-related multifamily and senior long-term care facilities.

As such, where we previously assumed a 10% reduction in multifamily cash flows, we now believe this will approach 15% to 20% by year-end.

Municipal Occupied Properties

In addition to getting more granular for specific commercial property types, we have also started to focus on lease construction. Based on the decline of GDP and unemployment, and taking into account additional stimulus, we increase our probability of default forecast from a pre-COVID-era 0.09% for majority gov’t tenant office and industrial to an expected default rate of 0.65%.

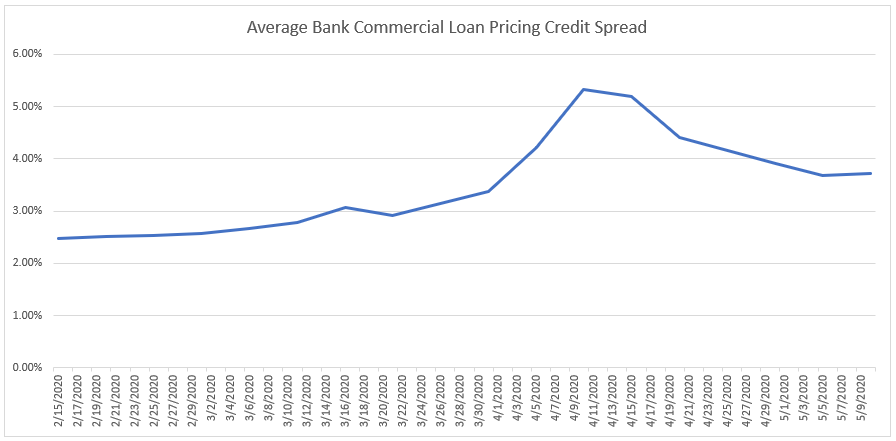

Loan Pricing

Since we last published, another major shift in the bank CRE loan market has been loan pricing. Loan pricing has since tightened, for an unknown reason, as most every loss model we have reviewed has only increased since mid-April. While interest rates have remained surprisingly stable, credit spreads have decreased from a high of 5.32% to 3.73%.

Up Next

Moving forward, we look to model a variety of different scenarios to apply to various industries and borrowers on a loan-level basis. We also look to take our stress test out from 2021 to 2024 in order to have a better view of future liquidation activity.

We also look to get more granular on specific bank vintages as preliminary data indicates loans originated in 2018, appear particularly vulnerable in most parts of the country due to its peak in value. We are also in the process of incorporating additional models from Trepp, Costar, Experian, and others as a way to triangulate our forecasts.

Finally, we are hopeful that we can find more data and experience around how the interplay of forbearance, stimulus, and a positive NOI response plays out. Will having a six-month forbearance end up in a lower probability of default than we forecast, or will it be the same with a higher LGD as cap rates trend sharply up?

It is scary to realize that at present, current bank property-level stress test models indicate banks will need to liquidate almost 20% of their CRE portfolio in 2021 and 2022. We can only hope our models are wrong on this.

Of course, as we have mentioned before, the above data are only estimates, just for a commercial real estate portfolio, and computed for an aggregate bank. Our assumptions might be off, and this may not pertain to your bank, but at least this gives you an updated view informing the allocation of your time according to the largest risk, instead of the largest credits.