100K Clients Prove It: The Formula For Better Bank Profitability

Community banks have long debated whether profitability is driven by pricing discipline, balance sheet optimization, or credit selection. While each of these factors matters, analysis of client-level profitability across thousands of commercial relationships tells a more decisive story: bank profitability is not built through isolated transactions; it is built through relationships largely characterized by multiple product usage.

We analyzed the commercial portfolio of a bank to determine what products, scale, cross-sell opportunities, and expected life translates to profitability. The granularity of this data reflects the state of the banking industry, and the lessons learned can be incorporated by most community bankers in their daily product pricing, marketing, and sales efforts.

The difference between a highly profitable commercial client and a marginal one is rarely a single loan facility or a single deposit balance. Instead, it is the breadth of engagement – the number of products a client actively uses and the degree to which the bank is embedded in the client’s operating and financial ecosystem.

The Bank

Our case study is a bank with approximately 100k clients and $34Bn in commercial loans. We reviewed each instrument, for each client and measured the 12-months profit after funding costs adjusted for fund transfer pricing (contribution to overhead). The bank’s products included loans, deposits, treasury management, merchant payment services, hedging, and investment services. We analyzed which products and cross-sell results in higher profitability for the bank. We also considered the distribution of profitability across client relationships and industries.

Bank Profitability Results

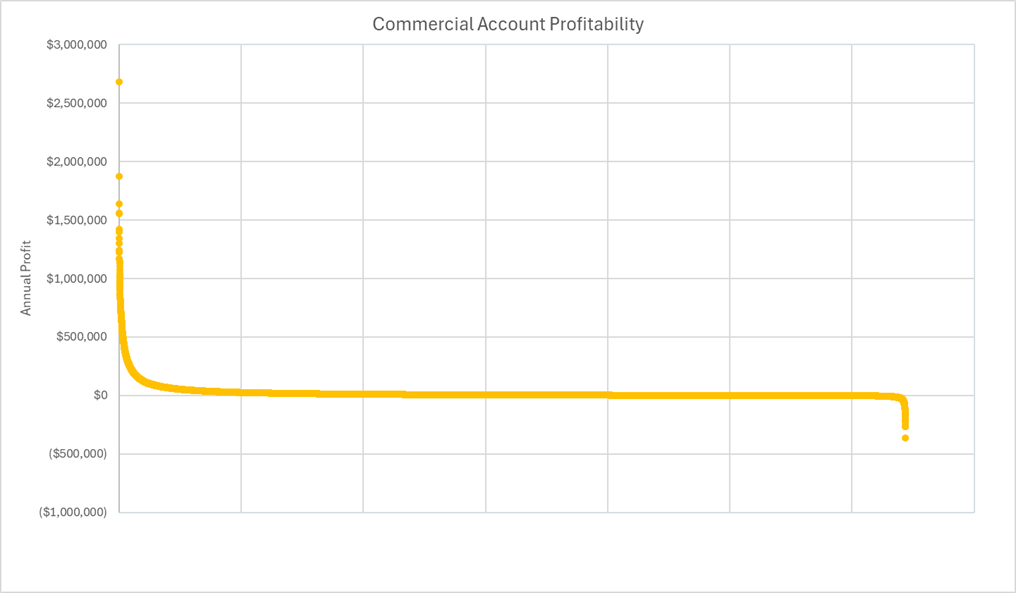

Below is a graph showing the distribution of profitability for over 100k commercial clients. The clients on the left side are highly profitable for the bank, the clients on the right side are highly unprofitable, and the clients in the middle of the graph contribute little to profitability (this distribution is common for all banks we have reviewed and for different business cycles).

We make the following observations about our analysis.

