AI Competition: How OpenAI and Anthropic Just Changed Bank Strategy

While AI can help banks, this month it is more like AI competition. Earlier this month Anthropic released its “Claude for Small Business” suite of agents and ChatGPT introduced its new personal finance experience which connects users’ financial institutions to allow them AI-generated insights. This infrastructure is quickly changing the financial landscape. In this article, we break down what these new tools mean for bank strategy and how your bank could position to fight.

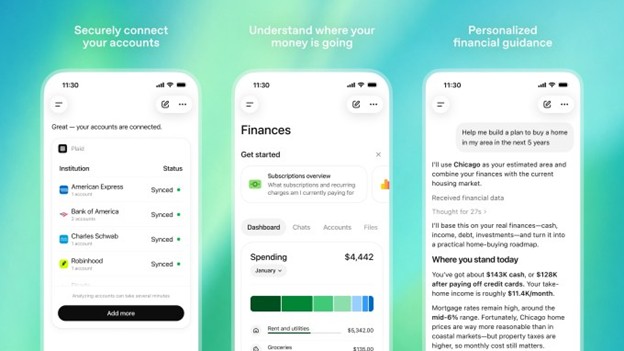

OpenAI’s New Personal Finance Functionality

For users with OpenAI’s Pro model ($20 per month), users connect their instance of ChatGPT to their financial institutions via Plaid. The logic from OpenAI is that they see more than 200 million personal financial questions every month, why not connect to the banks for more informed answers based on real-time data?

For the user, having all your financial information in one place that you can query and ask questions with an AI layer makes immense sense. There are other financial apps that do relatively the same thing, but the fact that it is integrated with your main LLM gives you some distinct advantages.

Sure, connecting ChatGPT or Anthropic increases your security and privacy surface but likely this is within the acceptable risk tolerance of many. Plaid has bank-grade encryption and has never been hacked. Connecting your LLM to your finances does create another vector to a non-regulated company but this is little different than all the ERP and personal financial applications that are already well used. While this is debatable, one could argue that when it comes to privacy and security, the resources and motivation of an OpenAI, Anthropic or Plaid is greater than your average fintech or community bank and likely safer.

AI Competition From a Banking Perspective

For the banking industry’s perspective, the rise of this technology is a different story and presents material AI competition. With this move, banks are being disintermediate and losing control of the customer.

