The Terminal Fed Funds Rate – How Far Will The Fed Go?

Last week the Federal Reserve again raised the Fed Funds rate by another 75 basis points – and again, that was in line with the market’s expectation. The question is when will the Fed stop, and what will be the terminal Fed Funds rate? We do not believe that the Fed’s “dot plot” fully reflects the amount of additional tightening that is required to bring inflation to the central bank’s desired 2.00% level. The debt and equity markets reacted to the glaring disconnect in the Fed’s forecasts by selling off aggressively. We believe that the Federal Reserve is misjudging the anticipated tradeoff between short-term interest rates and inflation trends. If that is the case, banks should be ready for an environment where short-term rates are higher for a substantially longer period.

Neutral Rate in Relation To the Terminal Fed Funds Rate

The neutral rate is the theoretical federal funds rate at which monetary policy is neither accommodative nor restrictive and is consistent with the economy maintaining full employment with associated price stability. Even though the Fed has now raised its anticipated terminal Fed Funds rate (substantially), the rate is still not consistent with monetary policy being neither contractionary nor expansionary. To lower inflation, the Fed must bring short-term interest rates above the current inflation rate and keep them there for some time. When short-term interest rates are below the inflation rate, monetary policy is stimulative, further fueling inflation.

There are two variables that interplay when monetary policy is restrictive, the first is how much the Fed Funds rate exceeds inflation, and the second is for how long. The higher the Fed Funds rate exceeds inflation, the shorter the required period to lower inflation. The downside is that highly restrictive rates are not conducive to a soft landing, and the central bank would prefer a slightly restrictive monetary policy for longer to minimize damage to the economy.

Unfortunately, the Fed’s own projections do not show that monetary policy will become restrictive.

Feds Projections

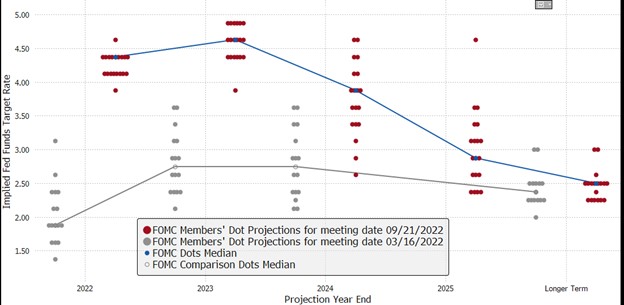

The graph below shows the FOMC member’s projected target Fed Funds rates from the September and March 2022 meetings. Over the six months, the members have concluded that the terminal rate must be 2.00% to 2.50% higher to tame inflation. The central bank is moving in the right direction, but there still does not appear to be enough monetary tightening to ease inflation concerns. Short-term rates will likely have to rise beyond 5% until real interest rates are positive.

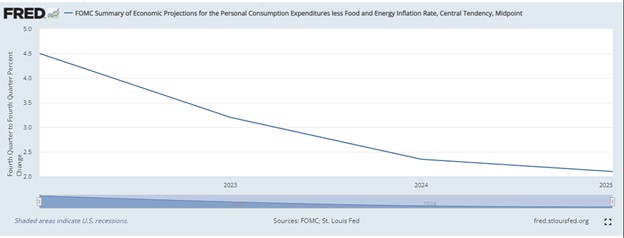

The graph below shows the members projected core PCE rates from 2022 to 2025. Coupling the projected Fed Funds rate and core PCE rates, the Federal Reserve believes that it can lower inflation without creating positive real interest rates. It seems either dubious or disingenuous to suspect that the Fed can keep short-term rates at or slightly below the inflation rate at the end of 2022 and still cause core PCE to drop 1.50% in less than one year.

Banks Should Expect a Higher Terminal Fed Funds Rate

It appears that the Federal Reserve would like to keep interest rates under a highly restrictive territory. If so, they will need to keep short-term rates elevated for longer. There are many reasons not to believe the tame inflation narrative in the next few years. Real interest rates are still expected to be negative, and this will result in an extended inflation battle. Also, the Fed will do what it can to avoid the Volcker policy mistake of the late seventies and early eighties. The Fed will want to avoid vacillating on monetary policy. During the Volcker inflationary period, the Fed raised rates to 20% to tame inflation but then lowered rates to 9% during the recession that followed, only to recognize that inflation was not quashed by the recession and higher unemployment. Each Fed zig-zag prolonged the inflationary environment.

Application for Community Banks

The Federal Reserve is conducting a long-term battle against inflation, which they are prolonging with continued negative interest rates. The terminal Fed Funds rate for this cycle will likely be higher than the 4.50% the current market expects. Community banks should be positioning their business models to anticipate the following:

- Deposits will decrease, and the cost of funding earning assets will increase;

- A flattening or inverted yield curve will put pressure on bank earnings;

- Banks will have unrealized losses in their investment and loan portfolios due to fixed rate exposure;

- Cap rates on real estate will increase, and real estate collateral values will decrease;

- Free cash flow for many borrowers will decrease as poor business models become challenged;

- As banks tighten underwriting policies, bubbles will burst with knock-on effects for suppliers and customers;

- Debt coverage ratios will be challenged for lesser-quality obligors; and

- Fee income will become more important in a higher-for-longer interest rate environment.