How to Increase Debit Card Profitability

While there are many overlooked products in banking, the debit card is perhaps the greatest. The product generates significant fees and helps drive deposit balances, yet debit cards rarely get a mention in strategy, marketing, or customer profitability circles. The debit card is one of the greatest workhorses of banking and, unfortunately, is forgotten about due to its sexier older brother—the credit card. In this article, we look at profitability and some simple ways that banks can boost customer profitability by using the debit card.

While banks are aware of the interchange fees debit cards generate, many bankers don’t understand the importance of the card in building balances and retaining customers. Few bank products are as wide-ranging as the debit card, so minor improvements in usage can have an outsized impact on bank profitability.

If you are not writing checks (and fewer customers are these days) and your bank does not have its credit card program in-house, then it is likely that your debit card is the only physical manifestation of your bank outside of the mobile app. Because of this, by promoting your card, your bank is promoting its brand and creating a more important customer.

Debit Card Profitability

We will start with debit card profitability. Depending on the size of the bank, the type of transaction, and the network, banks make an average of $0.34 per use. Banks over $10B in asset size make closer to $0.23 per transaction, and banks under $10B are about $0.52 per transaction. The more the customer uses their debit card, the more interest rate balances they will likely keep in their transaction account. Compare an active card account with an inactive one, and you will likely find that balances are about $510 higher in active accounts. Balances, we will quickly add, cost about 1.12% compared to having to pay a typical cost of funds that is currently north of 2.61%.

To support debit card operations, a bank gets charged a myriad of transaction charges and maintenance fees from the card rails (Visa, Mastercard, Discover, etc.), the network (Interlink, Pulse, Shazam, etc.) and the bank’s processor (usually their core). On top of that, a bank’s branch and card support network spends a lot of time handling card accounts, from opening to replacing cards to solving problems. Materials, training, and fraud also contribute to bank expenses.

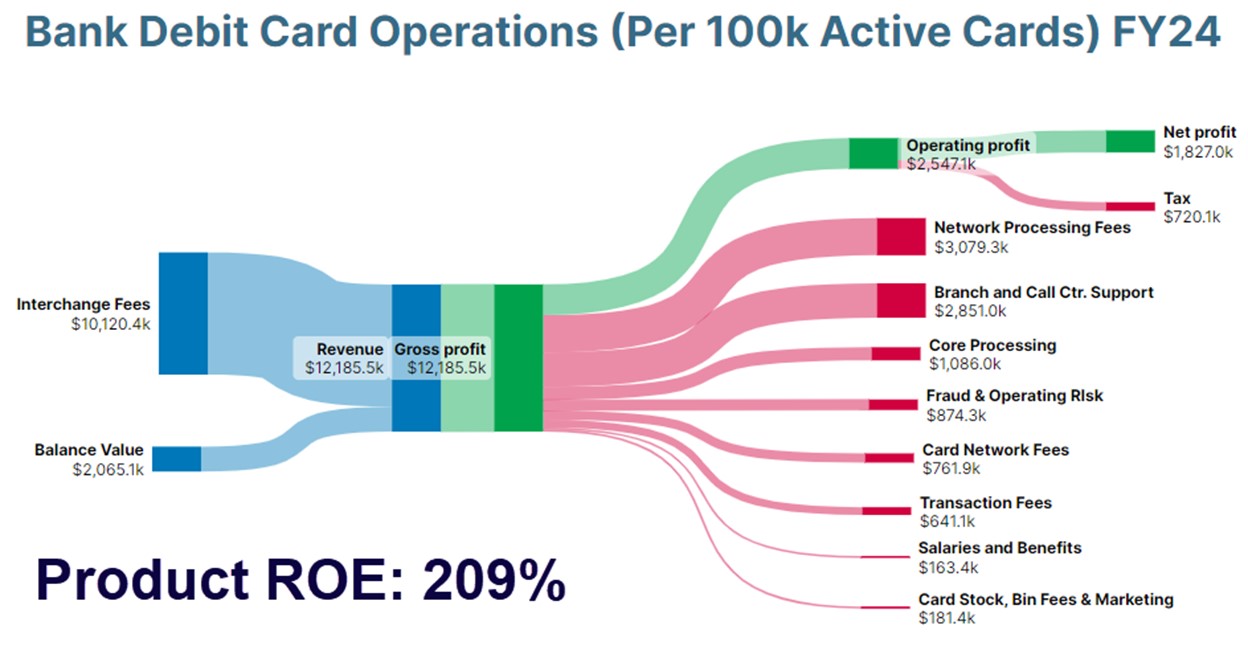

On a net basis, a bank under $10B likely has a risk-adjusted annual product profitability profile of something close to the below graphic per active 100,000 cards. We assumed a typical mix of 89% consumer and 11% commercial debit.

For banks above $10B, revenue is about half, dramatically impacting the ROE, causing current debit card programs to be breakeven propositions often unless a bank has enough scale.

