How Growth Can Destroy Bank Performance

As we say – every bank must pay for growth. The most obvious case is when a bank hires staff to bring in and service new customers. People. marketing, branches, technology, capital, and many other items are all inputs or investments into growth. The need to grow is probably the single biggest driver for bank CEOs. While many bank managers say “shareholder return” is their number one priority, their actions speak otherwise. Despite what these managers say, they often destroy bank performance for the prospect of future growth. In this article, we take a counterintuitive look at the math behind growth and show how growth impacts value plus detail when it is better to grow or not to grow.

The Math of Valuation Creation and Bank Performance

In order to generate long-term growth, banks need to make certain investments. The amount you invest depends on your bank’s ability to generate a return on capital from new investments. For example, if your return on equity (assuming no debt) is 15%, and you want to grow at 6% per year, then you will have to reinvest 40% of your operating income back into the bank each year assuming your current level of efficiency. The formula is:

Capital Reinvestment Rate = Forecasted rate of growth / Return on capital

The No-Growth Scenario

To better understand the reinvestment/growth trade-off, consider what would happen if you did not reinvest in growth. If your bank generates $10 million in operating earnings and your cost of capital is 10%, then the bank’s value can be considered to be $100mm, or $10mm/10%.

Your board gets together and decides that there is a better path and wants to pursue a basic level of growth in order to keep pace with the economy. The Board and management decide that 3% growth is a fair number. They still expect a 15% risk-adjusted return, so management uses the formula above and calculates that their reinvestment rate should be 20% or 3%/15%.

The value of the bank now changes and can be calculated at $114.3mm, or $10mm * (1-20%)/ (10%-3%). This means that the value of the bank, given our assumptions, will increase in value $14.3mm by pursuing a basic growth policy.

The Board then asks the appropriate question, “How much should we grow?”

How Fast To Grow for Bank Performance

Bank investors are obviously supportive of growth and are willing to trade off dividends and appreciation today for greater value in the future. The extent at which rational investors are willing to do this is largely driven by the following three factors:

Sacrifice: Is sacrificing 20% of current capital worth growing at 3% per year?

Sustainability: Can the bank continue to grow at X% per year in the future? A young bank may be able to grow at 20%, but sooner or later that level of growth will be difficult to sustain.

Confidence: Does the Board believe that a given return can be achieved from the new investment? Of the three questions, this aspect is the most critical and is why we stress that banks need to understand and achieve their cost of capital. For a large number of banks, the cost of capital and their return on capital is the same. If this is the case, the Board is indifferent to growing since any investment will produce the same as returning the funds.

If there is one point to take away from this article, it is – if your bank is not producing above its cost of capital, then adding more assets, liabilities, and operations HURTS, not helps bank performance. This is a huge point that is lost on many bank boards and even regulators. The board sits around each year planning to grow but never realizing their growth sows the seeds of their own destruction. It would be far better if the board focused on profitability first and then growth.

This is one of the deepest ironies in banking – a board and management celebrate at the end of the year for achieving their growth targets without realizing that the bank is worth less than when they started BECAUSE they achieved their growth goal. This blind spot often goes beyond the board and management as we have seen many regulators comment on strategic plans but skip over the elephant in the room that the bank’s growth plans leave the bank with less value than when they started the year. A strategic plan must first lay the groundwork to achieve a return over a bank’s cost of capital before it can grow.

Your Bank’s Cost of Capital

Since not all growth is good, bank managers need to strive for growth that provides an excess return above the cost of capital. As of this month, the cost of capital, adjusted for inflation, at banks is about 7.86% for a national bank, 8.47% for a regional bank, 8.90% for a publicly traded community bank, and about 9.57% for a privately held bank. For context, the average community bank is within the 10% to 12% range over the last ten years.

As a rule of thumb, the more liquid your bank’s equity is the more metro markets you serve, and the more stable your earnings, the lower your cost of capital. In the same vein, the lower interest rates, and the lower expectations of inflation, the lower the cost of capital.

To track the cost of capital for banks and other sectors, an excellent resource for data and calculators is the NYU Stern University dataset that can be found HERE.

