The Four Attributes of Superior Service in Commercial Lending

Delivering superior service is critical in banking. In our previous article (HERE) we discussed why delivering value to customers drives value for shareholders. Value in banking (or any business) is measured by a simple formula that states the following: Customer Value = Perceived Benefits – Perceived Costs. Perceived benefits include factors like quality, service, brand, and functionality. Perceived costs include the price paid, plus time and effort expended. In our previous article we discussed the five steps to implementing superior value at a community bank. We also underscored that because of limited size and resources; community banks cannot be all things to all customers and competing on price or credit structure leads to long-term value erosion for bank shareholders. There are four attributes that community banks can deliver in abundance and larger competitors cannot. In this article we will discuss those four attributes and how to market them.

Four Attributes for Superior Service

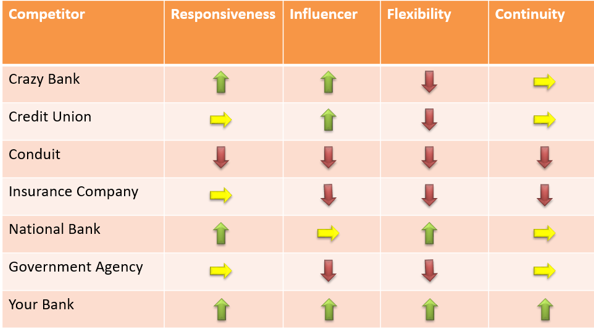

Only by adding value to customers can community banks create satisfaction, repeat business, long-term relationships, and differentiate from other, larger, financial service providers. Community banks will not be able to offer every bank service to every customer. In some cases, the banking product may not be best-of-breed, but, nonetheless, deliver what is required by customers. The table below shows the four attributes and the possible positioning of these attributes against six common competitors.

- Responsiveness: Time-on-task is the time a bank takes to accomplish an action that has an impact on the customer. The shorter the time, the higher the customer satisfaction. Time-on-task might be solving a problem, opening an account or responsiveness for a commercial credit underwriting. The action of commercial underwriting, for example, can be the time to underwrite credit, to produce a term sheet, to draft closing documents or to fund a loan. Here community banks have a distinct advantage against much of the competition. Being smaller and nimbler, community banks can typically react faster than credit unions, conduits, insurance companies, and government agencies. Clients value certainty and a quick decision-making process. Community banks should benchmark timelines for each of the tasks listed above based on competition in their market. On the high-performing end, we work with banks that can produce a term sheet within a business day of receiving the necessary borrower financials, take four business days to underwrite and approve a CRE or C&I credit (subject to necessary appraisals), take one business day to generate internal loan documents and can fund a loan within three business days from acceptance of the term sheet. On the other end of the spectrum, we see competitor banks that take three months from a commitment to funding. Your biggest competition for this attribute are the regional and national banks that have become very quick to commit clients and their required banking services, if the banking product fits neatly in their “box.”

- Influencer: Influencer describes how the client can advocate and be heard for their banking needs. This can happen both digitally or in-person. If the client can sit down and describe their business plans and personal needs to the decision maker of the bank or take the bank officer on a tour of the factory, then the influencing factor is high. Here community banks have a large advantage over most of the competition, but credit unions and some national banks may also have some power in this attribute. Community banks excel at understanding their clients because they are so close (geographically and strategically) with their clients. Clients ascribe high value to the local nature of a community bank decision-making framework, and community banks need to broadcast this attribute to their customers and prospects.

- Flexibility describes the potential of the bank to work with a client even if the relationship does not fit perfectly into the bank’s business model or if the relationship changes because of credit issues. This is an especially important attribute that community banks must not squander. One of the identified competitors is “Crazy Bank.” What we identify by this term are banks that make non-rational credit decisions. Those banks are currently in their comfort zone making interest-only loans, at 85% LTV, on low cap properties, without individual recourse, and no proven operator record in a recession. But situations and the economic environments change and when they do, will the Crazy Bank be able to show flexibility? Community banks can be flexible working with clients in good times, and if credit is initially soundly underwritten, community banks can be flexible working with borrowers in downturns.

- Continuity describes the consistency of the relationship between client and banker. Here again, community banks can have an advantage. Clients like to deal with bankers that understand their business and personal needs, and with whom they have a comfortable rapport. Commercial clients, especially, do not want to educate a new banker every couple of years because the bank is fond of rotating employees, or worse yet because of employee turnover. National banks are notorious for this mistake for small commercial banking. Further, if the economy in a particular geography takes a downturn, national banks, insurance companies, and conduits have the luxury of re-allocating capital to other geographies that demonstrate better returns. However, for better or for worse, community banks are tethered to a local community and do not move to other states. This certainty of relationship and consistency creates substantial value for borrowers, especially in unfavorable economic times.

For commercial and consumer relationships, community banks can provide superior service value on these four attributes. These attributes are highly valued by many clients, and they are attributes that community banks can excel against competitors.

Conclusion

While community banks want to differentiate from their larger competitors, it is important to show clients the value that the bank can create versus competing on price and credit structure. Delivering superior service is ground zero for building long-term foundational value. Community banks must be able to measure the value they deliver and set up benchmarks for these values. Community bank executives must explain the drivers of customer value to employees so that value is delivered consistently and noted to customers. We see four important attributes where most community banks can excel over their competitors and differentiate themselves from competitors. These attributes give community banks a marked competitive advantage.