Vibe Modeling in Banking: Lessons From Predicting The World Cup

Its World Cup mania and creating a model to predict the winner is excellent training for bankers looking to forecast their deposit run off in the future. In this article, we take bankers through a step-by-step process of “vibe modeling” a World Cup model and then apply it to modeling future deposit run off due to higher rates, money market fund competition, stablecoin and tokenized deposits. We will discuss the former model and provide output, and then in a future article, we will provide bankers with the deposit run off model.

A banker may not care who wins the World Cup. But every banker should care about what the vibe modeling exercise represents as AI is now a powerful tool that every business line owner needs to have. No matter if you are using Copilot, ChatGPT, Claude or another frontier large language model (LLM), we will show you a path to increase your predictive accuracy when it comes to bank decisions.

The Old Way vs. The New Way vs. the Proper New Way

To model the World Cup outcome or deposit behavior, the old way would have you spending weeks writing Python code to employ machine learning techniques to prosecute the data and gain insights. This took compute and an analyst with machine learning training.

The new way is to ask Claude or ChatGPT, “Predict the Winner of the World Cup” and get back “Spain.” However, if you went to the betting/prediction markets like DraftKings, Polymarket or Kalshi, France currently has the best odds (as of 6/13). You would be confused and you would only gain a single insight that would be of limited value if you were trying to set a bank strategy or a tactical plan around that one data point.

The proper way is to develop a standard methodology for testing models within the bank. In this age of vibe modeling, you can now describe the analytical objective in plain English, apply assumptions, feed the model data and back-test prior. Then you can use the model to simulate probabilistic outcomes. In stead of getting a single, overconfident answer from AI, you can now understand the problem better which you can then use to increase the accuracy of future models.

This is an important new skill for banking. The future is not only better large language models, agents, or better code, but a better understanding of some of banking’s most important problems.

The World Cup model is a useful analogy because it starts with a familiar problem: predict an uncertain outcome using historical data, current conditions, and judgment-based adjustments. That is exactly what bankers do when they ask questions like:

- What will be my balance growth if we raise our money market rate by 25 basis points?

- How will customers react if the bank introduces tokenized deposits?

- Which customers are most likely to leave if a competitor offers 3.75%?

- How much margin do we give up if we need to retain all of our deposits in the face of stablecoin competition?

You can discuss all the questions above around a table at your next executive management meeting but unless you have some quantitative way to make a decision, you are just guessing.

Having an opinion is good, but having the data to back up the opinion is better. Best yet, is understanding both the question and solution through probabilities.

The World Cup Vibe Model, Translated for Bankers

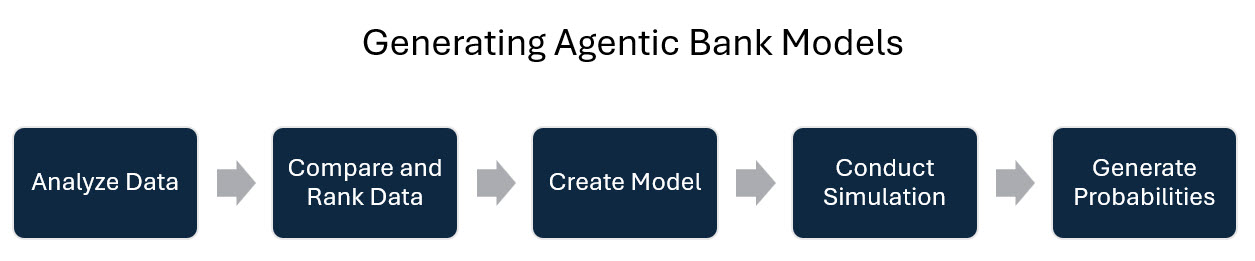

To build a World Cup, or deposit model, you can use five basic steps.

Gather the Data: First, gather a historic data set. In the World Cup example, we used all international soccer matches. In banking, which might mean five years of account-level deposit balances, rate history, gender, age, product ownership, transaction activity, branch geography, customer tenure, digital engagement, officer calling activity, and competitor pricing.

Side note – We were just recently asked by another banker what is the most important first party data set that you need to accurately model deposit behavior and the above is our answer.