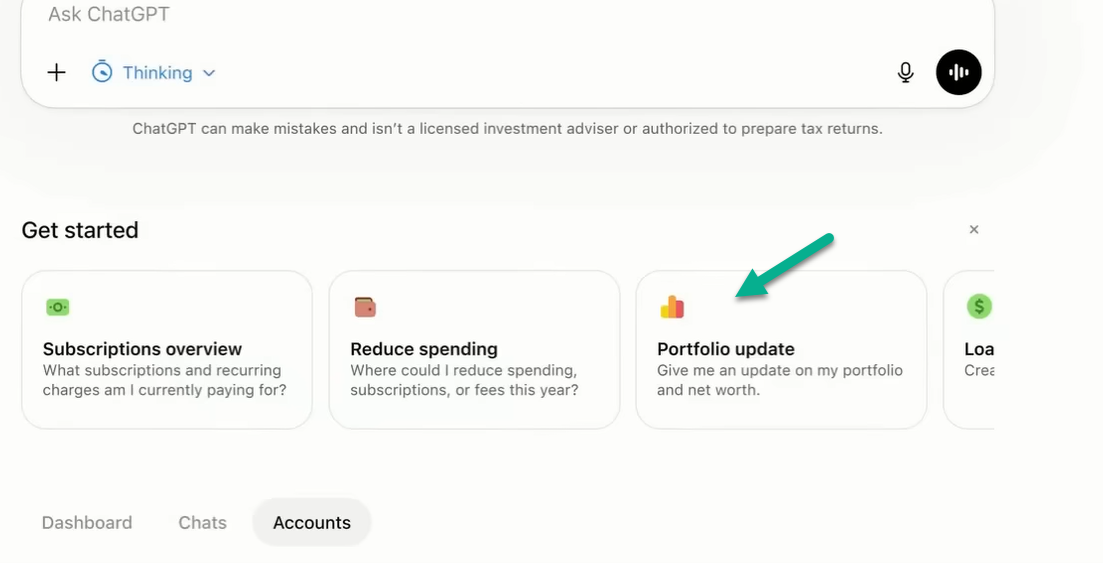

Both OpenAI and Anthropic’s tools come with a variety of prebuilt functionality (below) which helps the user get started.

Users can then ask any questions they want such as:

- Put a wealth management plan together.

- Create cash flow projections.

- Analyze loan structures.

- Analyze my transactions and highlight where discretionary spending can be reduced vs. benchmarks.

- Forecast my ability to make payroll in my business.

- Optimize my banking relationships and cash holdings.

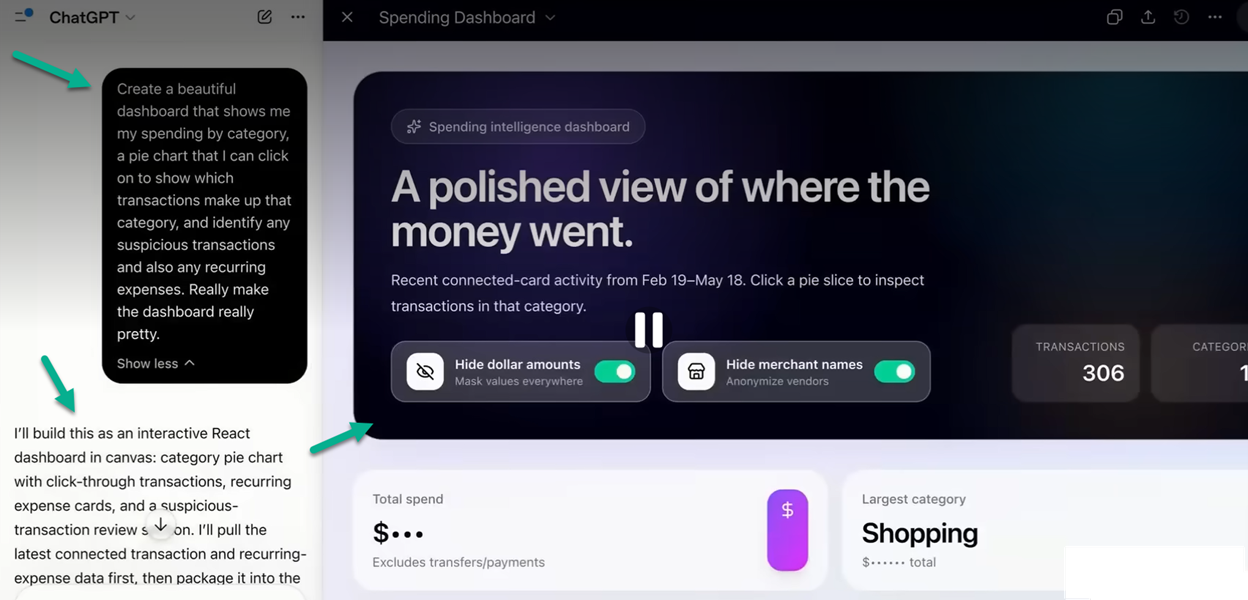

Not only can users ask questions, but users can vibe code any widget they would like for their specific purpose. The example below is a simple dashboard with the ability to turn on and off dollar amounts and merchants so we can demo the application live. However, we have created other applications that just focus on fraudulent transaction monitoring, market monitoring for suggested investment portfolio rebalancing, and foreign exchange monitoring that highlights U.S. dollar transaction that go overseas where a company might be able to save money by doing the currency translation with their domestic bank.

This AI functionality presents some stark lessons on how to strategically compete.

