Why Banks Should Require Single-Close Construction-Through-Perm Loans

Every commercial lender knows the feeling. The bank took the hardest risk on a project – the construction phase. The bank managed the draws, monitored the budget, inspected the site, and shepherded the borrower through permitting delays and cost overruns. Then, just as the project stabilizes and the loan finally becomes easy to hold, the borrower announces that another lender is offering a better fixed rate on the permanent financing. The bank is now negotiating against the market to keep a loan it already earned, and it is negotiating from weakness.

At least monthly, we come across the above scenario with the banks that we consult with. Most recently, a lender informed us about a customer with a floating-rate loan the bank had closed two years earlier at SOFR plus 2.40%. Now, with the project completed, the borrower wants a fixed rate of 6.00% or less and made clear that he could get it from another lender if he refinanced. The lender’s own conclusion was telling: “we will probably have to give up some spread to keep the loan.” The bank is now faced with lowering its spread or losing the loan.

The Standalone Construction Loan Is a Bad Trade

Construction loans, viewed in isolation, are among the least attractive credit products a bank can offer. The bank typically absorbs three distinct layers of risk: acquisition and permitting risk, construction risk, and lease-up or market risk. Meanwhile, earning only debt-level returns. The loans are short, typically six to twenty-four months, yet they demand intensive administration: draw management, inspections, budget reconciliation, and lien monitoring that can cost more than $2,100 per month, roughly two to ten times the servicing cost of a comparable commercial real estate loan. Because funds are drawn over time, average utilization runs only 50–60% of commitment, suppressing interest income. Loan pricing models consistently show that the return on equity at origination is negative even with a 1.00% origination fee, and many banks understate the problem by omitting the construction timeline and average utilization from their pricing altogether.

The economics only work if the bank keeps the loan after stabilization. On a risk-adjusted return on capital (RAROC) basis, a standalone one-year construction loan may produce a 3% risk-adjusted return or even a negative ROE, while the same loan paired with a ten-year fully amortizing permanent takeout can drive the average return to 15–18%, while simultaneously presenting a lower default risk and more cross-sell opportunities. The permanent phase is where acquisition costs are amortized, where customer lifetime value accrues, and where the loan finally becomes the low-maintenance, profitable asset the bank underwrote in the first place.

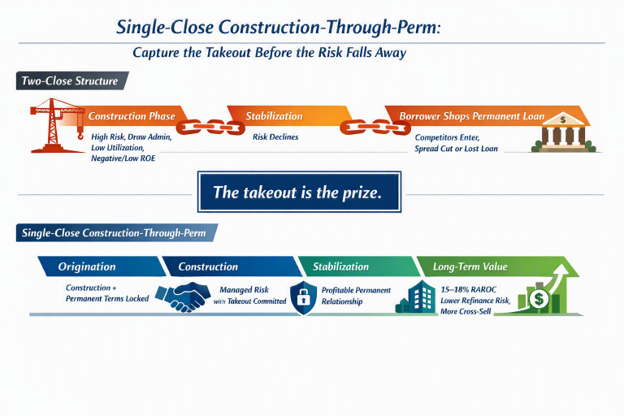

The Takeout Is The Prize

Here is the structural problem with letting the borrower negotiate the term loan after construction: the moment the certificate of occupancy is issued, the risk profile of the credit transforms, and so does the competitive landscape. Insurance companies, national banks, credit unions, and conduit lenders, the institutions that deliberately avoid construction risk, appear precisely when the risk has been wrung out of the deal. They offer aggressive long-term pricing on a stabilized, cash-flowing asset, and they can do so because they paid none of the costs of getting it there.

The originating bank is left with the worst of both worlds. If the borrower leaves, the bank held the high-risk, negative-ROE phase and captured none of the profitable tail. If the borrower stays, it is usually because the bank matched or beat the outside offer, which is exactly what happened in the scenario above, where the lender anticipated surrendering spread to retain the relationship. Either way, the borrower’s option to shop the permanent loan is a real economic cost to the bank, and it is a cost the bank granted for free at the initial closing.

Customer churn at stabilization is not an occasional misfortune; it is the predictable outcome of the two-close structure. Post-completion, borrowers rationally shop for the best long-term terms, and the incumbent bank’s only defenses are relationship goodwill and rate concessions. Neither is a strategy.

The Single-Close Construction Loans Fixes the Problem at Origination

A construction-through-perm loan bundles the construction facility and a long-term amortizing permanent facility (with a five, ten, or even twenty-year term) into a single closing, executed with one or two notes before the first shovel hits the ground.

Structurally, it changes everything:

It removes the borrower’s exit option. The permanent facility exists from day one, with pricing, amortization, and covenants agreed while the bank still has negotiating leverage. An embedded prepayment provision (a symmetrical make-whole or step-down structure) discourages the borrower from refinancing the term facility away prematurely, preserving the revenue stream the bank earned by taking construction risk.

It improves credit quality. With the permanent rate locked at closing, the take-out DSCR is underwritten on stabilized cash flow at a known debt service – not on a hoped-for rate environment one or two years out. The borrower is never exposed to the refinancing risk that sinks projects when rates rise during construction, which means the bank is never exposed to it either.

It maximizes customer lifetime value. The high acquisition and servicing costs of a commercial construction customer can only be justified over a long relationship. A two-year construction-only loan delivers low or negative shareholder value to the bank. But a twelve-year construction-plus-perm relationship amortizes those costs, captures a decade of interest income, and anchors deposits, treasury management, and future lending.

Borrowers Want Single-Close Construction Too

Requiring the single close is not an anti-borrower policy. If properly presented, it is a better product. The borrower locks the permanent rate before breaking ground, eliminating the single largest financial uncertainty in any development. One closing means one set of legal, title, appraisal, and documentation costs instead of two – a saving that commonly runs into five figures on mid-sized commercial projects. And the borrower mitigates the risk of failing to qualify for takeout financing if the market, the property, or the borrower’s own financials deteriorate during construction. Rate certainty, cost savings, and execution certainty are genuine value, and banks can legitimately price for delivering all three in one package – a niche most large competitors, who avoid construction lending entirely, cannot match.

Conclusion: Make It Policy, Not Preference

Some bankers still assume shorter commitments mean lower risk. The evidence says otherwise – for senior-secured, amortizing real estate credits, the longer combined commitment lowers total risk while multiplying return.

Banks should therefore make the single-close construction-through-perm structure a requirement of construction credit approval, not an option the borrower may decline. Price the construction phase honestly, embed the forward-starting fixed rate and prepayment protection at closing, structure around known future events like tax-credit paydowns, budget and time overruns, and capture the relationship when the leverage is yours.