What Is The Probability of a Bank Acquisition?

If you are a bank CEO, you already track performance and risk for regulators, the board, and shareholders. There is another audience you cannot ignore: potential acquirers. Banks that get acquired often share common traits. Some of these traits are quantitative and some are qualitative. The good news is that we can help you identify what to fix, so your bank is positioned to stay independent.

Why Banks Become Targets

When it comes to acquisitions, acquirers often look for a certain bank profile that fits their operation. While there is the intangible of culture that is often a major factor and one that we will not be able to quantify, there are a variety of other aspects that can be quantified. For instance:

- “Clean Operations”: While there are acquirers that like a story for a price, most like a clean, understandable bank with few surprises. The less esoteric business lines that must be explained, the wider the appeal of the bank.

- Core Deposit Performance: Every bank needs better performing deposits. The better your deposit performance, the more attractive you are the higher price you can command. Loan quality is often in the eye of the beholder, but deposit quality is universally known.

- Excess Capital or Balance-sheet Flexibility: Excess capital or liquidity that is underutilized screams to find a better home.

- Attractive Markets: Geographies or market segments that are attractive means that your bank is attractive. Sometimes this is just being at the right place and at the right time and other times banks can intentionally build value to protect themselves through higher performance or drive a higher price.

- Technology: The lack of technology or operational investment hurts performance and is attractive to banks that want to move your assets and liabilities over to their, more efficient, platform.

- Shareholder Base: If you are a closely held, family-owned bank, chances are you will be sold when the family is good and ready. This could be tomorrow, but it could be never. However, the more public you are, the more “you are for sale every day,” as our former chairman used to say.

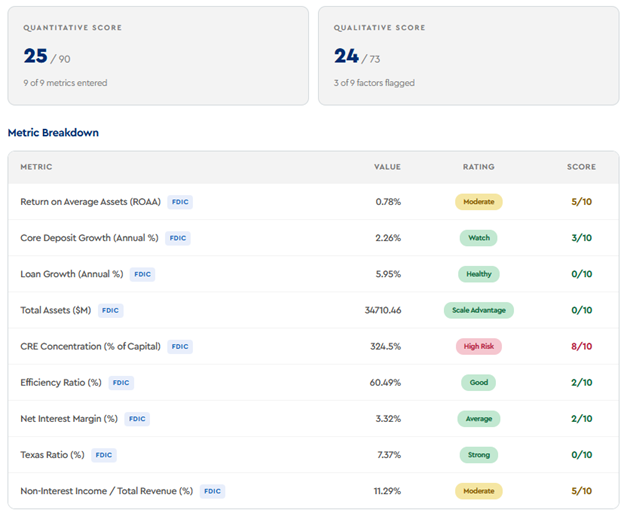

What Our “Look Up Your Bank” Risk Assessment Reveals

We created an “Acquisition Risk Assessment” tool where you can pull down your bank (or any bank) and it will load current FDIC data. We then score the bank using that data plus as a series of quick qualitative questions. We compare your results against current benchmarks from other banks and provide an assessment of the probability of being acquired.

The output is not a crystal ball, but it is a fast way to see where you stand versus peers, what looks strong, and what might invite a buyer to believe the deal is easy.

Making Your Bank Less Of A Target

When it comes to acquisitions, acquirers often look for a certain bank profile that fits their operation.

- Clarify Your Independence Story: Make your strategic plan and capital plan distinct from the competition. Acquirers look for uncertainty they can “solve.” By generating franchise value through strategy and execution, a bank generally makes itself too expensive to acquire.

- Reduce Funding Fragility: Stress test deposit betas and runoff assumptions, diversify larger relationships, and actively manage brokered and wholesale reliance so your funding profile cannot be quickly labeled as “fixable.” Increase product design and marketing to boost treasury management and DDAs.

- Eliminate Avoidable Concentrations: Review credit concentrations (by industry, geography, sponsor, and borrower type) and document the limits and monitoring that keep them within appetite.

- Increase Earnings Stability: Identify volatile parts of the balance sheet, non-core revenue dependencies, or unusually high expenses that make your earnings look like a simple efficiency play for a buyer, then address them on your terms. Monitor interest rate risk closely in both your loan and investment portfolio. Leverage artificial intelligence and agentic AI where possible to improve operating leverage.

- Make Capital Intentional: If you are carrying excess capital, articulate publicly why (growth runway, stress resilience, future shareholder actions) and how you will deploy it, rather than leaving it to be interpreted as “unused capacity.”

- Improve The Customer Experience and Engagement: It is underappreciated how important having a customer base that loves the bank truly is. The more you find ways to add value to your customers’ lives, the more they will reward you with more business. This means everything from having digital account opening, automated loan origination and a group of experienced bankers that can act as trusted advisors.

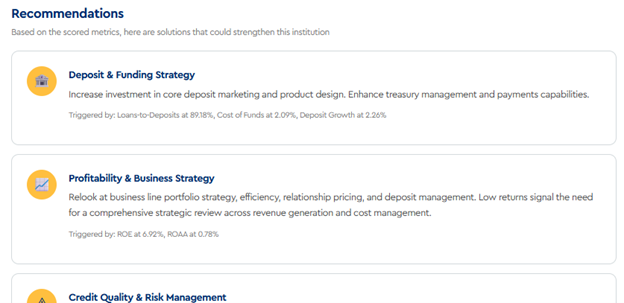

Our assessment also provides a set of recommendations customized for your bank.

Putting This Into Action

If you are interested to see the position of your bank through an M&A lens, look up your bank, analyze the results, do your own critical analysis, and then create a plan on how you can improve performance to prevent your bank from being an easy acquisition target.

It’s a barbell-shaped world out there when it comes to M&A. Banks that outperform and underperform get the primary attention. The difference is that management teams that outperform at least control their own destiny.

Click HERE to use the free Acquisition Risk Assessment Tool.

Disclaimer: This article, and the assessment tool, is for informational purposes only and is not M&A, legal, or investment advice. We focus on bank performance. If you need M&A advice, call an investment banker. Consult appropriate advisors when evaluating any sale or purchase transaction or strategic decision.