How to Price Fixed vs. Floating-Rate Loans

We talk to thousands of lenders across the country each month about structuring and pricing loans. We have never fielded so many questions and debates surrounding pricing differential between fixed versus floating-rate loans. We believe that this development is primarily driven by the uncertainty of the future path of interest rates (a perennial issue for bankers) but also because many banks do not measure the RAROC (risk-adjusted-return-on-capital) for fixed vs. floating-rate assets, and, specifically, because almost no loan pricing model measures prepayment speeds and embedded optionality of fixed-rate loans vs. floating-rate loans. In this article we will highlight what our research demonstrates for pricing various commercial loan structures.

Borrower Considerations

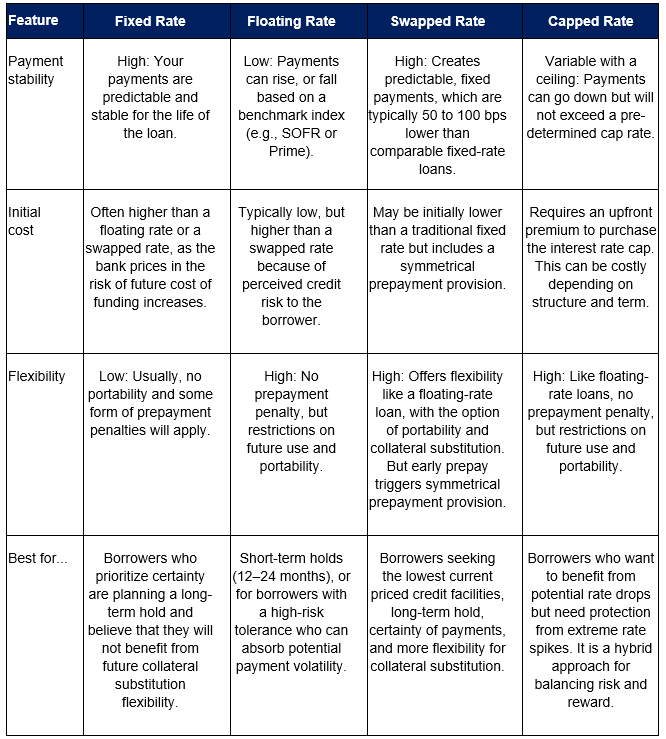

Borrowers have specific financing needs, novel business strategies, and individual market outlooks. When making a loan structuring decision, adept borrowers will weigh their market expectations, transaction costs, risks of being wrong on assumptions, capital costs, leverage risk, and desired hold periods. Many borrowers will have access to loans priced on a floating index and fixed rate, and many will also have access to swapped or capped loans.

There is no single best option for a borrower, and the ideal choice is the one that best aligns with the client’s business goals and financial strategy. Some of the key considerations for the client are as follows:

- Holding period: A shorter timeline of 1-2 years makes a floating-rate or capped rate a more attractive option.

- Market outlook: Most informed borrowers do not forecast future interest rates but rely on market expectations. This expectation is best expressed by fed funds futures and the swap curve.

- Risk tolerance: Seasoned borrowers consider their property/portfolio and the free cash flow’s ability to accommodate rising or volatile P&I payments. More conservative borrowers or properties or projects with more volatile NOI/EBITDA will favor fixed or swapped rates, while those with higher risk tolerance may choose floating-rates.

- Cash flow sensitivity: Sophisticated borrowers measure their business or property free cash flow sensitivity to interest rate movements. Businesses with tight profit margins, insensitivity between cash flow and interest rate movement, or less liquidity prefer the stability of a swapped or fixed-rate loan.

A summary of the borrower’s options and benefits/costs is shown in the table below.

Let us assume that the lender’s goals are three-fold: 1) making the right loan for the borrower’s expressed need, 2) safeguarding the bank’s financial position (including ALCO, income, credit, and sales needs), 3) generating a RAROC sufficient for shareholders. Goal number one is outlined above based on borrowers’ considerations. Goals number two and three can be analyzed using different methods. But we will consider a number of ways that community banks should analyze their commercial loan structuring preferences.

Lender Considerations

Pricing On the Curve

A community bank should be indifferent to a floating-rate and fixed-rate loans if both are priced at the equivalent credit spread, and assuming no embedded optionality exist to allow the borrower to prepay the floater when rates rise, extend the fixed rate when rates rise or prepay the fixed rate when rates fall. In the long run, without this embedded optionality, banks should be indifferent to equally priced (on the same yield curve) fixed or floating-rate loans.

