Here is the Biggest Problem Banks Face with PPP Forgiveness Processing

There is no surprise that you can only do so much when it comes to educating PPP borrowers. We have produced a comprehensive website, executed a detailed email campaign, conducted a series of webinars, produced videos, have a Getting Started Guide, and distributed a checklist – still, borrowers remain deficient in completing their application accurately. In this article, we explain this educational black hole, provide the latest data, and detail not only what it means for banks looking to process applications more efficiently but ways to solve the problem.

The Challenge

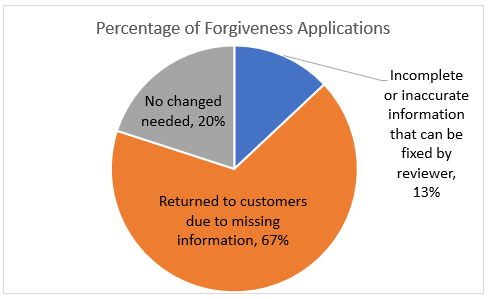

If you review 100 applications, 67% of these will need to be returned to the customer due to missing information. That is not only a surprisingly high number given all education that banks are doing, but potentially disastrous come October when most borrowers will file, and banks will need to hit full productivity to keep up.

Of the 67% of these applications that are returned, 12% of these will be received back to the bank and need to be kicked back to the borrower a second time, further taking resources.

In 13% of the applications, information needs to be corrected. This includes the wrong loan number, tax identification number, funding date, dollar amount, and other basic data. Our packaging team goes through some automated and manual checks and corrects information if known.

The biggest problem so far with PPP Forgiveness processing is that only 20% of the applications go through what we call the “happy path” or through a process that requires no additional interventions. Having to change the application and having to go back to the customer adds extra administrative and processing time to the tune of an average of 30 minutes of processing time and a delay of one to five days. At scale, this is ruinous to efficient production, but we point out pales in comparison to having an SBA reject and then having to re-process later in the workflow.

- Missing 2019 owner compensation support

- Missing or incorrect Feb 2020 utility baseline evidence support

- Missing non-cash (i.e., health care) or utility proof of payment

- Uncertainty on cash compensations (i.e., no bank statements and/or unclear if supporting payroll reports support claimed forgiveness).

- The lease or mortgage is not in the name of the business, dba, or owner, and there is no explanation.

While this data may not be the same for your bank, we suspect it is. Again, we are getting this high rate of rejected applications despite the fact that more than 25% of our borrowers attended one of our webinars and video sessions, where we discussed these exact topics. Banks that have not conducted as an extensive of pre-application educational campaign are likely to experience even more significant production problems.

Before You File

Now that the problem is identified, the solution is to provide a focused marketing effort targeted at the time just prior to when the borrower will start the application. This “Before You File” email text or pop-up, provides the “Top 5 Items to Check Before You Submit” content.

The smaller your service area, the more effective this email can be as you can show actual examples of payroll schedules and bills to upload. Banks can take examples from a sample population of customers and show anonymized graphics of what page of their utility bill to submit or upload (below).

Further, banks may also want to include links or graphics to help borrowers generate the needed payroll report since that is also one of the most common questions asked. While banks can’t do this for every payroll company, many top payroll companies such as ADP, Gusto, Paychex, QuickBooks, and Deluxe have examples either on the web or that they can send you.

Using the Double Tap Methodology For Improving Performance

While we have discussed this in the past, one common trick that bank marketers use is if they send a piece of marketing content via email. The customer opens it, and then opens it a second time, this “double-tap” usually means they are reconsidering your value proposition. Good bank marketers know that if they send a follow-up email within the same day as the double-tap, they are 60% more likely to gain engagement with that customer or prospect.

Using this methodology for PPP Marketing, if a bank sends an invite or general information to submit and a borrower double taps on that email, then they are likely getting ready to file. In this case, if you send a follow-up “Before you file” email, you will gain a material increase in form completion, saving your bank potentially thousands of processing hours.

Marketing email technology such as Hubspot, Salesforce Marketing Cloud, Adobe Marketo, and others can automate this for banks making this easy to execute. It takes just minutes to set up and tens of thousands of dollars saved.

Putting This Into Action

If you have this incomplete application problem currently or about to start processing applications and anticipate this issue, then consider preemptively sending educational content using the double-tap methodology for maximum effectiveness. This is likely the most critical issue that banks can solve in order to speed up production and save both time and aggravation.