CRE Credit Risk – What You Need To Know Now

The current banking crisis has put a magnifying lens on all non-Too-Big-Too-Fail banks. While the market focuses on deposits and liquidity, media pundits and analysts are waiting for credit problems to appear. Of all the credit risks within banks, one of the largest is in commercial real estate exposure. When CRE credit risk arises, it will likely spark a new round of bank failures. This article explores the risk and what to do about it.

CRE Risk Background

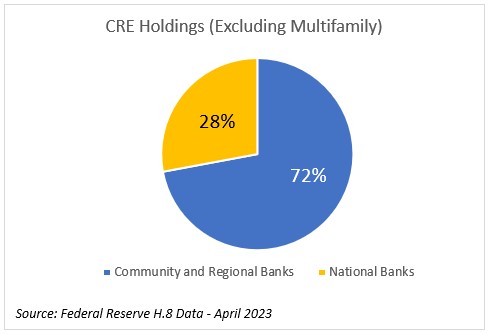

While ten years ago, community and regional banks use to make up some 55% of the CRE market, in 2023, these banks now compose approximately 72% (below).

More concerning is that while the CRE growth has slowed from double digits to just over 1%, regional and community banks are at a pace of greater than 12% of year-over-year volume growth.

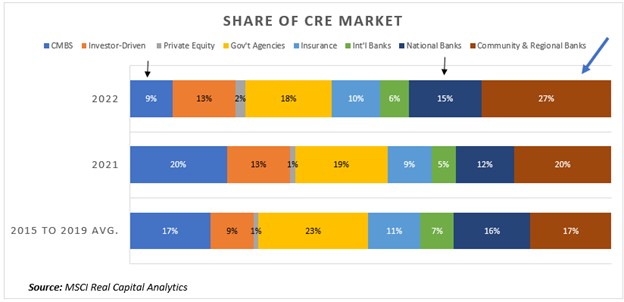

Taking a broader market share perspective, community/regional banks have expanded their market share of the CRE market from an average share of 17% over the four years from 2015 to 2019 to a share of 27% during the last year alone. Meanwhile, most other segments have maintained their averages. The risk here is that community banks continue to take on an above-average amount of CRE credit exposure.

Higher rates have already challenged credit availability. Making matters worse, lower liquidity from private equity and the commercial mortgage-backed securitized market has also put stress on borrowers. The little liquidity left in commercial real estate is in major markets such as Los Angeles, Chicago, New York, and D.C. In secondary and tertiary markets, it is only smaller financial institutions lending.

This lack of liquidity in the market now shows in CRE loan pricing. Reaching near its all-time lows last year, credit spreads were routinely around SOFR + 214 basis points. At the start of the year, pricing reverted to its mean of around 247. Now, amidst the banking crisis, spreads have increased to 295.

CRE Risk Circa 2008

If all this feels too familiar, these are the same conditions that were present in late 2007 when the Fed raised overnight rates from 1.00% to 5.25%, and many financial institutions had a negative market-to-market on their assets. The financial markets, then banks, pulled away from subprime mortgages, and many lenders, starting with New Century Financial Corp., touched off a wave of bankruptcies. What started as an interest rate shock turned into a liquidity shock and then manifested with a credit shock.

The writing was on the wall in late 2007; however, many community banks continued to lend at a rapid pace through 2008, not knowing they were headed full steam into a recession.

While national banks took the brunt of subprime mortgage losses, in the years (2008-2013) following the Great Recession, credit risk spread to CRE. Speculative and cyclical commercial properties came under pressure, and the end result was 507 community banks failed. Another 1,305 community/regional banks were driven into the hands of competitors through M&A (HERE).

The CRE Credit Risk That Is In Front of Our Eyes

The combination of rising rates, quantitative tightening, and less credit supply sets the table for a similar credit shock to banks that we experienced in 2008. The current rash of loan defaults has been primarily driven by borrowers taking on floating-rate risk and finding their interest payments are outstripping their cash flow. Soon, this will translate into balloon mortgages and adjustable resets.

Of particular concern are loans backed by office properties. Several entities, including conduit lenders, insurance companies, and banks, are covering up problems in the future performance of office loans. Few lenders have the incentive to disclose their risk. As such, the risk is lying in wait.

