What AI-Simulated Depositors Can Teach Your Bank

Up until this year, when a bank wanted to forecast the response to new deposit pricing, it either had to guess off its data, use a focus group or see the reaction to a test market. These methods were either inaccurate or took time. Now, synthetic data and AI-driven agents are starting to replace traditional methods not only allowing banks to increase accuracy, lower cost and shorten the time-to-market, but can now allow them to test thousands of prices, product, and promotion combinations. In this article, we explore this new paradigm for how banks are starting to understand their markets by using AI-simulated depositors. We show the technology that will progressively replace traditional deposit performance forecasting.

The Problems with Traditional Deposit Forecasting

Traditional deposit forecasting revolves around a set of fragmented tools to include regression analysis based on historical data, conjoint studies that ask banking customers to choose between hypothetical pricing, and panels that track deposit behavior for a defined sample over time. Each of these approaches have value, but also shortcomings.

Historical deposit elasticities reduce a complex market response to a single number, often ignoring the interactions between product such as certificates of deposit or money market accounts. Deposit elasticities usually do not show the non-linearity of the depositor’s response to price. Focus groups and panels often yield valuable information but are slow and expensive. They also may not reflect current market dynamics or are not representative of the targeted potential customer base.

Many regional banks still use methodology and tools from the early 2000s when data was scarce and compute was expensive.

What Are AI-Simulated Depositors

AI-simulated depositors are a new solution to an old problem. The approach is fundamentally different than using historical interest rate and balance regression approaches. Instead of estimating aggregate statistical relationships, AI-simulations constructs large populations of AI-calibrated agents that mimic human behavior. Each agent has its own preferences for product attributes (e.g., account type, tiers, brand, branch location), their own sensitivity to interest rates, and their own behavioral characteristics (e.g., response to alternatives, susceptibility to promotions, friction of switching banks, the need for safety).

AI-simulated depositors make purchase and balance decisions, just as real customers do, given a specific competitive situation. The situation can take into account current interest rates, investment alternatives, consumer confidence, sentiment and product attributes. The result is a bottom-up simulation of market demand that emerges from individual-level decisions rather than being imposed by a top-down statistical model.

For pricing simulations, banks can ask the question – “What amount of balances this offer would attract?” Each agent has a different objective, sensitivity and set of preferences. By combining a spectrum of agents, a solution can be obtained. Better yet, these agents can be asked thousands of times, which allows the banker to explore a solution space that not only is most likely but can uncover a set of prioritize objectives.

The Affinity Account Example

Let’s say, for example, your bank wanted to create an affinity account where the bank would donate a current 2.85% interest rate to the depositor’s non-profit of choice. You are interested in how your market reacts and, more importantly, how your current customer base reacts. You then create a set of agents based on the data of your current customer base and the economic, demographic and psychographic data of the area (we use ESRI) mapped back to your customer base so the model has a strong idea of how your potential customers will react given your current customers.

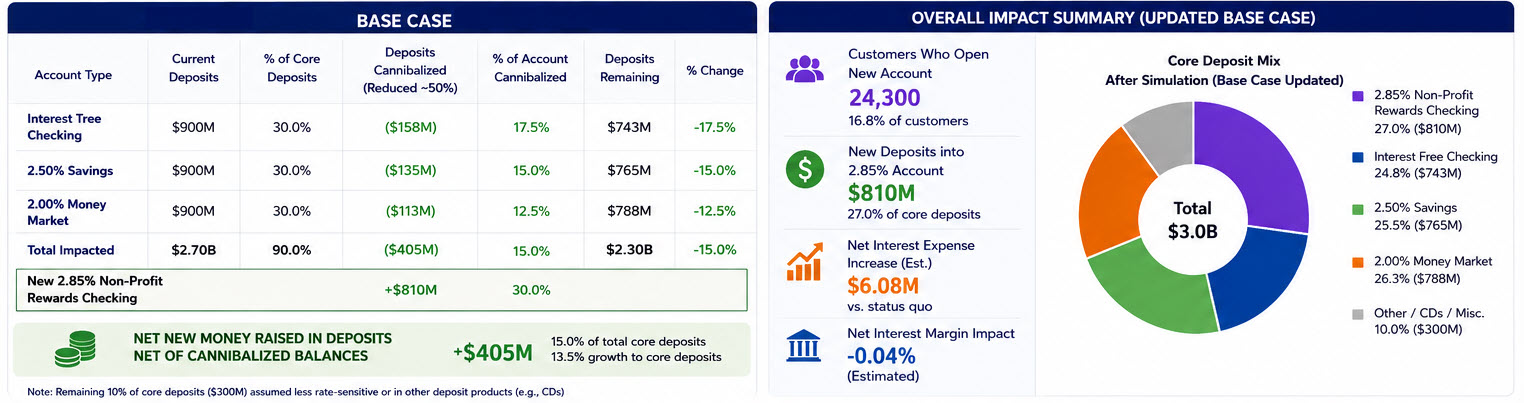

The model then runs thousands of iterations and comes out with the base case as outlined below.

