What Term Lending Index Should Banks Adopt?

Banks have ceased using LIBOR to price assets and liabilities after 2021. However, some community banks are still deciding on the correct term lending index to adopt. Many banks are uncertain that they have chosen the best term index for their products and markets. We believe that having more options for community banks is beneficial. Still, bankers need to streamline the number of indices used because having too many indices is not conducive to efficient pricing and loan and deposit processing. Most banks will need more than one index to allow them to conduct their business. Community banks have used overnight indices such as Fed Funds and Prime for decades, and those are not going away. However, how do banks decide on a term rate between SOFR, Ameribor, and BSBY? After almost four months in the post-LIBOR market, it is time to review each index, how each has fared, and help community banks decide which term index is most suitable for their business model.

Considerations For Choosing A Term Lending Index

There are several parameters that community banks need to consider when choosing an index, as follows:

- The index needs to be published broadly, and its composition and pricing mechanism must be transparent and understood.

- Robustness/Volume. The more entities that use the index, the more likely it will survive stress in the market and the less likely it is to be unavailable when needed in a market meltdown.

- Depth. An index that has more trades and observations is preferred. More trades and contracts create rate validity and accommodate more terms. An index representing overnight rates and term structures is fundamental to community banks that sell products with multiple payment periodicities.

- Validity. An index should be observable and not easily manipulated by market participants.

- Representative. Banks prefer an index that follows their cost of funding. While no public index will move in lockstep with any single bank’s COF, a high correlation coefficient is preferred.

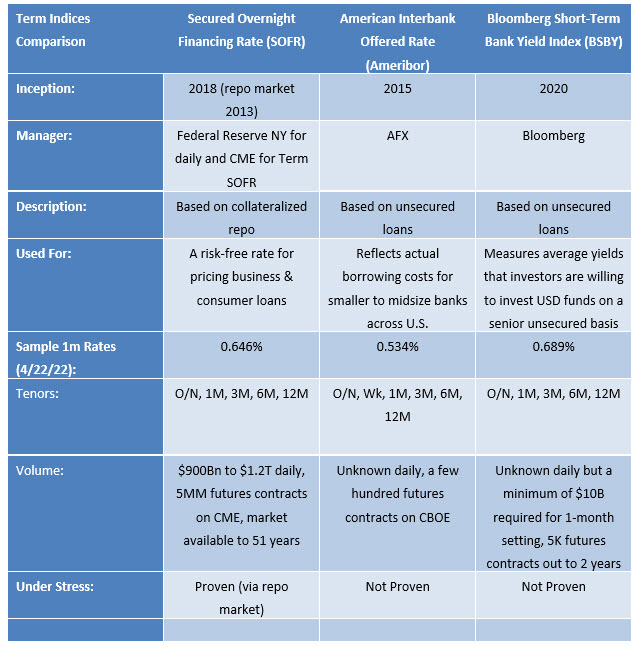

Prime and Fed Funds are overnight rates only, and community banks will continue to use those rates for products suited for daily repricing. There are three term indices available to community banks: SOFR, BSBY, and Ameribor. The comparison between the three is shown in the table below.

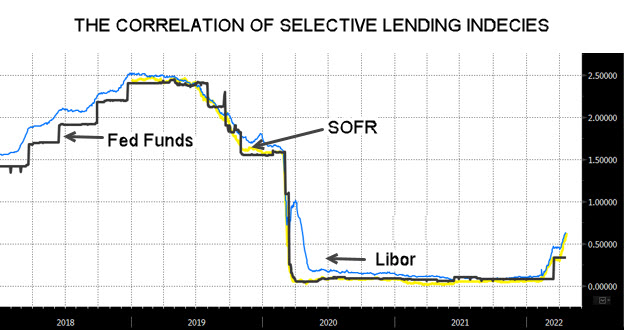

All major indices are correlated, and even overnight rates and term indices are highly correlated. The graph below shows Fed Funds, term SOFR and LIBOR over the last four years (correlation coefficient is close to 0.99 for all three).

The correlation between SOFR, BSBY, and Ameribor is more challenging to show because of the short history and lack of rate movement over that time. However, in the last few months, since interest rates have been rising, all three term indices have been moving in tandem.

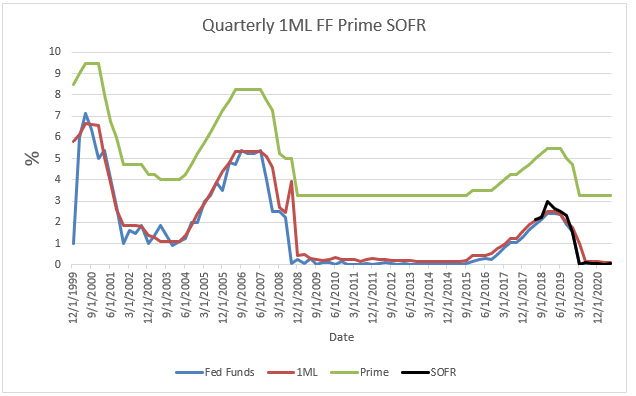

Some bankers have criticized SOFR because it is a risk-free rate (like Prime and Fed Funds) and unlike LIBOR, Ameribor and BSBY. There are a few responses to this criticism. Prime and Fed Funds also do not contain a credit component; therefore, the shortfall of SOFR is not specific to that index alone. The market has not similarly pushed back on using Prime and Fed Funds. All four indexes (Prime, Fed Funds, LIBOR, and SOFR) are highly correlated, as shown in the graph below.