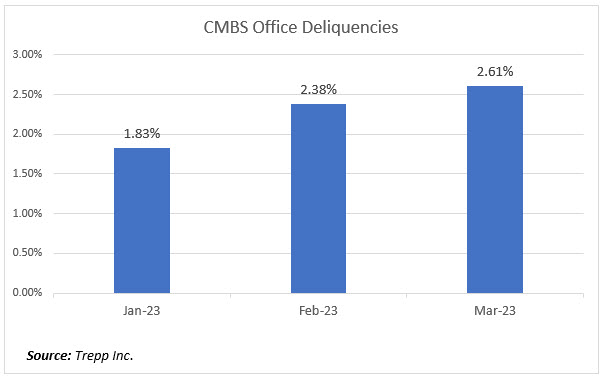

A look at securitized commercial mortgages shows a steady increase in office delinquencies (below).

Another way to look at this is that several firms utilize machine learning to normalize cell phone data to generate an accurate visitor count for any given property. What they have found, on average, is that foot traffic is down about 50% from 2019.

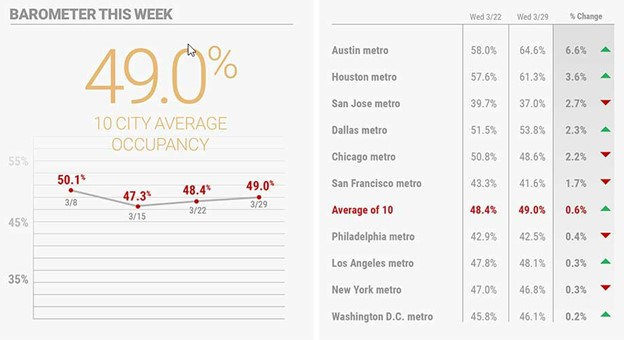

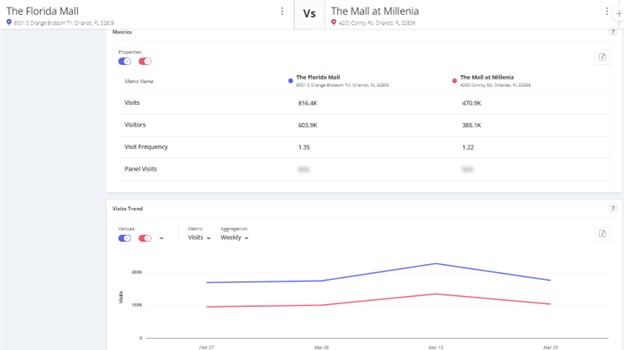

This data is further corroborated using data from firms like Kastle, which can track traffic through building controls and maps it to the days of the week (HERE). Their analysis shows that occupancy ranges from an average of 34% on Fridays to 56% on Tuesdays, with an average of 49% (below).

The downside risk here is that lessees will continue to downsize their space as it comes up for renewal. While a drop in occupancy was many banks’ worst fear when underwriting office property loans, it is now the norm. As such, we look for many more loans to be restructured in the coming years.

The latest analysis by Morgan Stanley shows that approximately $1.4 trillion worth of collateral office buildings will come up for refinancing over the next two years. If rates stay where they are, borrowers will find their rates some 3.5% to 4.5% higher than their initial loan.

To be clear, not all CRE is in trouble. Multifamily should continue to perform due to the positive demand/supply imbalances. Data centers, warehouse space, and healthcare are expected to continue to do well. However, office, traditional retail, and others are likely heading for trouble. Here, valuations are down some 40%, and loan-to-values are now over 100% (more information HERE).

Nine Tactics For Banks

While some of the damage is done, banks can take the following steps to limit their CRE Credit Risk:

- Increase Communication with All Borrowers: At the last poll done by Abrigo, almost 60% of bankers preferred for borrowers to call them to discuss restructuring options. This is the single most significant tactical mistake. Banks must start now and be proactive in triaging and reach out to all borrowers to check their status and avoid surprises. Management needs to establish a communication plan and standards immediately to stay ahead of CRE credit risk.

- Increase CRE Credit Resources: The dynamism of the market now takes constant vigilance. Community banks would be served well by increasing the amount of monitoring and management resources in their CRE portfolio. Banks should start to ask for increased data on occupancy and net rents. Third-party data sources such as Kastle or Placer.ai should be considered to augment property-level intelligence (below).

- Look 18 months ahead: Triage your loan portfolio as to CRE credit risk and prioritize floating-rate loans, adjustable-rate loans, and balloon mortgages. While banks usually look three to six months ahead of these events, you should increase your horizon to allow for the most flexibility for restructuring and workouts. The ability of bankers to grab cash, future cash flow, collateral, and data early has proven to be the critical element of success in a credit downturn.

