How to Use System Thinking To Better Solve Banking Problems

When trying to figure out any problem in banking, including strategic planning, it helps you to understand the system you are dealing with. Oftentimes bankers apply the wrong mental model to a problem and come up with a suboptimal answer. System thinking is the ability to recognize a pattern before you act so that you can better apply the right methodology for solving the challenge. In this age of AI, this is more relevant than ever. In this article, we describe the various types of systems in banking and explore how best to match the system with the solution.

The Importance of System Thinking

A firefighter doesn’t treat every fire the same way. To a novice, you see a fire and you apply water. To an experienced expert, applying water could be disastrous. Before a fire attack plan is put in motion, the fire, smoke, fuel, structure, and environment are analyzed to come up with a plan. The type of fuel, color of smoke, amount of smoke, wind, and surrounding area all play a part in setting a strategy. Open the wrong vent or apply the wrong suppressant, and you end up feeding the fire not stopping it.

Here is another common problem, a banker wants a new account opening platform. Their request-for-proposal is designed to find the best platform, not the best platform for the bank. That is a huge difference as the best parts in the world do not make the best car, but the best system of parts make the best car for your needs. That reframe is critical.

If you had a Toyota Camry and wanted the best engine, you would drop a Koenigsegg Gemera engine from Sweden into the car to produce a smooth 2,300 hp. However, without an upgrade in brakes, chassis, powertrain, transmission, electrical, and so on, it wouldn’t work in the best case and the worst case hasten your demise. The same is true in banking.

A system is a group of interacting elements that act according to a set of rules or constraints to form a unified whole.

Understanding a system, like a fire, allows you to apply the least amount of resources to have the most success. It doesn’t matter if you are trying to raise deposits, open an account, navigate your career, stop fraud, or set a strategic course for the bank, system thinking is the key to moving from that middle management role to that executive management role and moving the bank to greater performance.

