How To Talk To Commercial Borrowers About The Future Path of Interest Rates

The Federal Reserve Open Market Committee (FOMC) has raised short-term interest rates by 3.00% in the six months between March and September. The market is now forecasting an additional 1.25% in hikes by year’s end, with the next move coming on November 3rd. Many borrowers and market participants have been surprised by the speed of these increases. In this article, we would like to share best practices of how lenders advise borrowers on planning for the future path of interest rates and how borrowers should structure their balance sheets to better manage future cash flows.

Bankers As Trusted Professionals

As community bankers, we are foremost trusted advisors to our customers. We possess knowledge and insight and are best equipped to analyze specific financial situations and then offer prudent and objective advice to help our customers. We are paid for our professional knowledge. We get paid to provide advice that benefits our customers instead of selling loans, treasury management, or deposit services.

How should we respond to borrowers who seek our advice on the future path of interest rates? The correct answer is that we do not know where interest rates will be in the future, and that is an OK answer because that is not where we add the most value when offering advice.

There are five general areas that borrowers and lenders can consult to predict future interest rates: 1) the FOMC dot plot, 2) composite economic forecasts, 3) public and private modeling, 4) historical context, and 5) the futures market. However, all of these five predictors are, on average, wrong. If anyone could predict future interest rates, they would immediately abandon their day job. While forecasting and debating future interest rates may be an interesting conversation at dinner parties or business conventions, it’s foolish for anyone to think they can predict the future. Luckily, lenders don’t need to have a crystal ball to be valuable, trusted advisors to their customers.

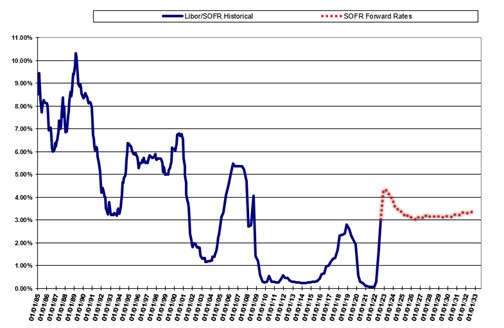

Example of Future Path of Interest Rates

A trusted advisor understands clients’ wants and how to help them get there. While lenders do not know where interest rates will be in the future, they can analyze a customer’s balance sheet, cash flow, and business model to structure products that insulate customers from adverse outcomes, regardless of what interest rates may do in the future.

We work with a banker (Neil) in the Northwest who follows the following principles when borrowers ask about the future path of interest rates.

First, Neil presents the interest rate futures curve to his borrowers. He states that no one can predict the future, but using the market expectations, where participants risk billions of dollars on forward positions, is the best place to start. Below is an example of a graph in which Neil shows his borrowers where short-term interest rates have been from 1985 to the present (blue line) and where the futures market believes interest rates will be for the next ten years (dotted red line).

Second, Neil points out that the forward curve is the market’s best estimation of where interest rates will be in the future, but the market is consistently wrong. Smart participants understand that the forward curve is just the best measure of expectation, and borrowers must factor in dispersion around the forecasted mean. That dispersion is currently about 80bps for one standard deviation in today’s market. Therefore, borrowers should consider if rates are 160bps higher and lower than the forward curve predicts to capture two standard deviation dispersion.

Third, Neil focuses borrowers on their business models instead of the forward rates. He asks borrowers what would happen to their business if rates are higher by 160 basis points than the market predicts, and what would happen to the business if rates are 160bps lower than the market predicts? What impact would rate movement have on the borrower’s balance sheet, cash flow, and income? There are a couple of key parameters to consider. If the business can generate more earnings before interest, taxes, depreciation, and amortization (EBITDA) or net operating income (NOI) if interest rates are higher, then the borrower has less interest rate risk exposure. However, if EBITDA or NOI is not sensitive to rising rates, then the borrower has interest rate risk exposure and needs to protect their business with stable debt expense. The second parameter is the expected timeline for financing. For example, if the borrower intends to retire in two years, the financing needs should be secured for two years. Alternatively, if the borrower wants to finance the business for the foreseeable future, is intent on growing the business and expanding, or has succession planning, then the financing needs should more closely match the longer duration of those needs.

Fourth, Neil does not try to sell his view of where the capital markets will be in the future because he knows he cannot predict that. He focuses on helping prospects understand their needs and risks and provides insight into the borrower’s business and how the bank’s product can reduce the borrower’s cash flow risk and increase profitability. Neil is so conscious of the borrower’s needs that he has historically suggested another bank’s product if his bank cannot provide the ideal solution. He knows that customers who trust you will do more business with you in the long term.

Conclusion

We believe that to be an effective and successful community banker requires us to be trusted advisors. Since we have not met anyone that can predict the future path of interest rates, lenders should focus on helping borrowers understand what can be more easily forecasted. Lenders provide the best value by understanding the borrower’s rate view and industry outlook. Then, they can add value by analyzing the borrower’s balance sheet, cash flow, and liquidity positions, then offering products that can help borrowers reduce business risk and increase profitability.