Use This Framework for Better Bank Innovation

Every bank wants to be “innovative,” but the truth is innovation is difficult. Add to that a bank’s resource constraints, compliance demands, budget goals, legacy IT infrastructure and talent gaps, and innovation for a bank is extremely difficult. When it comes to bank innovation, it pays to have a methodology in which to think about product design and improvement. In this article, we explore the Innovation Matrix and how to use it to better drive your bank’s efforts.

The Problem of Bank Innovation

In addition to the above bank constraints, one drogue chute that banks carry around is the lack of an innovation effort. Many banks don’t think in terms of innovation and are not set up for innovation. The kneejerk reaction is forming an innovation committee that often only compounds the problem. The larger the committee, the more banks will succumb to the lowest common denominator and the less innovative they will be.

Without an innovation plan, banks often rely on vendors and their core providers for innovation. This might be fine for some products and product improvements, but banks cannot rely solely on outsourcing innovation. Every bank, no matter the size, should think and train bankers on where, and how to look for improvements.

Innovation is a muscle that needs to be exercised often, less it atrophies.

Framing Innovation

From a 30,000-foot level, there are two main types of innovation for banks. There is radical innovation and incremental innovation. Radical innovation is a product or process that has never existed before that meets a completely new need. The iPhone, Uber, and Airbnb all fall into this category as does the ATM.

Incremental innovation, on the other hand, is the small, but meaningful, improvement process on an existing product. 98% of bank innovation falls within the incremental improvement category which is about how it is in other industries. Incremental improvement is lower risk, more customer feedback-driven, and is a surefire way to increase revenue, improve engagement (customer lifetime value), and cut costs.

It doesn’t matter what category of innovation your bank is going for, there are some steps you can take to make the process less daunting and more achievable. Utilizing an innovation framework can help products and services take shape faster and in a more organized fashion.

Focusing on Total Experience When It Comes to Bank Innovation

At the core of all great innovation is the goal to improve the Total Experience. Innovation requires serving the customer AND employee needs more effectively than your competitors. While most companies just focus on the customer, top-performing innovative banks know that the employee is a central part of that equation.

Innovation should always be about bridging a clearly articulated need with the next best alternative that is currently in the marketplace. Innovation is much more than just new technology and encompasses a combination of product design, pricing, and marketing.

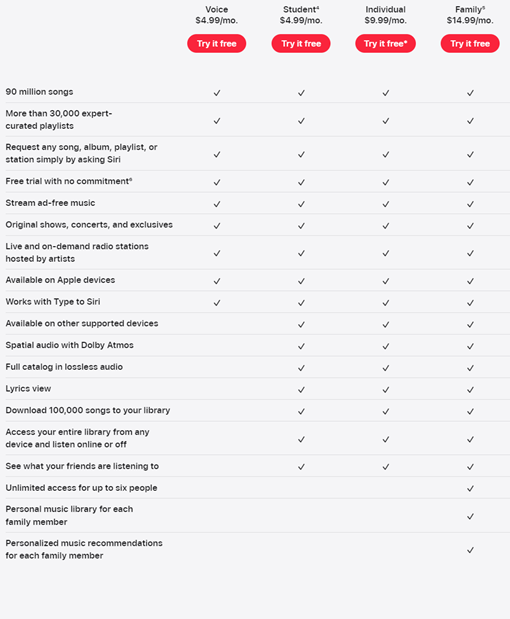

For example, for innovation to be successfully adopted, it must provide a greater utility than what is being charged. While making 90 million songs available in Apple’s music streaming service was innovative, the overlooked aspect of this product was how it priced the product on a bundled basis and in such a way that you wanted to sign up your entire family for the product thereby generating Apple the most revenue.

In focus groups, households thought they were getting at least $25 per month of value for Apple’s $14.99 charge. The product, combined with the pricing structure, help propel Apple to over $4B in revenue and 100 million subscribers. When the right product, meets the right unfulfilled need at the right price, success is sure to follow.

To start the innovation process, it helps to think in terms of the 2 x 2 innovation matrix.

