How Banks Can Better Use Grid-Based Pricing

Grid-based pricing is typically used to set the applicable margin of a loan based on specific performance measures, such as credit rating or cash flow coverage. However, grid-based pricing can also be used to increase deposit balances. The average borrower does not calculate their cost of borrowing and return on deposits on the economic value as determined by fund transfer pricing (FTP). Community banks can maximize profit and increase loan balances using innovative grid-based pricing for their commercial clients.

Fund Transfer Pricing (FTP)

We have written about FTP in other articles, but in summary, FTP measures interest rate, credit, and liquidity risk and enables costs to be transferred from central treasury functions to the bank’s products and business lines. Fundamentally, FTP divides a bank’s overall net interest margin (NIM) into two significant sub-margins (one for deposits and one for asset origination). Banks can then measure the economic value obtained from each product separately. Grid-based loan pricing in relation to deposit balances can be an effective way for banks to capture cheaper and longer-duration deposits by providing lower margins on loans and increasing profitability on the total relationship.

Cost of Funding

Bankers have been focused on higher short-term interest rates and their effect on the cost of funding (COF), but few truly appreciate the greater source of risk to COF – liquidity risk from the Federal Reserve quantitative tightening. The Fed may have reached its terminal Fed Funds rate, but COF will continue to rise as the Fed continues to liquidate its balance sheet. The graph below shows the Fed’s balance sheet from 2002 to the present.

The Fed is reducing its balance sheet by $95B/mo, or $1.1T per year. The Fed’s balance sheet reduction directly and linearly affects the banking system’s liquidity. Every dollar reduction in the Fed’s balance sheet reduces the reserves that banks hold at the Fed. That, in turn, reduces deposits at banks by the same amount. Between June ’22 and June ’23, the Fed decreased its balance sheet by approximately $600B, and during that same period, the banking industry reported a $870B drop in deposits. Since the pandemic’s start, total noninterest-bearing deposits have increased by $2.3T, and we expect the Fed quantitative tightening to draw most of that excess liquidity out of the banking system by early 2025. Therefore, attracting long-term, stable, and lower COF deposits is paramount for community banks.

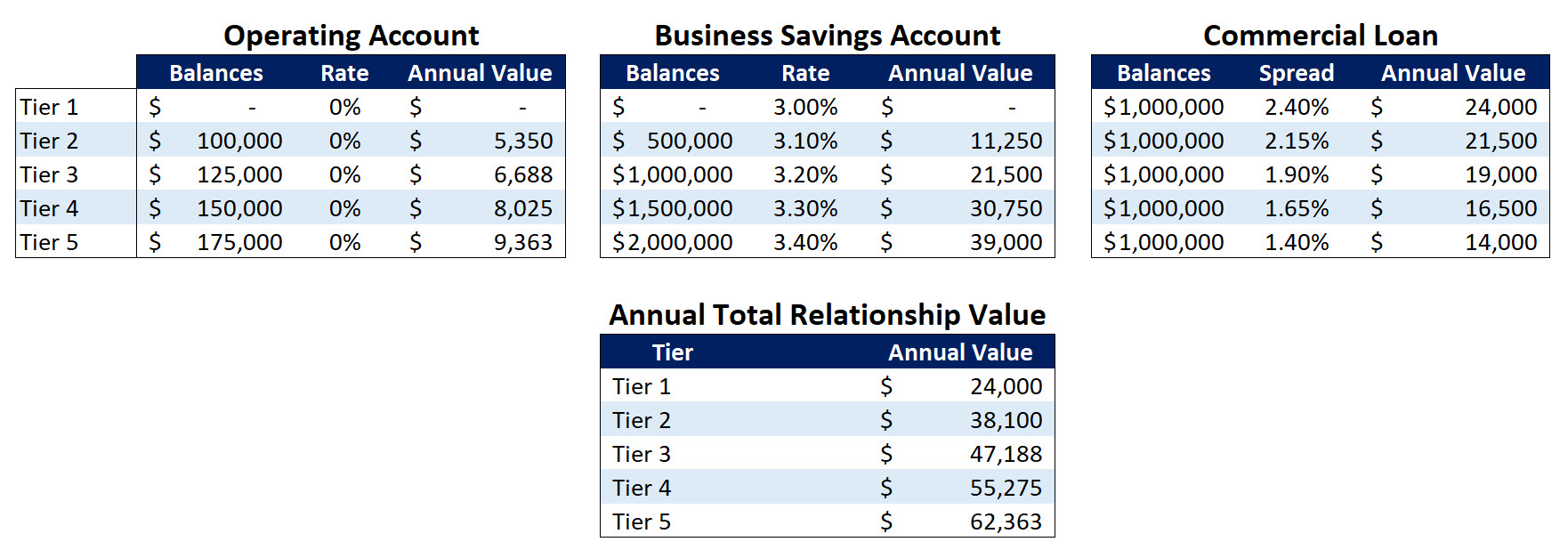

Grid-based Loan Pricing and Deposits

Grid-based loan pricing dependent on deposit balances is not a new concept and has been used by banks in previous periods of low or declining liquidity. The practice also should not breach the anti-tying restrictions of the Bank Holding Company Act Amendments of 1970 and related supervisory guidance. The scope of the anti-tying restrictions of the statute expressly permits a bank to condition the availability or price of a product or service to a customer on a requirement that the customer also obtain another traditional banking product, such as a loan, discount, deposits, or trust service, from the bank.

The benefit to a community bank is that FTP and decreasing liquidity in the market make each incremental basis point of margin from either a loan or deposit almost equally profitable. However, the margins on most deposit products are much wider than the margins on loan products (that is the stark reality when measuring ROE using FTP). Therefore, banks should be motivated to create grid-based pricing to give up some loan margins to capture deposit margins.

Further, one of the most significant issues with deposit profitability is the undefined contractual life of those deposits. The argument that deposits are for life, or some arbitrary number of years based on historical performance, has been shattered by rising deposit betas and declining balances due to the last tightening cycle.

In our grid-based loan pricing example, we will make some assumptions as follows: $1mm loan amount priced at 2.40% starting spread over SOFR (approximately industry average), operating account based on typical balances for the size of the relationship, business savings account with industry average yield tiered to balances. The annual value of the total relationship is shown in the bottom box.

The key takeaways from the above grid-based pricing and deposit relationship are as follows:

- The majority of the value to the bank is created in the combined operating and business savings accounts.

- Decreased loan spread is less valuable to the bank than the value created in the combined deposit accounts.

- The decrease in loan spread is only effective if the combined deposit account minimum average balances are maintained for the period (this can be monthly, quarterly, or annual, depending on the bank’s operational abilities). Grid-based pricing quantifies the economic value of the deposits instead of just a verbal undertaking by the borrower to maintain deposits.

- Most customers prioritize the value in the decreased spread on the loan vs. the value of the deposits. This allows banks to maximize income even as the loan spread is reduced.

Grid-based loan pricing dependent on deposit balances can be applied using any number of products, rates, and client needs. Our example is a simple $1mm commercial loan with two deposit accounts, but banks can use the concept to fit their specific needs. The appeal of grid-based pricing is that banks can now influence deposit balances and duration and take advantage of the FTP concept to increase the profitability of the total relationship.

How to Apply Grid-Based Pricing at Your Bank

The Fed balance sheet reduction will continue to pressure deposit balances and COF. The industry’s average deposit betas will continue to climb as the Fed slows or pauses interest rate hikes. Community banks with larger and more stable DDA, checking, and savings accounts will fare better. Grid-based loan pricing dependent on deposit balances can increase deposit balances and the duration or stability of those deposits, substantially enhancing bank performance.