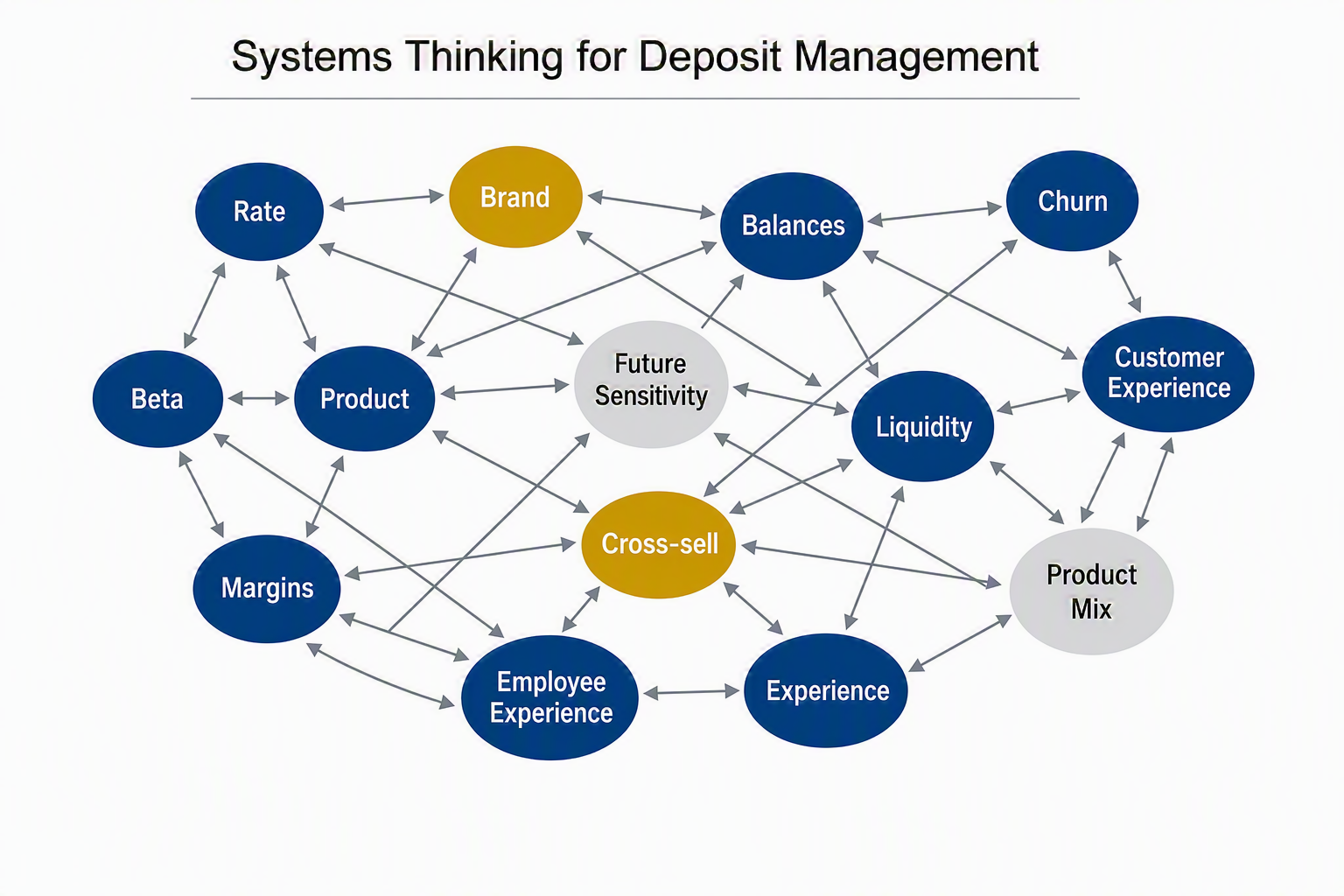

Take deposit raising as an example. A community bank sees funding pressure. A competitor raises rates. A digital bank posts an aggressive money market offer. A large depositor asks for more yield. The instinctive response is to match, promote, or defend. Raising customer rates solves the immediate problem but has both downstream and upstream effects that causes other problems.

Deposit pricing is rarely a simple math problem. It is a system. A rate change affects new balances, existing customer expectations, frontline behavior, margin, liquidity, betas, product mix, promotional churn, relationship profitability, brand, and future pricing power. The visible effect shows up quickly. The real effect often arrives later.

That is why community bank executives need more than pricing models or vendor selection. They need system thinking.

Understanding Your System And Applying System Thinking

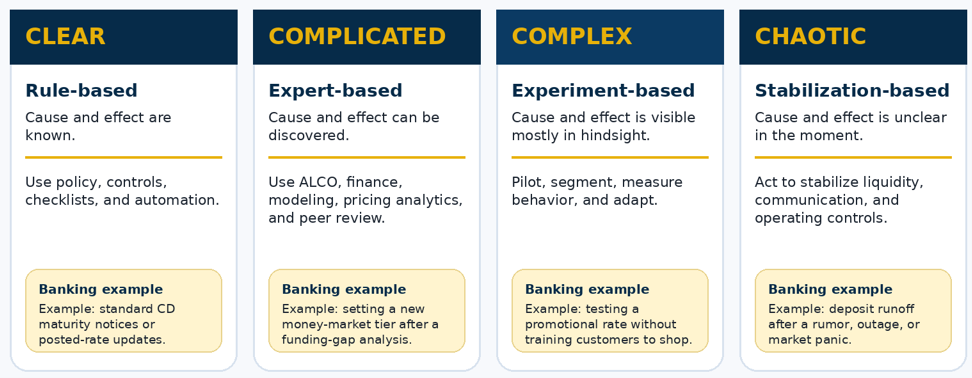

The Cynefin framework, developed by Dave Snowden in 1999, is a conceptual model which helps bankers understand their challenges and to make decisions in context. The framework describes four system types – Clear, or simple systems, Complicated, Complex or Chaotic systems. The framework then describes different approaches to take for each of these domains, depending on the relationship between cause and effect. Knowing what system, you are dealing with is the first step to optimizing a solution.

Clear Systems

In a clear, or simple system, the system is known and the cause and effect of changing anyone component is directly observable. Predicting outcomes in a clear system is highly accurate. Following a recipe while cooking is an example of a clear system. Handling CD pricing, or merit increases are examples of clear systems in banking.

To thrive in a clear system, being consistent, having policy, controls, checklists, and automation help control risk and enable scale. When applying generative or agentic AI, always start with a clear system so that any deficiencies can be easily corrected and the system can be easily integrated for success.

Complicated Systems

A complicated system may have less nodes or actions than a clear system, but what makes it a complicated system is that the relationship between the cause and the effect isn’t easily known. Your body is often considered a complicated system. Stomach pain could be something you ate that will go away in minutes or it could be an internal bleed that could result in a terminal condition in minutes. In banking, setting deposit tiers, suggesting a mortgage product, conducting M&A due diligence, or introducing a new revolving line of credit product are examples of complicated systems.