Eliminating Embedded Optionality

Most community banks’ cost of funding is highly correlated to shorter-term rates, and banks generally prefer shorter loan duration – that is floating, adjustable, or fixed rates of up to one to two years. The entire banking industry COF correlation to Fed Funds is almost 90%. When banks offer commercial fixed-rate loans, borrowers are motivated to extend duration for as long as possible during periods of rising interest rates and refinance the loan when interest rates fall – this loan structure is called a one-way floater.

There are three steps that community banks can take to counter this one-way floater and the resulting dilution of return for the bank:

- Banks are well served to include and enforce a strong prepayment provision where it makes sense to do so. If interest rates fall the bank will minimize the loss of an earning asset. Prepayment provisions not only protect banks against one-way floaters, but they also increase stickiness and cross-sell and upsell opportunities for banks.

- But prepayment provisions do not help banks with fixed-rate loans when interest rates rise (margin continues to contract). To counter this erosion in ROA/ROE banks must charge a premium for fixed-rate loans. This risk premium will depend on volatility in the market, inflation risk, type of borrower and loan category, but in summary this premium has historically been 50 to 75bps over the equivalent floating rate.

- Since it is impossible to consistently outwit the market – equity, debt, or any other highly active market, neither the borrower nor the lender can be certain that we are entering a declining or increasing interest rate environment – especially over multiple years. Many community banks eliminate the one-way floater by offering their borrowers the ability to fix the loan rate from 3 to 20 years through a hedge. The hedge not only solves this issue but results in a stickier relationship and can generate substantial hedge fee income. Most regional and national banks view this as the preferred solution rather than charging a risk premium on the loan (for highly desired client) or trying to enforce a prepayment provision with its attendant reputation risk.

Forecasting Prepayments and RAROC

Few community banks measure RAROC for commercial loans, and almost none measure forecasted prepayment speeds based on structure and prepayment provisions. However, almost all national banks are doing this analysis. Our research shows a clear and direct relationship between loan prepayments and RAROC. There are five main reasons why prepayment provisions increase profitability for banks, as follows:

- Decrease the value of the option held by the borrower to repay the credit when interest rates or credit spreads are lower.

- Increase the lifetime value of the relationship.

- Increase cross-sell and upsell opportunities.

- Reduce negative selection bias in an economic downturn.

- Reduce the cost of having to replace loan prepayments with new, more competitively priced, loans.

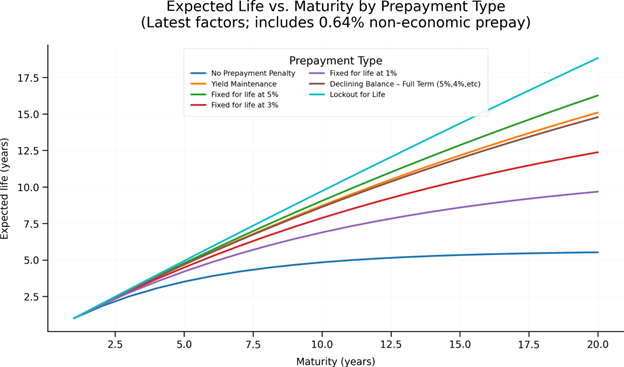

Floating-rate commercial loans prepay faster than fixed-rate commercial loans: at some banks, the prepayment speed of floating-rate loans is twice the speed of fixed-rate loans. The issue is that floating-rate loans are self-selecting to temporary financing vehicles and it is almost impossible to embed prepayment provisions for floating-rate commercial loans. Our analysis below shows expected life of a loan based on contractual maturity, using various prepayment provisions and assuming 0.64% pa non-economic prepay. Without prepayment provisions, floating-rate loans rapidly prepay (note the bottom line labeled “No Prepayment Penalty”).

Key takeaways from this analysis is that floating-rate loans do not benefit from prepayment provisions and have a shorter expected life. Therefore, these loans are less attractive for banks, all else being equal. Fixed-rate loans with strong prepayment provisions increase RAROC for lenders. When we calculate the impact on same loan RAROC floating versus fixed with strong prepayment provisions, the variance is between 2.9% and 14.4% depending on loan size, credit quality and loan category. We assume in our modeling that contractual prepayment provisions are enforced, but with the inclusion of carveouts and exceptions to the prepayment provision, RAROC returns can be much lower than anticipated for certain prepayment types.

Conclusion and Application

There is no same right answer for every financing situation. However, lenders can enhance RAROC and safeguard their bank’s financial positions by applying the right structure and prepayment provision for their specific borrower. The right prepayment provision and structure can increase the ROE on a relationship, keeping credit spread constant. The case for community banks to prefer long-term credit facilities with strong prepayment provision is unequivocally sound.