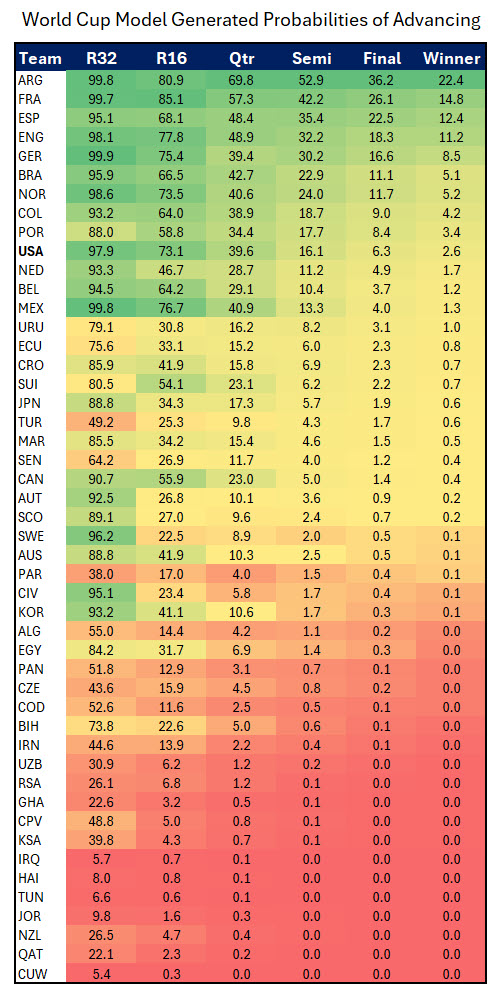

For the World Cup model, we had Claude pull every men’s international game since 1872. That’s about 49,000 matches, including all the friendlies and qualifiers. We weighted recent games more.

Develop a Score: Second, we create a strength rating. This is common when it comes to sports forecasting (think NCAA basketball), chess matches (think Ello rating), or deposit rate sensitivity (see our sensitivity model HERE). For soccer, we estimate team quality. For banking, the equivalent is a customer or household strength score. That score could reflect balance depth, relationship tenure, rate sensitivity, product breadth, direct deposit behavior, operating account status, debit activity, treasury services usage, loan relationships, and profitability.

Build a Simulation: Third, simulate what you want to model. Use the score as the basis for a simulation and run the simulation some large amounts so that outliers get normalized. In our case, we ran the model 50,000 times. For our deposit model, we ran it 10,000 times.

Develop a Model Based on the Score: Forth, turn the ratings or score into probabilities. A stronger team has a higher probability of winning, but not a guarantee. A high-value commercial operating account has a higher probability of staying but still may leave if the spread between your rate and the market becomes too large. A rate-sensitive household may move balances even if they have been with the bank for 20 years.

This is the most important part. The output of our model did not say, “Argentina will win.” It said Argentina may have the highest probability of winning, but many outcomes remain possible. This is a critical nuance to help a bank’s management team understand the other possibilities.

For bankers, this means the right question is not, “How much deposit growth will we get?” The better question is, “Across 10,000 possible outcomes, what is the distribution of deposit growth, margin impact, cannibalization, runoff, and lifetime value?”

Back Test: Fifth, test your model on hold out data. A model is just a random number generator if you don’t back test. Take a portion of your data set and “hold it out,” or don’t use it to develop your score and probabilities. This is called “out of bands testing,” and is the way to validate a model. For the World Cup model, we tested it against other tournaments to see how the model did against the actual outcome.

What we found was another important lesson, models don’t predict the future, but they can inform the future. Any sports tournament is hard to predict, particularly the World Cup with its limited data (sound familiar). In testing, our model achieved about 54% accuracy which isn’t bad for a weekend morning’s worth of work.

This is how the largest banks think about deposit modeling and now with the advent of generative and agentic AI, it is now easier than ever for a $200mm bank to have a sophisticated deposit model for about $1,000 of tokens.

The Role of Judgment: Home Field Advantage

Another aspect of modeling and AI is that it does not replace an experienced banker. In our soccer example, a strict statistical model overlooks the grandeur that is the World Cup. It also overlooks the importance of playing the World Cup in North America.

In our World Cup model, we included a host-nation bonus for the United States, Canada, and Mexico. We applied a 10% relative lift to the win probability of the three host countries because home field advantage is likely understated in a purely historical model. Travel, crowd support, climate familiarity, time zone, venue familiarity, and emotional momentum matter. In the adjusted view, the United States is close to Germany in the ranking and significantly above where a straight statistical model would have them based on all historical games. That does not mean the USA is more talented than traditional powers. It means the model reflect a contextual advantage that raw history may not fully capture.

