Growing Fee Income For Performance

In our previous article (HERE), we explained that fee income (not net interest margin, asset size, or nine other variables) has the highest correlation to community bank performance as measured by both return on assets and equity. Growing fee income is one of the most critical investments you can make. Why? We believe that this correlation between non-interest income and ROA is explained by five main factors, as follows:

- Fee income is a direct contribution to the bottom line that typically does not require additional assets. In this article we will also highlight the highest potential sources of fee income on a community bank’s balance sheet.

- Higher fee income is also an indication of a bank’s ability to service high-net-worth customers.

- Fee income is an example of a profitable cross-sell opportunity available to all community banks.

- ROA/ROE is even higher where fee income can be recognized upfront and not amortized over the life of the relationship.

- In a competitive commercial loan environment, fee income is more accretive to ROA because in many instances it is not directly paid by customers out-of-pocket – more on this below.

In this article we will further analyze the inherent advantages that community banks have in growing fee income. We will discuss why community banks do not need to buy new lines of businesses or hire additional personnel to increase fee income. We will also highlight an obvious source of fee income available to all community banks.

Industry Comparison

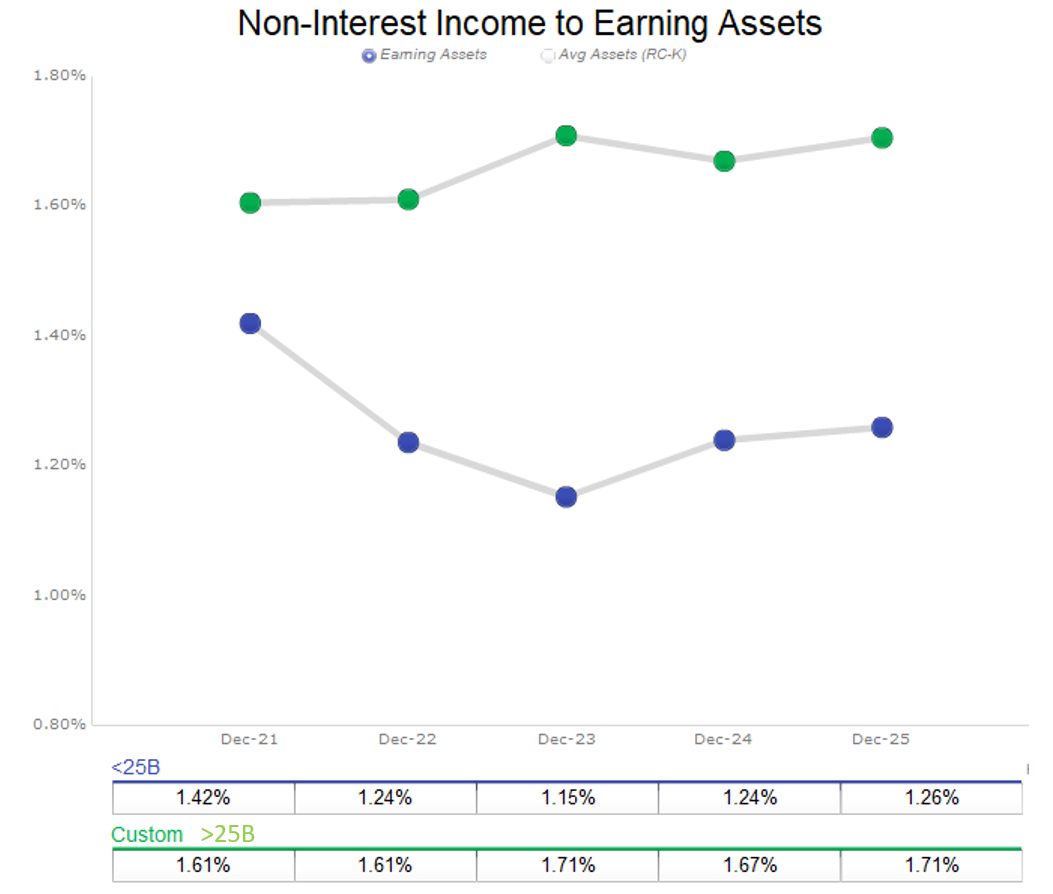

Community banks generate higher NIM than non-community banks (as of the end of 2025, 3.80% NIM for community banks vs. 3.39% for non-community banks). However, non-interest income is highly skewed to the advantage of non-community banks (see graph below).