Aside from product profitability, an active card user will likely be less interest rate sensitive and have more products with the bank. This combination of attributes means that customer defections are lower, and the average customer life is about 2.1 years longer compared to a non-active debit card customer. At 20 average monthly transactions and additional balances, an active debit card user produces about $94 per year of extra revenue. Combined with an additional two years of life, the average consumer lifetime value moves from about $3,283 to closer to $4,132, or a 26% increase in customer lifetime value.

6 Tactics to Increase Profitability on Debit Cards

Banks need to focus on promoting debit cards to increase fees, balances, and customer retention. We don’t advocate a major effort here, but there is some low-hanging fruit that any bank can execute to improve profitability on the margin.

- Get A Product Manager, Set a Strategy & Measure Performance

The lack of attention on debit cards almost stems solely from the fact that few banks have a debit card product manager, a distinctive strategy, a tactical plan, or a set of key performance indicators that track progress.

Given the above profitability, it pays for a bank over $1B to have at least one person focused on driving debit card value. This is an excellent early management position for an up-and-coming banker. Responsibilities include setting and executing a strategy to drive activation and engagement, plus managing daily operations. In addition, the debit card manager would work with retail, small business, marketing, and the branch network to bridge across silos.

The debit card product manager would also produce a set of KPIs to track and improve performance.

- Onboarding, Activation, and Top of Wallet – Education

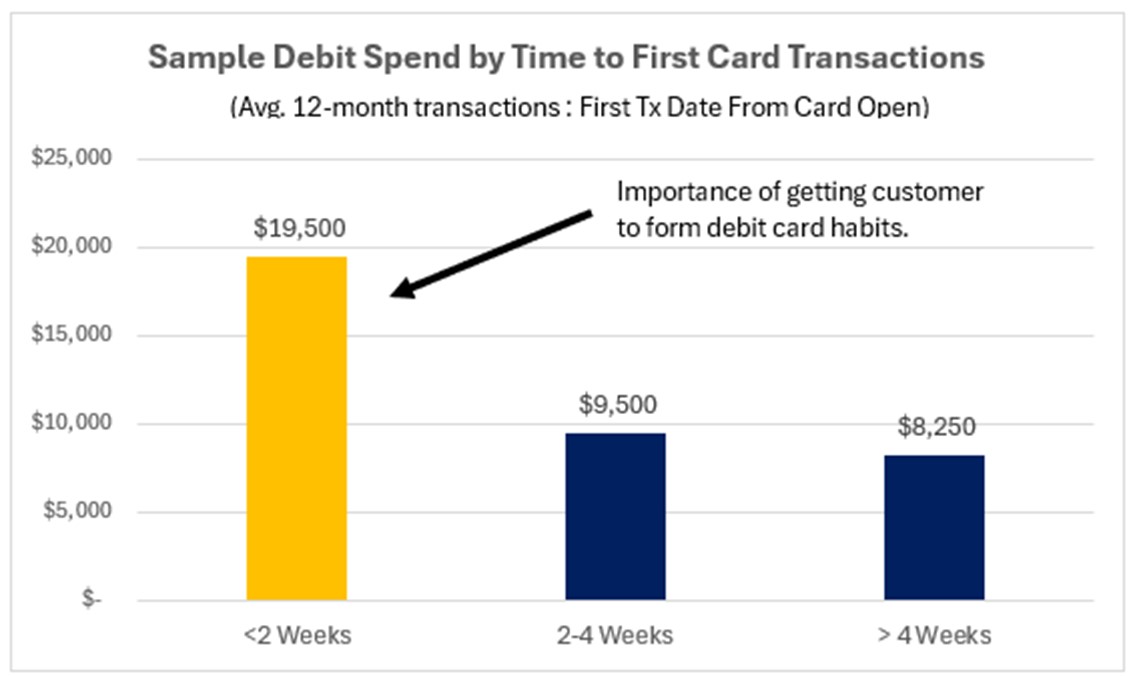

When it comes to low-hanging fruit, nothing is lower than the average 35% of bank customers that receive a card but don’t activate it. Customer spend and bank profitability are primarily determined by a bank convincing the customer to move their card to the top of their wallet and/or routinely using their card in the first two weeks. A customer who uses their debit card in the first two weeks usually produces more than twice the dollar volume and number of transactions than a customer who waits a month to activate their card.

This is particularly true for the 58-77-year-old cohort. Here, spend and the number of transactions per month can be more than 2.4x greater than for a customer who waits a month to use the card for the first time. If a bank can convert 3% of their new card customers to having a first transaction within two weeks of issuance, it would result in an additional 643k transactions or another $341k in revenue.

Banks should target existing customers with activation marketing campaigns while getting branch personnel and drip marketing campaigns (email and in-app notifications) to better onboard customers to a debit card. Most banks merely hand an instant issue debit card to the customer at account opening or let them know one will be mailed shortly. It is extremely rare for a banker to explain the pros and cons of using debit cards vs. a credit card.