The below table are the relative rankings from the vibe coding exercise showing Argentina winning followed by France, Spain and England. Whether any of the below happens, we are not sure. What we are sure of is that are process for using data is sound and that the exercise gives us a better feel for what we know, and more importantly, the fallibility of the outcome. Most importantly, we know that now that we have a methodology, the model will get more accurate with each use which is not the same if you don’t use a model.

In similar fashion, good bank modeling applies the same principals.

We discussed this when we showed our deposit sensitivity scoring. We compensated for the historical data set by capturing a banker score of how loyal the customer is to the bank. Our non-adjusted deposit model reflected a 30% probability of moving funds if the bank remains 125 basis points below market. However, if a banker knows the relationship is strong, we provided a place, and a weighting, to capture the data and adjust the data.

This also can happen in reverse. A model may see a 20-year relationship and assume stability. However, a banker may know that the customer is shopping the relationship because the next generation of ownership has taken over. That context also matters.

While it is possible our banker, or geographical adjustment may “overfit” the model, the lesson here is that you will never know unless you try, test and iterate. Having skills in vibe coding, and having access to your own model where you can improve the process each iteration is a huge step forward for accuracy.

Deposit Modeling Is a Tournament

Deposit modeling is similar to tournament modeling. Think about each customer as a team in a bracket.

Some customers are favorites to stay. They have operating balances, multiple products, strong engagement, and low demonstrated rate sensitivity. Others are underdogs. They have single-product money market accounts, large balances, low transaction activity, and a history of chasing promotional rates.

When the bank changes a rate, every customer “plays a match” against several forces to include:

- Your offered rate.

- The customer’s current rate.

- The competitor’s rate.

- The customer’s switching friction.

- The customer’s relationship depth.

- The customer’s liquidity need.

- The customer’s trust in the bank and its brand.

- The customer’s awareness of alternatives.

The problem is that no single factor determines the outcome. A 75-basis-point exception rate increase may retain one customer, fail to retain another, and unnecessarily overpay a third who would have stayed anyway.

That is why deterministic models are dangerous. A spreadsheet that assumes “raise rate by 50 basis points and retain 80% of balances” hides the most important question: which 80%?

A better AI-assisted model would segment customers into probability bands and simulate behavior across multiple scenarios. For example:

Base case: no rate change.

Defensive case: increase rate by 25 basis points for selected customers.

Aggressive case: increase rate by 75 basis points for customers above a rate-sensitivity threshold.

Relationship case: offer a blended package, such as a moderate rate increase plus treasury fee concession, cash management review, or loan pricing benefit.

The output should not just be deposit balance growth. It should be risk-adjusted return on capital (RAROC) to include net interest margin impact, cannibalization, customer lifetime value, fee income, expected churn, and relationship profitability.

The Biggest Mistake: Asking AI for an Answer Instead of a Model

If you ask Claud, “Tell me what deposit rate to offer.” That is the banking equivalent of asking, “Who will win the World Cup?” That question is reductive to the point of being dangerous.

The better prompt is:

“Build a customer-level deposit retention model using historical balance behavior, rate changes, tenure, product ownership, gender, geography, customer age, officer coverage, digital engagement, and competitor rates. Estimate the probability of runoff under different pricing scenarios. Separate existing balance cannibalization from new money. Run 10,000 simulations and show expected balance retained, incremental interest expense, net margin impact, and confidence intervals by segment.”

AI makes that kind of modeling more accessible. A banker no longer needs to wait weeks for a traditional analytics queue to answer every question. The banker can start with a natural-language request, inspect the assumptions, challenge the data, adjust the model, and run scenarios.

In no way is the banker abdicating judgment.

The World Cup model is only as good as its assumptions. How much should recent matches matter? How much should home field matter? Should injuries matter? Should travel distance matter? Should knockout-stage experience matter?

Deposit models have the same issues. How much should recent balance behavior matter? How should we treat pandemic-era deposits? How should we weight branch proximity? How should we handle customers with multiple entities? How should we adjust for competitor intensity by market?

The power is not that AI gives bankers perfect answers. The power is that AI gives bankers a faster way to test imperfect assumptions.

Most importantly, a model provides the foundation to build future, more accurate models. Testing banker judgement now matters more than in the past as AI can now quantify that judgement and make it actionable.