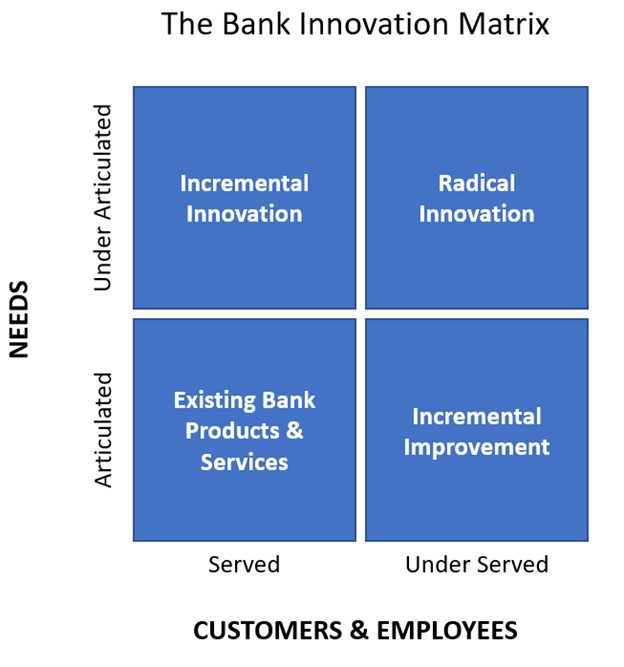

The Bank Innovation Matrix

When it comes to innovation, you need to start with your customers and employees. Design a two-by-two matrix with “Served” and “Unserved” across the bottom, or X-axis. Any current product or service idea goes on the left side while new ideas that don’t exist yet go along the right. The more an idea differs from what is being offered, the more to the right it goes.

Along the vertical or Y-axis goes “Articulated” and “Unarticulated” needs. Articulated needs are products your customers and employees are asking for while to the right are ideas that no one is asking for but the bank thinks is a good idea. The more common the need that is being met the lower the product goes.

Most customers need a credit or debit card, it is a common product so any new idea around offering a product that is already common to a customer base that is already well-served would go in the bottom left.

Common products or services that can get slight tweaks, new attributes, or be used for an underserved market, would go to the bottom right and can be thought of as “Incremental Innovation.” This is like McDonald’s offering a healthier menu based around salads, Salesforce moving CRM to the cloud, or the fintech Brex targeting banking products to start-ups with an open banking solution.

Of course, the opposite of a common financial product there is radical innovation to the top right. This is the riskiest category but potentially the most rewarding. This is where we get the iPhone, Airbnb, or the smart contract for payments.

The best banks in the world are constantly innovating. However, few banks, or fintechs, focus on the top right quadrant. Most best-in-class banks are so because of a concerted program around incremental innovation and their ideas fall within the upper left or bottom right quadrants. They are always trying to improve their existing products in small ways to meet underserved needs. In the process, they can drive incredible value.

While Airbnb started off with a radical idea, most of their adoption came after they introduced professional photography (upper left quadrant) so that homes could be more effectively marketed. A couple of years ago, they launched “Experiences” so once you get to your place to stay, you can now enjoy local experiences such as walking tours, boat rides, or local history lessons.

Incremental improvements are not always ground-shaking, but often they provide more customer growth, revenue, and franchise value than radical innovations. Each product improvement usually reduces cost, attracts new customers, enhances engagement, and drops acquisition expenses.

The critical takeaway here is to understand that the more a bank’s customer base grows, the more valuable incremental improvement is as the cost of that improvement is spread over a wider base and improvements can then fuel more than linear growth. The conclusion here is that banks should always be looking for ways to improve their products and solutions as that is the less risky innovation path.

Getting The Tools – 7 Tips To Better Bank Innovation

Incremental innovation can also lay the foundation for radical innovation.

Buy now pay later (BNPL) started off as an unarticulated incremental innovation on both a credit card and a faster check-out procedure. The main innovation here was the real-time creation of credit. By getting the merchant to offer a discount, companies like Klarna, Afterpay and Affirm combined several incremental innovations to produce a whole new credit category.

The matrix can be instrumental in evaluating new ideas for their level of ambition and where it falls in the two-by-two matrix. You can visually see where your products or products of competitors are falling short and not meeting a customer or employee’s need. Highlighting the gaps in needs and then understanding if the need is articulated or unarticulated allows bankers to go out and test the product to see if it relieves a pain point or what is called “jobs to be done” (JTBD) in customer experience parlance.

To put this in motion, here are some suggestions on how to practically use this framework:

- Identify and articulate defined needs of the customer and employee

- Detail a use case or Jobs To Be Done (JTBD)

- Ideate and test against articulated and unarticled needs

- Map ideas on the Matrix – the higher and more to the right an idea is, the more testing required to validate if the product fulfills the stated need

- Seek out JTBD that will improve engagement and adoption

- Seek partners and third-party products that can grow with the bank and have an improvement schedule

- Audit bank products at least every other year for improvement