7 Levers To Pull For Commercial Loan Profitability

We were recently collaborating with a community banker who was trying to win a relationship client from a regional bank. The issue was that the incumbent bank was pricing this client at a credit spread of 1.25% over SOFR and our client banker was told that his bank would not accept less than 2.40% credit spread. The banker stated that “bank management is trying to exercise pricing discipline and increase the bank’s existing return on equity (ROE) of 7.4% by increasing net interest margin (NIM) from low 3% to at least mid-3.0%. It seemed like this deal was a non-starter for this community bank, except that the minimum acceptable credit spread that management had instituted was the root cause of this bank’s underperforming ROE. In this article we will explain our analysis and how community banks can build commercial loan profitability, and why minimum credit spreads, in isolation, do not explain bank performance.

A RAROC-Based Framework for Commercial Loan Structuring

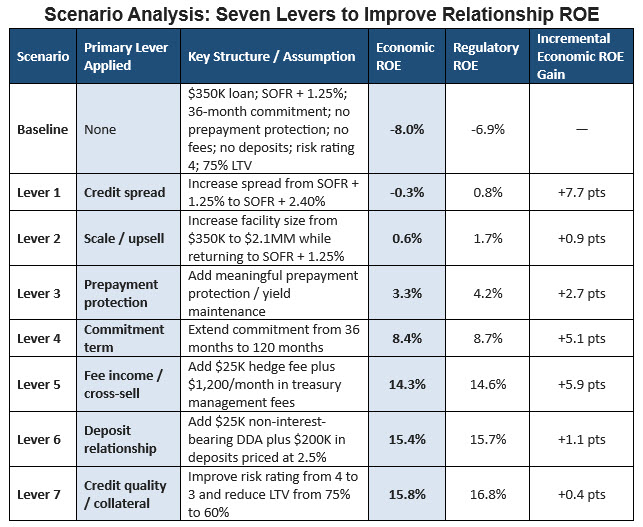

Risk-Adjusted Return on Capital (RAROC) analysis is the cornerstone of sound commercial lending decisions. We priced this specific loan for the banker using our Loan Command application and examined a progressive scenario analysis demonstrating how relationship managers can transform an unprofitable baseline transaction into a highly attractive credit facility if cross-sell, upsell, and structuring strategies exist to create a full banking relationship. The analysis shows that a loan initially generating a -8.0% economic ROE can be restructured to deliver 15.8% Economic ROE and 16.8% Regulatory ROE – a 23.8 percentage point improvement – when systematically applying relationship and structuring levers.

The Baseline Problem: Small, Vanilla Loan Transactions Destroy Value

To build commercial loan profitability, the analysis begins with a sobering reality that every commercial banker must internalize not all loans create shareholder value. The community bank’s average loan size is typically an unprofitable piece of business. Our baseline scenario examines a $350,000 commercial loan (average loan size for this bank) priced at SOFR + 1.25% (aggressive pricing) with a 36-month commitment (average commitment for this bank), no prepayment protection (common for most banks), no ancillary fee income, and no deposit relationship. The borrower carries a risk rating of 4 with 75% LTV.

The above-described transaction produces an economic ROE of -8.0% and a regulatory ROE of -6.9%. In plain terms, the bank would be better off not making this loan. And our community bank is using averages to sense that this loan is not profitable – a correct assumption, except this loan is not the bank’s average loan. The capital consumed by the facility earns less than the bank’s cost of equity, meaning the transaction destroys economic value.

The 7 Levers to Commercial Loan Profitability

Small loans carry fixed origination, underwriting, and servicing costs that cannot be spread across a meaningful principal balance. Additionally, most of the bank’s loans have short commitment periods and even shorter expected lives, thereby shortening revenue earning potential of the credit. Thin credit spread provides inadequate compensation for expected losses, unexpected loss provisions, and the operational burden of maintaining the relationship. This scenario represents the “commodity lending trap” that erodes franchise value over time.

The graphic below summarizes the levers that community banks can use (and measure) to build commercial loan profitability, when the credit spread lever is not available for competitive purposes.

Lever 1: The Credit Spread

Lever 1: The Credit Spread

The first improvement when you want to build commercial loan profitability is straightforward: increase the credit spread from SOFR + 1.25% to SOFR + 2.40%. Holding all other variables constant, this 115-basis point spread increase improves economic ROE from -8.0% to -0.3% and Regulatory ROE to 0.8%.

Unfortunately, the client already has a 1.25% credit spread and, like most clients, is rate sensitive to his large mortgage. While increasing the credit spread to the bank’s minimum improves ROE, the transaction is still only breakeven, and it highlights an important lesson. Credit spread pricing alone cannot transform an economically challenged structure into an attractive opportunity. Relationship managers who rely solely on spread negotiations will find themselves perpetually fighting for marginal deals. The real value creation lies elsewhere.

