Commercial Credit Trends – Where to Tread Carefully

Lending is getting riskier. Due to higher rates, inflation, and a slowing economy, the three essential credit metrics – probabilities of default (POD), POD rate of change, and POD volatility- have all materially increased from 2022. In this article, we look at what is happening at the state level, look at 30 common industries where credit risk is rising, and 30 industries where credit risk is the lowest. This data is critical for pricing, capital allocation, and marketing. Once again, it is time to play more defense.

When you write a blog, your work is there for all to see. In 2021, we published articles warning bankers against higher rates (for example, HERE) and the resulting impact on credit. We have seen the higher rates, and now bankers should brace for a credit shock.

For the first time since 2007, we are starting to see material signs of stress in the form of lower cash flows and less debt service coverage. The result is higher probabilities of default and greater credit volatility.

Credit Trend Summary

In general, the average probability of default increased by 65% over last year. The average probability of default at the end of 1Q was 2.86% in the U.S., 109 basis points (bps) higher than the same period last year. To put this in perspective, usually, credit changes an average of plus or minus 21 basis points each year against a long-term average POD for bank commercial credit of 2.19%.

Credit volatility also is seeing an increase. When liquidity and credit are plentiful, PODs tend to compress, and volatility is reduced. Now, the opposite is happening. As a result, almost every industry became more volatile. As an average, the two standard deviations are around 2.02%. This quarter, it is 2.58%.

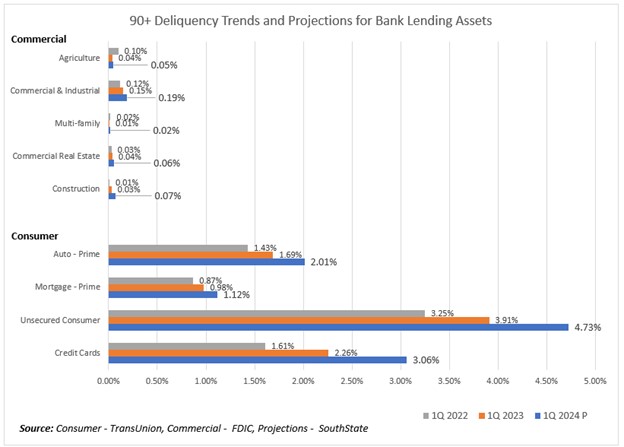

Below are the current delinquency trends and projections. As can be seen, the consumer is starting to feel the credit shock first while commercial lending is still performing. The operative question is when commercial PODs will show a spike. Our answer – within the next 18 months.

Commercial Credit Trends By State

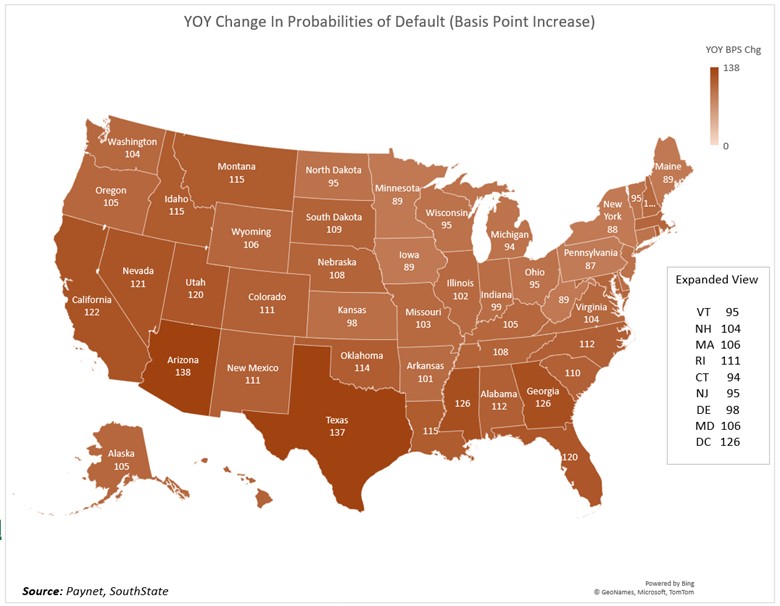

Every state increased its forward-looking probabilities of default on a material basis.

Below is a breakdown by state and their net probability of default increases, year-over-year. The Midwest continues to perform the best, followed by Pennsylvania. As can be seen, Arizona and Texas have the largest increases in credit risk, while Minnesota and Maine are the most stable.