Using an agent simulation on a set of assumptions, a bank can see that this scenario generates $405mm of new money will cannibalizing about $810mm of existing funds for this $3B bank.

Why AI-Simulated Depositors Will Change Your Bank

In addition to seeing the overall behavior of new and existing customers, bankers can drill down into specific questions – How much of the funds are coming from outside the footprint and how much is non-insured? Different customer segments, represented by bots, can be broken down and queried.

In the example above, it is Segment 19, the “Milk and Cookies” psychographic that are young affluent families in the Texas suburbs that have young children and an average income of $138k that are the most likely to take this promotion.

This solution set would be hard to obtain through any other methodology.

This is to say, by using AI-simulated depositors, you can model interactions. If you increase the rate on your money market account, some AI-simulated depositors will adjust their balances in CDs and checking. Traditional price elasticity models treat each product independently. AI-simulated depositors treat the bank’s deposit market as a system (which it is).

Another advantage is that agentic depositors are derived and can be evolved by more data. Historic deposit data teaches AI-simulated depositors the revealed preferences of real customers. Conjoint survey results can be layered in to capture preferences for attributes not yet tested in the market.

For example, the next time the bank does a customer survey, AI can use the information from that new survey to weight the importance of brand, marketing and any new locations the bank imparts on its customer base. The result is a single coherent model rather than disconnected analyses that need to be manually reconciled.

Finally, having a group of theoretical customers at your disposal restructures how bankers think and work. The marginal cost of running an additional scenario drops to essentially zero. Once built, new simulations can be run in minutes. Instead of looking at a single scenario, chief deposit officers, liquidity managers and customer experience officers can now look at multiple deposit pricing scenarios across hundreds of alternatives. Not only can more solutions be explored, but they can be explored with much higher analytical confidence.

Best of all, bankers start to better understand the customer base they have and quickly figure out how to get the customer base they want. Bankers can not only know how customers might react to any given new product introduction or pricing promotion but understand how various cohorts of demographic or psychographic segments react. Bankers quickly get a quantified feel for which customer segments are the most responsive, loyal, the most profitable and where the greatest opportunities are.

The Limitations

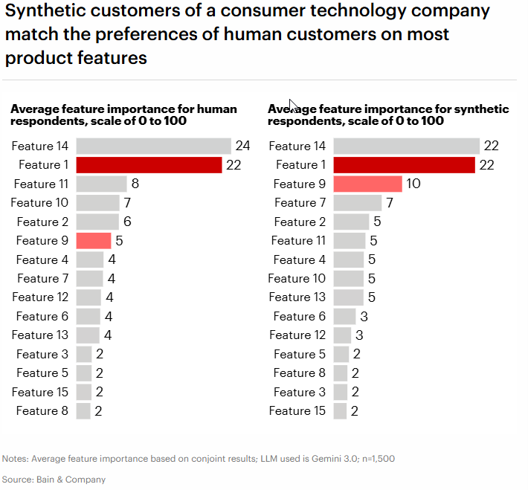

Like any AI methodology, there are inaccuracies. In a recent Bain & Company study (below) match product feature desirability in the 75%+ area, which is fantastic. However, the more you ask the model to assume, the more it will speculate and we have seen accuracy drop to the 25% range for a theoretical deposit product that is not invented yet.

AI-simulated depositors also do not help with understanding customer’s formation of qualitative preferences. In our example above, ask the model about the AI-customer’s feeling about a new tokenized deposit product and not only will the balance projections likely be inaccurate, but the preference strength and framing will likely be made up (which may or may not be accurate).

This is to say that there is still a place for talking to your customers, customer focus groups, and test markets. AI-simulated depositors can tell you HOW they might react, but not WHY they behave the way they do. The human “why” is beyond the reach of any current AI model.

Coming Up Next

We will be talking about this more at our upcoming Deposit Conference in addition to delving more into the output and how to better use AI-simulated depositors. In future articles, we will discuss how to build, or obtain, these models plus we will be exploring how banks are structurally changing their strategy and tactics to better act on what this deposit analysis reveals.