Lever 2: Scale and The Power of Upselling

The third scenario demonstrates the transformative impact of loan size. This specific loan is much larger than this community bank’s average loan. By increasing the facility from $350,000 to $2.1 million while returning to the original SOFR + 1.25% spread, economic ROE jumps to 0.6% and Regulatory ROE reaches 1.7%.

This 8.6 percentage point improvement in Economic ROE comes entirely from scale. Fixed costs are now distributed across a larger revenue base, and the relationship consumes capital more efficiently. The message for relationship managers is clear: pursuit of appropriately sized facilities aligned with client needs and capacity should take priority over accumulating numerous small transactions. Quality and scale outperform volume in RAROC-driven organizations.

Lever 3: Prepayment Protection and Extending Yield

Adding a meaningful prepayment provision to the $2.1 million facility further improves economic ROE to 3.3% and Regulatory ROE to 4.2% – an incremental gain of 2.7 and 2.5 percentage points, respectively.

Prepayment protection is among the most under-utilized structuring tools in commercial banking. When borrowers refinance or prepay facilities early, banks lose anticipated interest income and must redeploy capital in potentially less favorable rate environments. Yield maintenance provisions (especially) ensure the bank captures the economic value it has underwritten. Importantly, sophisticated borrowers understand and accept these provisions as standard market practice for committed and aggressively priced facilities.

Lever 4: Commitment Term and Extending Duration

Lengthening the commitment from 36 months to 120 months (10 years) while retaining yield maintenance produces the analysis’s most dramatic single improvement. Economic ROE rises to 8.4% and Regulatory ROE to 8.7% – an increase of 5.1 and 4.5 percentage points, respectively.

Extended commitments benefit banks through multiple channels. First, origination costs are amortized over a longer revenue stream. Second, longer expected asset life improves net interest margin contribution. Third, committed facilities of longer tenor often command premium pricing. The scenario notes indicate this structure carries a 77-month expected life versus 21-28 months for shorter commitments – nearly quadrupling the effective duration of the revenue stream.

Relationship managers should recognize that term extension is not merely client accommodation; it is a value-creating structural element that merits explicit pricing consideration.

Lever 5: Fee Income and Cross-Sell Imperative

While the customer was adamant about not paying loan origination fees, layering $25,000 in upfront hedge fees plus $1,200 per month in treasury management (TM) fees onto the 10-year structure elevates Economic ROE to 14.3% and Regulatory ROE to 14.6% – an incremental contribution of 5.9 percentage points each.

This represents the largest single step-up in the entire progression and validates the strategic emphasis banks place on ancillary product penetration. Fee income is particularly valuable because it typically requires minimal incremental capital allocation while contributing directly to pre-tax profit. TM relationships also deepen client dependency, reducing attrition risk and supporting the durability of the overall relationship economics.

Commercial bankers must view loan origination as the entry point for comprehensive financial services delivery, not as an end in itself. The RAROC framework makes this imperative mathematically explicit.

Lever 6: Deposit Relationships

Adding a deposit relationship consisting of $25,000 in non-interest-bearing demand deposits (DDA) and $200,000 in deposits paying 2.5% contributes an additional 1.1 percentage points to both Economic and Regulatory ROE, reaching 15.4% and 15.7%, respectively.

Deposits represent low-cost, stable funding that directly reduces the bank’s effective cost of funds for the loan relationship. The non-interest-bearing component provides particularly high-value funding. Beyond the direct economics, deposit relationships create operational stickiness and provide valuable information about client cash flows that can inform credit monitoring.

Lever 7: Credit Quality and Collateral Reduces Capital Requirements

The final scenario (reflecting the specifics of this loan instead of the community bank’s average credit) improves the borrower’s risk rating from 4 to 3 and reduces loan-to-value from 75% to 60%. These enhancements lift economic ROE to 15.8% and regulatory ROE to 16.8%.

Better credit quality and stronger collateral coverage reduce both expected loss provisions and economic capital allocations. While bankers cannot manufacture credit quality improvements, they can prioritize pursuit of higher-quality borrowers and structure transactions with conservative collateral margins. The incremental benefit here is modest 0.4 percentage points for economic ROE, but it represents risk reduction without corresponding return sacrifice.

Summary and Implementation

The cumulative lesson from this RAROC progression is profound. Starting from a value-destroying baseline (average loan), the systematic application of seven relationship and structuring levers transforms a -8.0% Economic ROE transaction into a 15.8% return – comfortably exceeding typical cost-of-equity hurdles.

Bankers should approach each client opportunity with a structured framework:

- Right-size the facility to client needs and bank efficiency thresholds.

- Incorporate prepayment protection as standard practice.

- Extend commitment terms where appropriate for the client’s business model.

- Lead with ancillary products, particularly treasury management and hedging.

- Capture deposit relationships as a condition of favorable credit terms.

- Prioritize credit quality through disciplined client selection and conservative structuring.

The data makes clear that transactional, product-siloed banking leaves substantial value unrealized. Relationship-oriented strategies, quantified through rigorous RAROC analysis, consistently outperform.