From Vibe Coding to Vibe Modeling

“Vibe coding” is the idea that users can build software by describing what they want in plain English and letting AI generate the code. For bankers, the bigger opportunity is “vibe modeling.”

A banker can describe the business question: “We are considering a 50-basis-point rate increase for high-balance money market customers in three competitive markets. Estimate balance retention, cannibalization, margin compression, and customer-level profitability over 36 months.

Then AI can help build the model, identify missing fields, test assumptions, generate visuals, and explain the results in plain English.

The banker’s job becomes higher value. Instead of building formulas cell by cell, the banker asks better questions:

- Does this model separate new money from retained money?

- Does it overstate rate sensitivity for operating accounts?

- Does it understate digital-only attrition?

- Does it reflect local market competition?

- Does it include relationship profitability?

- Does it show downside risk, or only the expected case?

That is where bankers create advantage both for the bank, and for their careers. Bankers that don’t learn these skills will become less valuable in the future.

Some Final Insights on Vibe Modeling

This exercise was helpful to uncover some meta-truths that we want to highlight even if you are not going to learn how to vibe model.

Banks Can Save Cost: Vibe coding unlocks an internal super power for all bankers in areas of credit, finance, ALCO, marketing and sales. Before the advent of agentic AI, bankers would have to “big thumb” it, or turn to a vendor that may or may not help. Now, bankers have the tools to develop a world class model themselves with the help of AI.

Messy Data Is Now Useful: The hardest part of any bank project is getting clean data. AI can now help clean and use desperate data easier than ever before. You can now feed it various spreadsheets, pdfs, CRM links, and Word files that you previously would have needed a data team to handle. Here, a frontier LLM, like Copilot, can digest 49,000 matches in about 20 minutes.

Your Experience Is Now Exponentially Important: Any new banker can ask ChatGPT a prompt. Before we model anything, we made sure the model digested the data set and then asked the model to ask us questions to improve the output. We then had to decide how much to weight the games over time, geography, and importance. How much should a friendly match weigh? Once we were satisfied with how AI was handling the data, only then did we move forward to scoring.

When you go to banking conference or listen to pundits, they often make it seem like it’s the initial prompt that is critical. While prompting is important, the new job of bankers is the back and forth to prosecute the model and get it to where you can trust it. Part of the value of AI is how it forces you to think about banking problems.

The Modeling Process is the End Not the Means: We authored this article to underscore the need for bankers to not only learn how to vibe model, but how to develop a repeatable process. While any model is likely important, the ability to educate and train the whole bank on the proper way to create, develop and test the model is what is the most valuable.

Data Still Maters: While messy data is now useful, you still need the data. Our World Cup modeling was sped up because we found a clean data set on Kaggle.

Side Note – Kaggle has lots of clean data sets applicable to bank modeling.

For many bank modeling efforts, data collection will not be as easy. You may have to develop agents to retrieve data from various FDIC websites, your core systems, or various spreadsheets before you pull the data into a single place and clean it up. We understand that we are making this sound easier than it is. Bank data wrangling remains a challenge.

Use the Model to Model: Most bankers are evolving in their AI usage to have the LLM itself help teach AI. You don’t have to be an expert modeler any more than you have to be an expert coder. Ask your model to test its own output and where it thinks your assumptions are weak. Use your experience to then judge AI’s judgement. A good answer that knows its limits beats an overconfident “great” answer.

Putting Vibe Modeling Into Action

The World Cup example is fun because everyone understands the uncertainty. Argentina, Spain and France may be the favorites but Germany and England could easily end up winning for reasons that the model can’t capture.

But the deeper lesson is not about soccer.

The lesson is that AI allows bankers to move from static reporting to dynamic forecasting. Instead of looking backward at deposit runoff after it happens, banks can simulate customer behavior before they change rates. Instead of treating all deposits the same, banks can model each relationship as its own probability curve. Instead of debating one forecast, banks can compare thousands of possible outcomes.

This is the future of banking analytics. It’s not about one answer, but the ability to now easily model the real world. Creating a set of assumptions, a probability distribution, a model, combined with a banker smart enough to challenge the output can now do things only the largest of banks could do before.

We are working on such a deposit model to be released shortly which takes off from our Deposit Vulnerability Index that we highlighted HERE.

To learn more about using AI for deposit modeling, come to our Deposit Conference in October (Chicago) as we are getting close to capacity (Register Here)

To learn more about AI for marketing modeling, come to the ABA Bank Marketing Conference (Learn More HERE).