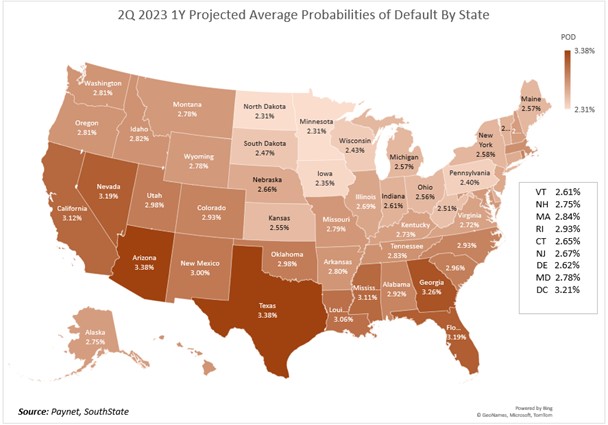

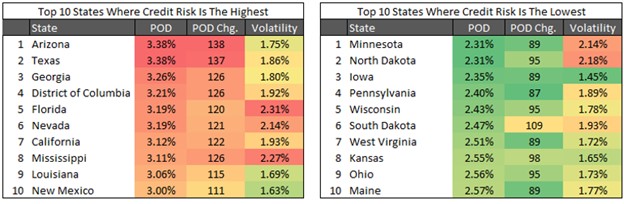

In terms of absolute probabilities of default, Arizona, Texas, and Georgia are the three riskiest states in terms of likelihood of default. Minnesota, North Dakota, and Iowa were the least risky states to lend into.

Regarding volatility, Alabama is projected to have the most significant variability in credit, while Connecticut is expected to have the most minor variability. AL ranks in the middle for overall risk, so they are not called out below, but because of the volatility, banks should monitor and exercise caution.

For more details, below are the top 10 worst and best credit risks by state.

Commercial Credit Trends By Industry

Most banks rate the bulk of their credits either a grade of “3” or a grade of “4.” The reality is that banks should be much more granular than that to allocate capital more efficiently. In good times or times when credit is improving, banks tend to overprice credit risk. However, in worsening times, like now, banks tend to underprice credit risk.

An increase in PODs means an increase in expected losses. Commercial expected losses, considering collateral, went from 62 bps to 114 bps and are likely to climb more. With the average loan loss and lease allowance (ALLL) at 1.60% for the industry, many banks will find themselves under-reserved.

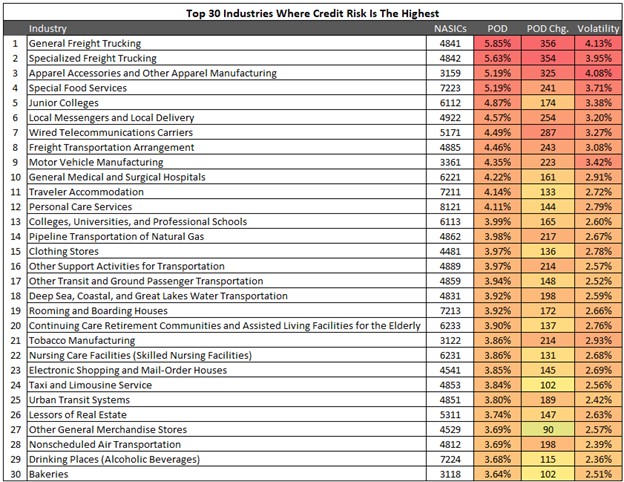

Freight, transportation, apparel, food services, and education dramatically increased in risk. Add to these five sectors the wired communication industry, and this group is exhibiting the most significant credit volatility and the largest increase in credit risk. The fact that freight is having issues is also a harbinger of larger issues. Lower freight revenue is often a leading indicator of future problems in manufacturing and retail.

