LIHTC Opportunities for Community Banks

Less competitive markets can boost returns for community banks. Specialized lending refers to customized financing tailored to specific industries, asset classes, or complex business transactions. Unlike standard commercial loans that rely on simple financial ratios, specialized lending requires expertise to evaluate unique collateral and cash flow structures. There are some specialized lending opportunities that fit well within the community bank model and expertise. We work with half a dozen community banks that fund Low-Income Housing Tax Credit (LIHTC) projects, and these loans have minimal risk, acceptable credit spreads, high fee income, and above average ROE.

LIHTC Projects

All 50 states, Washington, D.C., Puerto Rico, and the U.S. Virgin Islands offer LIHTC projects. LIHTC is a federal program authorized under Section 42 of the Internal Revenue Code, and the federal government allocates tax credit authority to every state annually based on population. Each state administers these federal credits through its own designated housing finance agency. While every state participates in the federal program, there are major differences in how each state layers their own resources on top of it. To combat high development costs and fill remaining financing gaps, at least 32 states and Washington, D.C., have enacted their own state LIHTC programs that provide separate state-level tax credits on top of the federal ones.

Benefits of LIHTC Lending

LIHTC is a public-private partnership that may allow community banks to de-risk commercial real estate portfolios while directly lowering their federal tax liabilities. But there are other benefits as follows:

- Fulfill regulatory CRA expectations.

- Generate predictable financial and tax benefits. The senior financing offers highly predictable, risk-adjusted yields that outperform many CRE categories.

- Low default rates. The affordable housing sector historically features one of the lowest default and foreclosure rates in the real estate industry. By formula, rents are set below market causing more demand than supply. This creates a backlog of renters keeping vacancy rates near zero. In addition, borrowers want to protect the tax credits and will often be more likely to provide additional cash flow to the bank to prevent or cure any delinquencies.

- Expanding business and community footprint. Community banks can deepen relationships with local developers, establish relationships with municipal agencies and Community Development Financial institutions, invest in local infrastructure, and help gentrify local neighborhoods.

- Enhanced return for smaller loans (generally under $20mm). For smaller loans where the competition is less intense, we see banks pricing credit at SOFR plus 2.25% to 2.75% (pre-tax adjusted). Hedge fees are between 2.0% to 2.70% of the loan amount, and loan origination fees are 12.5 to 50 bps. These loans result in a RAROC of 20% to 30% depending on loan size, cost-of-funding, and efficiency ratios. Smart banks also ask, and usually get, the reserve accounts for replacement equipment as deposits thereby boosting RAROC by 200%+ for the deposit side, creating an average relationship RAROC closer to 30%.