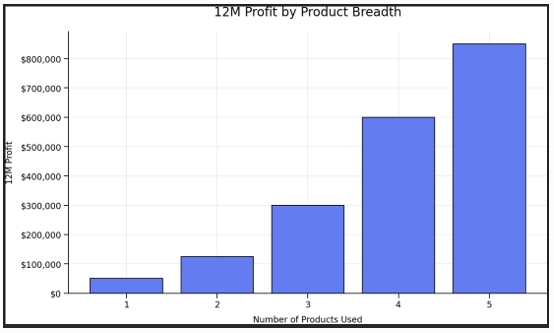

- A single-loan relationship is easier to originate, faster to book, and simpler to manage. However, while that loan product may appear profitable, it has a few weaknesses. For this bank, more products lead to higher profits per relationship as shown in the graph below. More products sold to each client translates to more profitable relationships.

- Different bank products result in varied profitability. Our analysis shows that credit products are hindered by the following:

- Thin margins (because they are high-ticket items and highly competitive).

- Higher volatile earnings with interest rate changes.

- High incidence of negative profit because of credit and rate risk.

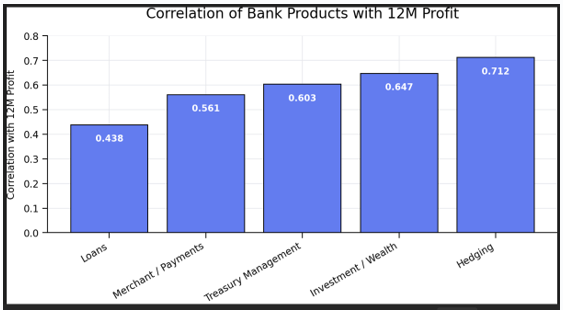

However, diversification across interest margin, fee income, and deposit spread can meaningfully increase bank profitability. The graph below shows correlation between this bank’s products and 12-month profit.

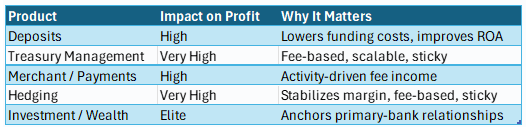

- Cross-sell drives profitability beyond revenue addition. It adds revenue diversification, lowers the cost to serve the account, improves credit outcomes and increases stickiness and retention. The graph below explains how each cross-sell product helps the bank’s profitability.

- While any additional cross-sell matters in driving profit, the analysis shows that certain combinations are particularly powerful.

- Loans plus deposits appear to be the profit foundation for this bank and others that we have studied.

- Clients that maintain both lending and operating deposits consistently outperform loan-only or deposit-only relationships. Deposits lower funding costs and improve net interest margins even when loan spreads compress.

- Treasury management is high margin and scalable. Treasury fees are high-margin and recuring revenue streams.

- Merchant and payments scale with client activity and reinforce treasury adoption, further compounding relationship economics.

- Commercial loan hedging products decrease credit and interest rate risk, create substantial upfront fee income, increase stickiness, and lead to more deposit opportunities. Commercial loans, hedging, and deposits appear to be a winning formula for many commercial banks.

- Investment services and wealth management represent fewer clients, but those that use the product rank among top-tier profitability. These relationships signal true primary-bank status.

- Industry and profitability are only loosely correlated. Certain industries have different scale, credit quality, and cross-sell opportunities. Some industries with complex cash flows and entity structures show the strongest correlation between product breadth and profitability. However, that relationship is not as strong as the size of the client and number of products used by the client. Below is the industry ranking for this bank.

![]()

Conclusion

Low-profit accounts are often labeled as “bad clients,” but the data suggests a different conclusion: most low-profit accounts are incomplete relationships, not fundamentally unprofitable clients. The common traits of these unprofitable accounts are loan-only usage, lack of treasury adoption, absence of operating deposits, and no fee-based products. We believe that cross-sell works best when it is embedded into relationship strategy rather than treated as a quota exercise.

The key implications for community banks is to measure profitability per account and instrument, incorporate relationship profitability into RM incentives, align credit strategy with cross-sell potential, and identify under-penetrated clients as growth opportunities. Community banks that consistently outperform do not ask, “How do we sell another product?” They ask, “How do we become operationally relevant to this client?”