Most lenders can easily price a credit premium over Prime, Fed Funds, and SOFR to get an equivalent credit component inherent in LIBOR, BSBY, and Ameribor. The adjustments between SOFR and LIBOR have been established and published by the Alternative Reference Rate Committee (ARRC). For example, the credit spread adjustment is 11.448bps between 1-month LIBOR and SOFR and 26.161bps between 3-month LIBOR and SOFR.

The real concern for lenders is allowing a borrower to arbitrage the bank – borrow cheaply from the bank when the bank’s cost of funding is rising. This is precisely what happens on lines of credit when banks price these facilities to indexes without a credit component. In times of financial stress in the market, a bank’s cost of using rises, but Prime, Fed Funds, and SOFR would all be expected to fall, making a borrower’s cost of borrowing lower. This is particularly unfortunate since most banks do not charge a standby fee on lines of credit – lenders do not earn any return, potentially until the lender’s COF goes up, and that is when borrowers are more likely to draw.

There is a sound argument for lenders not to use SOFR (or Prime or Fed Funds) for any credit facility without the appropriate credit spread adjustment.

Market Adoption

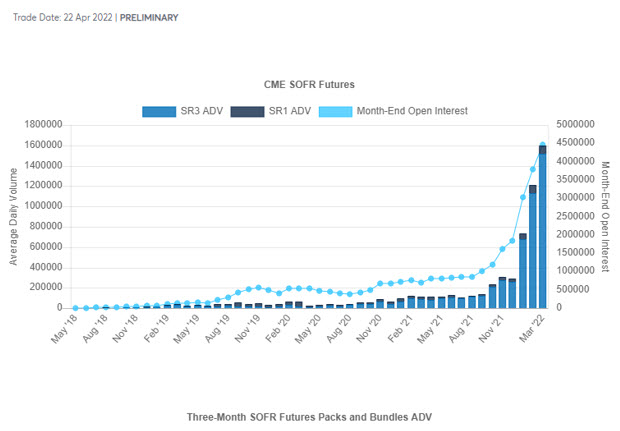

The national and regional banks have been mainly adopting SOFR for loan pricing. Term SOFR futures contracts on the CME are arguably the best gauge of SOFR adoption in the market. A graph showing open contracts on the CME is shown below (or updated HERE). The market for SOFR contracts is much larger than for BSBY and Ameribor (about a thousand times larger).

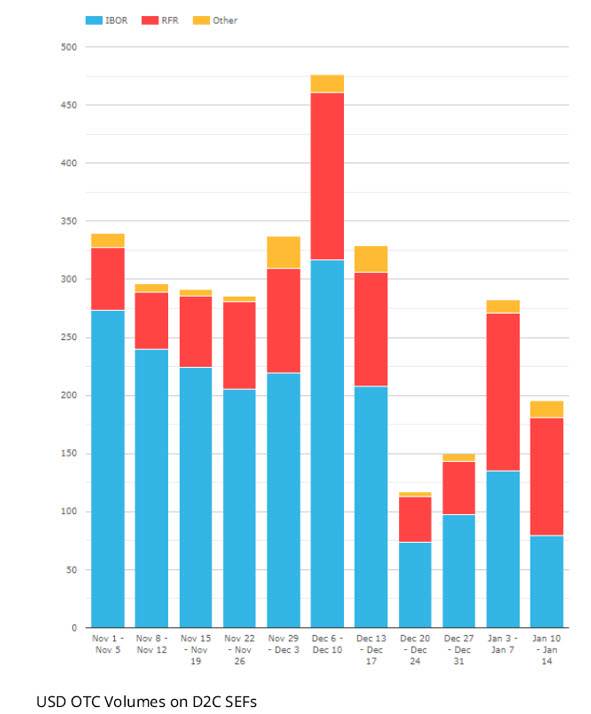

The hedging activity for end-users is shown in the graph and demonstrates that SOFR-based hedging is larger than any other index (IBOR, which includes Fed Funds).

In contrast, BSBY hedging is only approximately 0.4% of the market as of the beginning of this year (as shown in the graph below) and Ameribor hedging is less than that.

Conclusion

Every community bank must analyze its market and product to adopt the term lending index that is best suited for its needs. Regulators are on record stating that banks do not have the luxury of burning time reinventing the wheel when AARC has described a clear transition path for them – term SOFR. As soon as regulators encouraged a forward-looking term SOFR last year, the market rapidly adopted term SOFR as its primary index. This is why term SOFR has the dominant share of the cash, futures, and the hedging market.