- Understand The Property & The Documents: At this point, each property’s cash flow is likely to be nuanced. Walk the property ascertaining its condition and potential needs. Inspect the tangible assets. Review the appraisals. Do UCC searches. Be clear on the entitlements, “springing” guarantees, and potential for bankruptcy. Audit the A/Rs, the invoices, other transaction accounts at banks, and inventory for owner-occupied properties. Have a clear view of the current quality of your collateral. Understanding the dynamics of the physical geography, the major tenant(s), and the potential trends of industries that might use the property are essential in developing a pre-workout plan. Starting this process early will give your bank an advantage. The same is true for loan documents. The loan documents of at-risk borrowers should be reviewed, and any mistakes or shortcomings should be corrected now before relationship risks become adversarial.

- Focus on Special Assets: Many banks’ special asset groups have been dormant for the last five years. Now is the time to bring this department back up to speed and get them working on restructurings ahead of other bank lenders. Bankers need to understand the nature of positional fluidity as some bankers will now need to flow between departments at a much quicker than normal rate. The current banking crisis could quickly turn into a macro banking credit contagion.

- Reengage Your Network: Now is the time for the special asset department to reach out and re-establish relationships with private equity, mezzanine lenders, and other pockets of capital to help in restructuring the capital stack for large properties. These lenders and equity players can have more flexibility than many banks and help a bank secure its position in exchange for future upside. In addition, you might need refreshing relationships with workout attorneys and contract employees. Banks want to get on pre-negotiation letters early and will need additional resources.

- Be careful about Floating, Adjustable Rate, and Balloon Loans: It is unclear where rates will go, but we caution banks about exacerbating their interest rate risk problem. As we have recommended over the past several years, banks should consider locking the rate to the borrower and then floating the rate to the bank utilizing a loan hedge (ARC HERE).

- Move Up in Credit Quality: The best way to offset losses is to keep the income coming. There are still quality borrowers with low CRE credit risk out there looking for help. Banks are likely already choosy but should pay particular attention to the quality borrowers that have many options and many relationships that could be consolidated. While this article is a plea for defense, a good offense is part of that. Locking in a borrower for long-term financing may be the best defense. The critical factor here is the acknowledgment that the yield on loans may drop, not increase. This is counter-intuitive since March saw a material increase in loan pricing spreads in-line with higher probabilities of default. Banks are cautioned about increasing nominal credit spreads without taking into account risk and increasing the probability of being adversely selected by riskier borrowers.

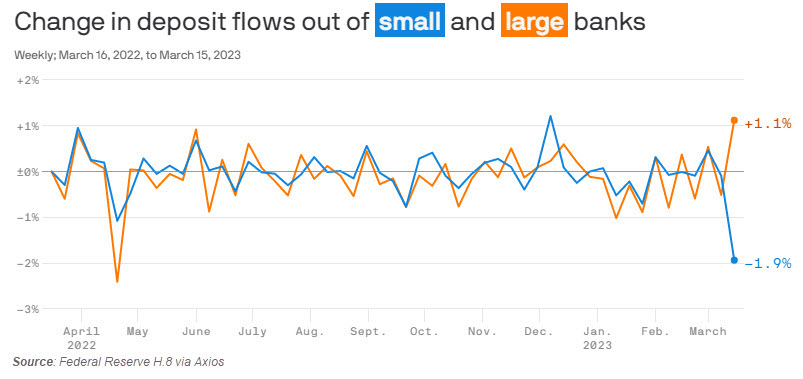

- Control Growth/Shrink: Pressure on funding costs and higher cost of capital now makes growth more expensive. According to Federal Reserve data (HERE), community and regional banks saw $108B, or almost 2% of the deposit base, go out the door to larger banks, money market funds, and investments (below). Sometimes the best strategy is to retreat and live to see another day. Banks should consider shedding risker credits in any way possible while adding quality borrowers to offset earnings and build their performing asset percentage. On a net basis, banks need to be prepared for lower earnings, but that will be far better in the long term than higher delinquencies.

Putting This Into Action

This is not a message of panic but of caution when it comes to CRE credit risk. The next few years will likely be a difficult time, and this is a plea for bankers to get ahead of the potential forthcoming crisis. While a full-blown credit shock is not a foregone conclusion, the probability of a downturn is quickly approaching 50%. Being proactive, organized, and focused on specific objectives will help banks gain a competitive advantage.