Case Study

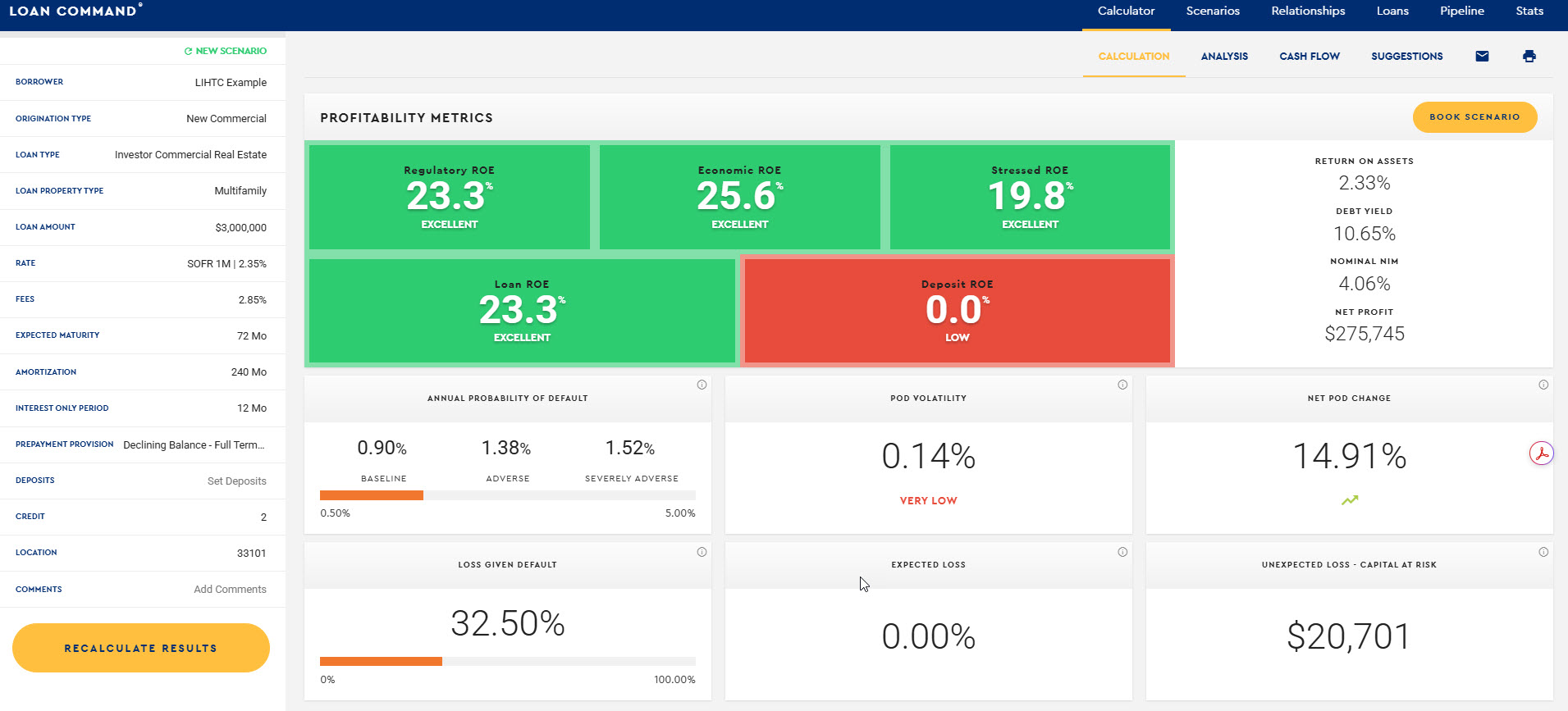

On a recent deal we helped our partner bank close a $3mm LIHTC loan on a $6.3mm project, 24-month construction followed by 15-year term loan. Pricing was SOFR plus 2.40% (pre-tax adjustment) with a 50bps loan origination fee and 2.6% hedge fee, for a RAROC of 24.5%. The required length of funded permanent debt is determined by equity investor mandates and federal compliance windows, which universally dictate a minimum loan term of 15 years. While the loan is typically amortized over a longer 30-to-40-year window. The bank used our ARC program to convert the fixed rate debt to the borrower to an adjustable rate on its balance sheet with a four-page Rate Conversion Agreement, no derivative for the bank, and single billing statement to the borrower. The permanent financing was locked at the inception of construction with a 24-month forward – a single close, construction through perm structure. The banks that we work with favor the ARC program for its simplicity, and when applied to LIHTC deals this program allows community banks to compete against national banks, but competition thins out for smaller deals (generally below $20mm in size, and certainly below $10mm). The ARC program also allows our lending partners to generate substantial hedge fee income.

Putting This Into Action

The ability to offer banking products and services that avoid competition is an effective way to enhance returns for a community bank. Senior funded LIHTC loans require a few minor adjustments to a standard community bank loan and result in a specialized lending product that generates above industry average RAROC. Community that can offer construction through perm, a hedge to accommodate at least 15-year terms, amortize over a longer period (30-40years), and ability to price on a tax-exempt basis can take advantage of superior returns on LIHTC financing.