How To Destroy Bank Value

Let’s assume your cost of capital is 10% but you are only producing an 8% return on capital which happens to be the 10-year average for the community banking industry. Using the first formula, this yields a 37.5% reinvestment rate or 3%/8%. Thus, the in-place value of the bank drops to $89.3mm, or $10mm * (1-37.5%) / (10% – 3%). In this case, the bank would have been better off reducing expenses and choosing not to grow.

If a bank’s return on capital is greater than its cost of capital, then the value of growth will increase as the growth rate increases and the length of the period of that growth extends. Conversely, the value of your bank will move inversely with your growth rate and the length of your growth period the more you underachieve the cost of capital. In other words, the better investor you are of your capital, the more the value of that growth is worth.

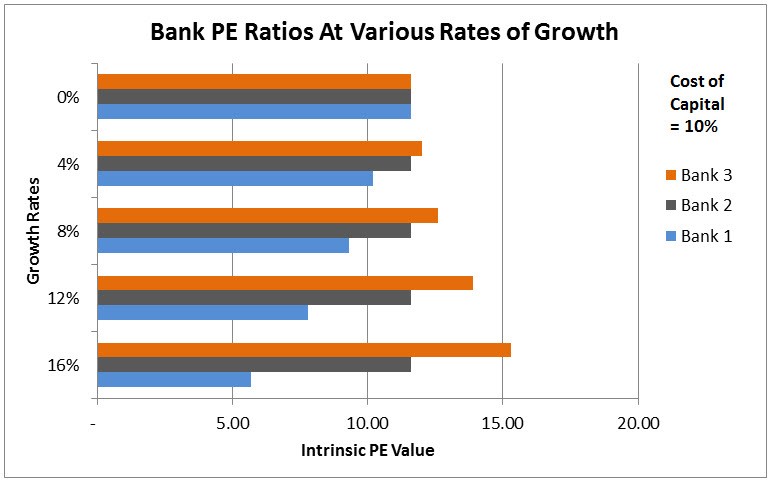

Another Way To Look At The Value of Growth

Let’s look at this challenge in another way. We can calculate the “intrinsic” PE ratios given different levels of growth for the three banks. We will assume all have a cost of capital of 10%, but we will change the returns from new investments in growth – Bank 1 earns 8%, Bank 2 earns 10%, and Bank 3 earns 12%.

As you can see above, Bank 2 that earns its cost of capital retains a price to earnings (PE) ratio of 11.6x with growth or without. This compares to Bank 1 that earns below their cost of capital. Here, the PE ratio decreases as growth increases which is another way of viewing the destruction of value. Bank 3 is the most successful investor of capital and its PE ratio increases as growth increases. This difference in multiples is the price of growth and an investors/managers’ point of indifference. You would pay up to this amount to achieve that level of growth.

Putting This Concept Into Action To Help Bank Performance

Understanding the value of growth is another tool to help bank managers and their boards make strategic decisions. Calculating the value in place of a bank’s assets and then looking at that change in value can help analysts understand if that bank is under, over, or evenly valued. Bank management can also reverse the formula above and ask, “What does my growth rate need to be in order to achieve a given return on capital for a given period of time?” This is often called the “implied growth rate” and yields an equally telling result. Some banks come out with reasonable growth rates while others require growth rates that are unachievable in any market.

These calculations can also be used for strategic planning as one of the main questions for every bank’s management team is – how can we drive operating leverage? Targeting a growth rate is an insufficient measure as we have shown today. Banks need to choose strategic initiatives that increase their profit margin while at the same time growing profit. For more insight into the strategic planning process, be sure to check out our recent article that talks about how to incorporate the right amount of risk into your strategic planning as well as highlighting the top initiatives for community banks (HERE).

Growth, in the wrong hands, can be dangerous. In the right hands, it can drive value and fuel bank performance. Bankers should take note of their cost of capital and be cognizant of the level and track record of their investments in growth. When returns are tough to come by, growth should be reined in and controlled. When risk-adjusted returns create value, they should be supported.