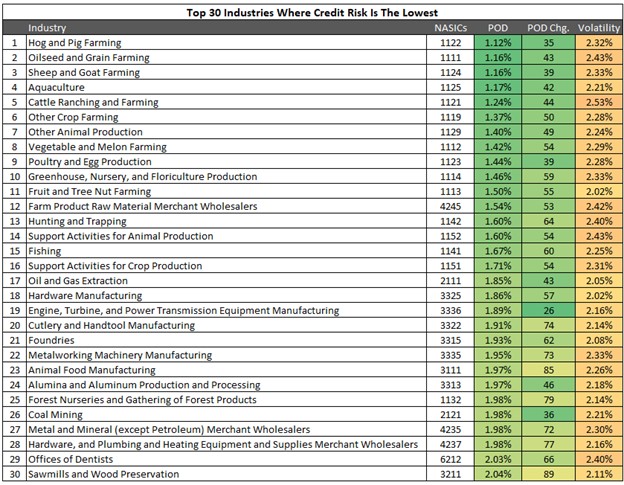

On the opposite side of the credit spectrum, farming and ranching had the lowest PODs, increased risk the least, and had the lowest credit volatility.

Credit Trend Ramifications & Loan Pricing

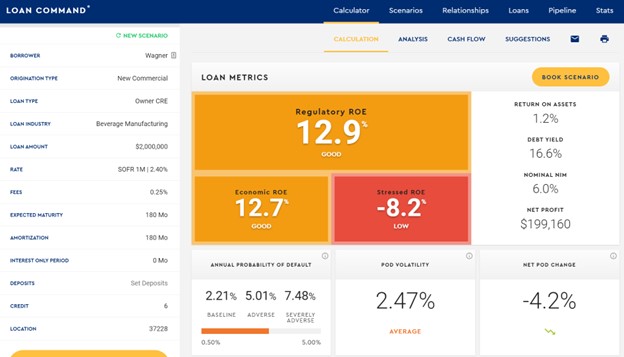

If you use Loan Command, our relationship profitability tool available to any financial institution for $89/month/person, you have all this data live to help you with your pricing and credit decision. Credit for hundreds of industries is included, as well as live rates. We have priced this cheaply so any bank, no matter its size, can afford this valuable tool. If you are not a subscriber, ensure your profitability model considers this significant credit increase.

One material ramification of this data is expected loan profitability dropped from a risk-adjusted return on equity of 14.6% last year to 12.7% this year as higher expected losses result in an increased credit charge. We modeled a sample average transaction below with the increased PODs and volatilities.

One counterintuitive point that merits contemplation and tactical decisioning is pricing. Typically, pricing needs to increase due to higher credit risk. However, as banks tighten lending (as evidenced by the latest Senior Loan Officer Opinion Survey), banks have stopped lending to many risky sectors. As a result, banks are going after higher-quality borrowers and existing customers where the credit risk is known and low. As a result, pricing has contracted in 2Q from an average spread of 2.48% at the start of the year to 2.33% in 2Q.

In terms of structure, as expected, loans with floating rates to borrowers and adjustable loans coming up for reset are now under the greatest credit pressure. In many of these cases, expected losses have tripled as borrowers get hit with the double whammy of increased interest and credit charges.

Fixed-rate loans from the 2020 and 2021 vintage are now performing the best in terms of credit, as many of these loans provide an extra incentive for borrowers to keep making payments. Inflation has likely helped cash flow in these cases while interest cost has remained fixed. Unfortunately, many of these loans have negative mark-to-market positions and are losing money for the bank because of the interest rate risk despite their low credit risk profile.

Of course, banks that extended fixed rates to the borrower and hedged with a floating rate have the best of all worlds. These loans perform at an 18%+ risk-adjusted return on equity as net interest margins have increased due to higher rates. At the same time, credit risk has dropped in many cases (office exposure being the notable exception).

Putting This Data Into Practice

In good times, this data can be ignored. If you are wrong in pricing credit or allocating capital, the impact is likely less than 50 bps of ROE performance. However, when the principal is at risk, being wrong can have terminal consequences.

When borrowers feel stressed, this data is invaluable for pricing, capital, and structuring decisions. The increase in PODs, loss-given defaults, and expected losses mean that banks need to choose their credit and pricing wisely. Getting more granular in credit risk means a more efficient allocation of capital.

Banks are more leveraged than the average hedge fund, and lending decisions have outsized consequences. Equally important, there is a time dimension to credit that is seen in only a few industries. While banks manufacture credit and relationships, it’s not like selling a widget.

You can correct your error the next day if you misprice a widget. When bankers make a credit decision, they live with that credit and that pricing for an average of six years.

While many banks are seeing increased liquidity pressure, credit may geometrically compound that problem. When credit risk starts to manifest on banks’ balance sheets, which it will, banks will experience liquidity pressure, the likes of which they have never seen. This is saying something given the historical quarter we just finished.