How To Do Better Against National Bank Lending Competition

Community bankers need to understand their competitive landscape. Who the competition is, what the lending competition is offering, their delivery channels, and service levels can help community banks differentiate their services and enhance their competitive advantage. Understanding the competitive banking landscape helps community banks set proper pricing, respond to rival marketing, and compete more effectively. Analyzing the competition can also help a bank be realistic about which products it can sell and at what price. Unfortunately, banking is challenging to study, and some banks inadvertently ignore their significant competitors. Community bankers sometimes fall into the trap of believing that they are competing exclusively against other community banks, but nothing can be further from the truth. Many existing community bank customers and prospects are also national bank customers. Community bankers must understand how and why the country’s largest banks compete for the most profitable local deposit and loan customers and be able to respond to that competitive threat.

Who is Your Lending Competition

With the increased use of the internet to buy banking services, banks no longer have just local lending competition. The banking industry is nationwide and is becoming less branch-focused. There are now many online, nationally-focused lenders that are capable of an entire virtual relationship. Further, the competition is not just another bank that might make a loan or take a deposit, but it could be a credit union, insurance company, retail store, or a fintech.

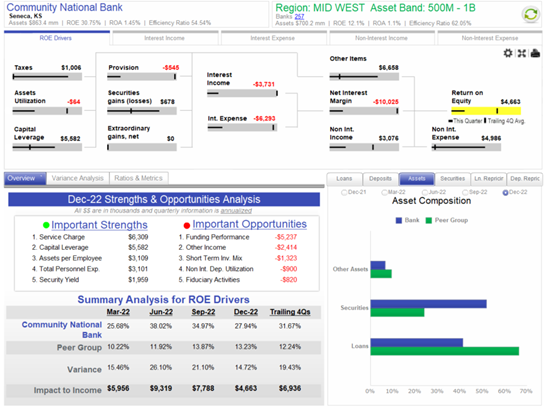

Traditionally, community banks would compare their financial performance and health to similar-sized banks in their region. The graph below shows a random community bank compared to similar-sized banks in the mid-west. The peer group is 257 banks between $500mm and $1B in assets in the mid-west. Unfortunately, this peer group eliminates the vast majority (over 80%) of the competition in this community bank’s footprint. By excluding larger bank lending competitors, this SWOT analysis is mainly useless because it doesn’t compare this community bank’s performance with the majority of the banking competition in its region.

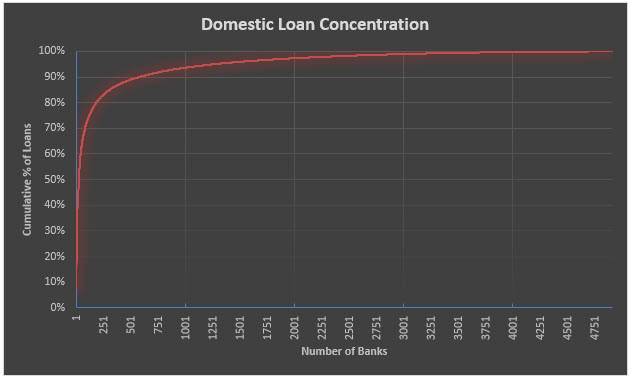

The graph below shows the concentration of domestic loans for all banks in the country, and it demonstrates that just a few banks control the vast majority of the loans. The same picture emerges for domestic deposits. The country’s largest few banks hold most domestic loans and deposits, and the smallest 4,500 banks barely make up 10% of all loans and deposits.

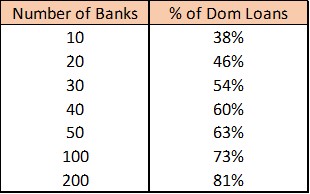

The largest 100 banks dominate the industry with almost 75% of the market share. The number of banks that control the domestic loan market is summarized in the table below.

What is starkly evident in this data is that a small number of banks control a significant majority of the loan (and deposit) market. Over the decades, the largest banks have been gaining market share while the total number of banks in the industry has been declining. However, community banks largely exclude these big institutions from their SWOT or competitive analysis.

When we talk to community bankers, most say they do not believe they compete against the country’s largest 100 or 200 banks. We feel that community banks overlook a vast percentage of profitable clients and prospects by excluding national and regional banks from their analysis. Further, community bankers may be overlooking products, services, delivery methods, and strategies that the largest 200 banks in the country use to gain market share and profitability.

The national and regional banks are not doing everything well, and community banks would be making a mistake if they imitate larger banks’ business models. However, community banks are competing for loan and deposit customers that are also customers of the largest four, ten, and 100 banks in the country.

Notable Tactical Differences in Lending Competition

Many of the largest banks in the country consider themselves technology companies that manage and measure profitability and maintain relationships. Scale, security, and innovation are all linked to better information technology design and implementation. Large banks that are not investing heavily in IT cannot compete effectively. Community banks cannot match software companies or larger banks in spending and IT development. Still, community banks also have talent and can evolve and buy off-the-shelf technology that allows them to compete more effectively.

Community banks should not mirror the larger banks in their services, price, or delivery channels. However, we see a few essential management tools that community banks are overlooking, which the larger banks deploy consistently, and that allow these larger banks to be uber-competitive. Community banks should consider implementing the following management tools (all used by their larger competitors) because they are easy to adopt and can gain community banks significant advantages against their lending competition:

- RAROC – larger banks measure product profitability with risk-adjusted return on capital models. Loans, deposits, fee services, branches, product lines, and relationships can all be measured using a RAROC model, allowing for better capital allocation, product development decisions, and product pricing.

- FTP – larger banks, as a rule, deploy funds transfer pricing in RAROC measurements. This tool allows banks to understand the profitability contribution from various units and products. FTP allows banks to allocate profit to branch deposits, loan pricing, liquidity premium, duration risk, and optionality.

- SVA – larger banks consider shareholder value-added pricing, which takes into account operating profits produced over that bank’s cost of capital. This helps banks understand the importance of size and scale to profitability. Community banks may still want to make smaller-sized loans, but understanding the impact on SVA helps banks determine how much of that business they want to do and at what cost.

- Debt yield – At most larger banks, debt yield is an underwriting criterion on real estate loans in addition to loan-to-value and debt service coverage ratio. Debt yield measures the return the lender would receive if they foreclose on the property. Debt yield is an essential underwriting criterion in a low or declining capitalization environment. We will write more on this topic in our next article.

Conclusion

Community banks should not try to be national or regional banks. They can maintain a high level of service while innovating products and services to best their lending competition. Community bankers can learn from larger competitors and position their banks to solve their customers’ challenges, and we should consider national and regional banks as our direct competitors. These larger competitors control most of the market share and would gladly have a community bank’s best customer – just the customer you want to keep.