Educate your bankers on the power and importance of your debit card and chances are they will pass this knowledge on to your bank’s customers. The best sales technique to do this – just ask. If a banker doesn’t ask the customer to use their card, many customers will keep with their normal habits of using another bank’s debit or credit card.

For customers who are averse to using credit or trying to live without credit, debit cards are preferred over credit cards. For customers that don’t care about loyalty points, a debit card is more efficient as you don’t have to make a second payment to a credit card bank and don’t risk missing the payment and being responsible for interest.

- Engagement Marketing

If the debit card is active, then banks should create marketing campaigns to promote the use of their cards in daily transactions. These can come in the form of email, in-app notifications, digital ads, organic content, social media, and digital retargeting campaigns. The highest marketing return on investment (ROI) occurs when banks remind customers to use their debit card for groceries, retail services, restaurants, and telecom/utility bills in that order.

In addition to marketing the physical presentment of a debit card, banks can tell if a customer’s card is being used for digital purchases. Targeting customers who don’t have e-commerce transactions on their debit card is also a double to triple-digit ROI when it comes to debit card marketing.

Marketing campaigns should target customers in the 26 to 57 age range since these cohorts make up more than 70% of a bank’s debit card transactions by dollars spent. Targeting dormancy is also a popular card marketing tactic.

- Increase Fraud Tools

The largest impediment for customers using their card more often is the narrative espoused by many financial sites and advisors that the debit card is less safe than the credit card. While credit cards often provide better consumer protection, the probability of debit card fraud is much lower (only 17% of card fraud is debit card related), and the expected loss is lower as well. The loss liability for the consumer is the same ($50) on both debit and credit if debit card fraud is reported within two days. It is true that debit card fraud immediately impacts the customer’s account whereas customers can see a provisional reversal of the fraudulent transaction. These are important educational points, and having consumers monitor debit transactions in your banking app will help limit fraudulent activity plus drive engagement.

More importantly, the reason why credit is preferred to debit is that credit card companies have more advanced fraud tools because of their liability. Banks that put additional debit card fraud tools in place, the same tools banks need for instant payments, can dramatically reduce debit fraud. These tools include real-time transaction monitoring, machine learning algorithms, data analytics, multi-factor authentication, biometric authentication, location tracking, device fingerprinting, customer behavior analysis, fraud risk scoring, and an enhanced “Know Your Customer” (KYC) verification process. Doing any of these things can dramatically reduce debit card fraud activity.

On average, banks lose almost $900,000 per year per 100,000 active cards, mostly through “card not present” e-commerce-type transactions. Investing in fraud tools not only reduces this expense but also helps drive more engagement, as both customers and employees will have more confidence in debit cards.

- Manage Active Declines

Debit card transactions that are declined ends up hurting the customer experience and costing the bank valuable time in managing. Not having sufficient funds is the largest reason for card declines (about 35% of all declines). Educating customers and getting them in the habit of checking their account balance online/mobile can bring these declines down dramatically.

In about 20% of the cases, debit cards are declined due to hitting limits. This is an educational issue as customers often forget (or were never told) what their limits are. On the other side of the equation is many banks don’t utilize dynamic limits and have their limits set too low. By better-managing limits, banks can make their operations more efficient while creating a better customer experience.

- ATM Benefits

For the average community bank, about 70% of debit card holders have used the ATM in the past 12 months. On average, about 20% of these ATM transactions occur at an ATM that is from a different financial institution (a “foreign transaction”). This highlights a need for banks to build the elimination of foreign ATM fees into their account line up to help drive transaction account opening Having this option not only helps drive customer satisfaction and debit card usage, but also helps open more transaction accounts.

Preparing for the Future of Interchange

The debit card is a banking workhorse. It does much of the heavy lifting of promoting a bank’s brand while allowing everyday banking relevance. By working on some of the initiatives outlined above, a bank can generate between $257k and $1.3mm per 100,000 active cards.

The Federal Reserve currently is poised to release its final rule on interchange fees that is expected to further reduce interchange fees by around 28% to 14.4 cents per transaction. This would devastate the programs at many banks, particularly those between $10B and $25B in asset size. It is within this range where interchange fees are cut and there is likely not enough scale to make debit cards profitable.

When interchange fees do get cut, banks will need to enact many of the initiatives outlined above while renegotiating processing and network fees. Banks should also start thinking now about new products they should be introducing such as more “pay-by-bank” applications that can help reduce payment costs for the bank and merchants. For that matter, when fees do get cut, banks will have to start contemplating how to move off the debit card network rails to establish their own networks, possibly utilizing FedNow as a common payment rail.

No matter what the future holds, banks should consider starting to increase their investment in debit card engagement while it is still profitable.