Below are our five insights:

Insight 1: The Loss of the Application Layer

The biggest AI competition lesson here is the execution of what banks, fintechs, and software firms have been fearing. With one set of releases, these new personal finance function signals a major shift for banks, warning them that they risk being reduced to underlying infrastructure while AI platforms own the customer relationship. By letting users link over 12,000 financial accounts, these LLMs are transforming into a conversational AI layer that sits directly on top of everyday financial data.

Where banks and fintechs have built this application layer, it is now abstracted and no longer under control of banks. Banks are being reduced to data providers very quickly.

Insight 2: There is Room to Compete – Ambient Over Interactive

In our tests, about 15% of the data or insights uncovered by these applications were inaccurate or incomplete. In some cases, we found OpenAI just made-up transaction data which is disconcerting and undermines trust. In other cases, it provided less than optimal advice based on information that it had but ignored such as our stated goals.

Then there is this issue of the user interface and after using these applications for a week, it got tiring of always having to prompt for questions and then having to refine. If you are connected to your child’s or senior parent’s account, you must constantly monitor and prompt to remove from your data and analysis.

For fintech and banks that want to compete, creating a professional grade application and then layering an AI chat bot to further query the data and derive insight will be the winning user interface similar to how many health apps do it today such as the Oura ring, a health-focused wearable.

Chat works well for open ended queries like search but is suboptimal in other categories of questions where the context is broadly familiar but not specifically clear to the user. In focus groups, most bank customers desire their data to be flagged when it’s off with the bank focusing on how to fix it. Banks can use AI, for example, to flag potentially fraudulent transactions and then create an easy path to help investigate and correct. In other words, bank customers want an ambient over an interactive interface.

Instead of the traditional data => output => action model, banks need to shift to more ambient thinking where AI assists with observation => insights => anticipate => automated action approval. In the future, bank customers will interact with bank provided models less and have more experience with the bank systems running in the background.

All that said, this is the first release and likely the worst this functionality is ever going to be which doesn’t bode well for the longer term for financial institutions.

Insight 3: Vendor Decisions

Moving forward, there is a whole swath of financial functionality that will likely move to agentic AI. Personal and small business financial management is just the start. Performance dashboards, document management, tax reporting, onboarding, AML/KYC, and array of other applications should see competition from the frontier LLM models.

Before a bank spends $300k+ for integration and lock themselves into a three-year contract with functionality from their core provider or a fintech, it is worth asking the question internally around how long before the frontier LLM models duplicate the application?

Insight 4: Expertise Matters

The frontier models will likely stick to generic applications for the near future. Strategically, this means banks should consider more of a focus on more of a segmentation strategy and provide this functionality with a higher level of industry-specific analysis. Humans on top of more detailed analysis is what will set banks apart in the future.

Insight 5: The Execution and Relationship Moat

While account opening and payment execution will eventually go to agents, there are still many hurdles with authorization, validation, and liability. The near term means that these frontier LLMs will focus on analytics and advisory.

This leaves some space for banks to focus more on execution to including moving money, placing trades, settling accounts, complex advisory and putting credit in place. Bank relationships matter more than ever. Banks need to rethink how and when to use their bankers to deliver more sophisticated, accurate and nuanced advisory.

Further, to avoid losing their customers’ trust and attention to these LLMs banks should prioritize offering their own AI-driven solutions that harness real-time market data and other account information not available on Plaid.

Battling Against AI Competition

AI competition is now real and will get tougher. The broader message for banks is clear: AI will continue to compress the value of generic financial applications, but it does not eliminate the importance of trusted execution, specialized expertise, and strong customer relationships. Institutions that move quickly to embed AI into purposeful, bank-led experiences rather than treating it as a standalone feature will be better positioned to defend relevance, deepen client value, and compete effectively in the next phase of financial services.

To learn and discuss more about how AI is both helping AND hurting banks, come to our Elevate Banking Forum in the beautiful Wild Dunes Resort in the Isle of Palms, SC, on September 21 – 23. Register HERE.