To thrive in a complicated system, bankers must apply analysis or seasoned expertise that have knowledge of the system to excel. Bankers suggesting an ARC loan hedge product or a FX solution are examples of experts helping clients solve complicated systems. Bankers should look for Complicated Systems in which to help their clients.

Conducting Monte Carlo simulations, stress tests, or hiring a consultant are all good reactions by bankers to better understand complicated system optimization. You don’t need a consultant for a Clear system and applying a consultant to a Chaotic system is likely worthless, but the value of getting the experienced consultant is immense for a Complicated system.

Complex Systems

Complex systems is a complicated system where some inputs have a disproportional impact on the outcome that is not always predictable. That is, system nodes often have non-linear, or geometric relationships with other nodes. Often, a hallmark of Complex systems, is that accurate predictions are complicated and only observable with hindsight. World Cup outcomes like we vibe modeled HERE to explain Complex system modeling using agentic AI is a real-world example. In banking, deposit management, M&A integration or cultural development are example of Complex systems.

To thrive in a complex system, AI modeling and consultants can help, but they are less effective than they are in a complicated system. They also tend to be more expensive because the bank needs support over a longer period. Time is part of what makes complex systems difficult: what worked in one interest rate environment may not work in another. To succeed in Complex systems, bankers must run ongoing experiments to learn how relationships change in real time and over time. Then bankers need to dynamically adjust strategy and tactics to stay ahead of a Complex system.

As discussed in our World Cup vibe modeling piece, success in predicting the outcome of Complex systems rests on banks moving from a deterministic view to a probabilistic view. Being able to model outcomes and their probability of occurrence allows banks to set a variety of strategies.

It’s also worth noting that banks need to redefine success in a Complex system. Success in a Complex system means you should strive to be directionally correct instead of precisely right.

Chaotic Systems

A Chaotic system is a complex system where the cause and effect between the input variables and outputs is not only not known, but likely impossible to know. While certain variables are more sensitive to inputs than others in a Complex system, in a Chaotic system, the entire system is more sensitive to its starting variables.

The good news is that despite their chaotic appearance, Chaotic systems are bounded and structured. When plotted in a mathematical space, they create distinct, repeating, and bounded shapes (often called “strange attractors”). The bad news is that banks just can’t know the bounds, limits, or rules of the system until it’s too late.

In life, weather, biological and social media are all examples of Chaotic systems. In banking, bank liquidity runs, cyberattacks, and market panic are palpable current examples.

A bank rarely can thrive in a Chaotic system, only survive. The proper strategy when dealing with a Chaotic system is to shut down all or parts of the system to limit the number of variables in play. This is why we recommend that every bank have internal limits on when they shut down liquidity outflows to prevent a catastrophic event.

In a Chaotic system when things go bad, it is a race for understanding that is pitted against liquidity, credit, reputation, or other critical variable. Buying yourself time and insight into what is happening should be management’s sole goal as an initial defensive plan.

On the other side of the coin, it is equally important to understand that action and controlled experimentation is the key to survival. Bankers must train themselves to act on imperfect information and not suffer from analysis paralysis. Like in a fire or an earthquake, creating safety, anyway possible, should be the first order of business.

During the Great Liquidity Crisis of March of 2023, the banks that failed placed too much emphasis on their perception of regulation and customer experience and not enough on survival. Any time a bank finds a critical variable (liquidity, credit, etc.) passing a three standard deviation event, which is an indication that they are likely now in a Chaotic system, and it is time to start limiting your variables. Once you reach a five standard deviation event, you likely need to be at a full stop to survive.

Unfortunately, about 500 people a year die of acetaminophen (Tylenol) overdoes. These mostly happen over time. However, when seven people died within 48 hours after taking average dosages of Tylenol back in September of 1982, Johnson & Johnson knew they had a five standard deviation Chaotic event. They survived because they shut everything down and immediately recalled all 31 million outstanding bottles. There was no analysis, no waiting for the FDA to approve, no counter marketing, only action.

Chaos has no interest in analysis, data trends, regulations, or the customer experience.

Up Next: Applying System Thinking to Banking Problems

System thinking gives leadership teams a practical framework for knowing when to standardize, when to bring in expertise, when to experiment, and when to act decisively to protect the institution. In a market defined by liquidity pressure, AI adoption, margin compression, and accelerating customer expectations, banks that understand the system before choosing the solution will allocate resources more effectively, reduce execution risk, and create a more durable competitive advantage.

Next week, we will provide a diagnostic tool to help bankers determine what system they might find themselves in and a more detailed plan on how to react. We will also look at applying system thinking to deposit management and how setting up feedback loops is the key to controlling system performance.