Banks over $25Bn have historically generated higher fee income and this divergence has become more pronounced with the cessation of PPP loans after 2021. On average, the regional and national banks generate about 36% more fee income as a percentage of total revenue. We compared service charges on deposits, gains on assets, insurance fees, securitization fees, and servicing fees, and for all these reported lines of business the fee income was similar. There are two lines of business where the larger banks are outperforming community banks for fee income: investment banking, brokerage and underwriting, and loan fee income. While community banks are unlikely to invest in advisory, brokerage and underwriting businesses, the ability to generate additional loan fee income is feasible.

Some national banks favor fee income from loan fees, and we believe that much of that difference stems from hedging programs. For example, in any given year JP Morgan’s community banking total fee revenue comprises on average 25% of total revenue. National banks recognize large upfront fees on commercial loans – approaching approximately1.3% of the loan portfolio, and most of this fee income is from hedging activity (recognized upfront) and not upfront loan fees (recognized over the life of the loan).

Loan Hedging Income For Community Banks

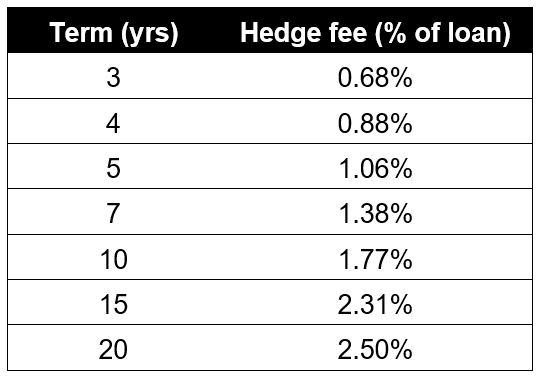

One advantage of loan hedging income for community banks is that every community bank already makes commercial loans – therefore, a new line of business is not required especially since many vendors offer off-the-shelf hedging programs that require minimum investment. Hedge fee income on commercial loans is compelling because it magnifies the value of the fee over the life of the loan. The hedge fee is the cumulative sum of a spread on a loan and is paid in a lump sum and may be recognized by the bank upfront. The hedge fee can vary from 50bps to about 2.5% of the loan amount, depending on the term, amortization, and market competition, and under GAAP is recognized when received. The table below shows loan terms in the first column and the corresponding hedge fee as a percentage of the loan that community banks can generate in the second column.

However, the fee numbers above understate the benefit of hedge fee income to community banks for the following seven reasons:

However, the fee numbers above understate the benefit of hedge fee income to community banks for the following seven reasons:

- Hedge fee income can be an important substitution for community banks for an industry-wide move to eliminating service charges on deposits.

- When loans prepay, the loan margin goes away and must be replaced with new earning assets. However, the fee income is retained by the bank regardless of if or when the loan prepays.

- Loan prepayments increase the value of fee income. If a community bank can replace the loan with another loan and another hedge fee, the fee income becomes magnified over a constant-sized loan book.

- Each time a loan is upsized, extended, or otherwise modified provides an opportunity for banks to generate additional hedge fee income. This creates a steady stream of potential new fee income without the substantial cost of new business acquisition.

- In a non-zero interest rate environments, upfront income is more valuable than future sources of income (loan coupons).

- Most borrowers do not negotiate hedge fee income but will heavily negotiate their loan rate.

- Borrowers are loathe to pay banks for almost any service. However, hedge fees are delivered to a community bank by a hedge counterparty and paid by the borrower over time – the borrower does not have any out-of-pocket costs. This is the exceptional benefit of hedge fee income and replicated by very few other bank products.

Conclusion

Historically hedge fees have been the domain of national banks. However, community banks can also generate hedge fee income, and the amount of these fees can make a major impact on community banks’ performance. The majority of community banks already possess products and customers that can allow them to generate substantial hedge fee income. Community banks should consider how growing fee income through hedge fees can increase their performance and stabilize prepayment rates on relationship credits.