Use This Systems Framework to Better Manage Deposits

Want to make better decisions and be a better leader? Understanding system thinking is a great unlock. Last week (HERE), we discussed the importance of system thinking and described the four main types of systems (below) that bankers need to recognize before solving a challenge. In this article, we provide a framework for managing problem solving within those systems and apply system thinking to better manage deposits.

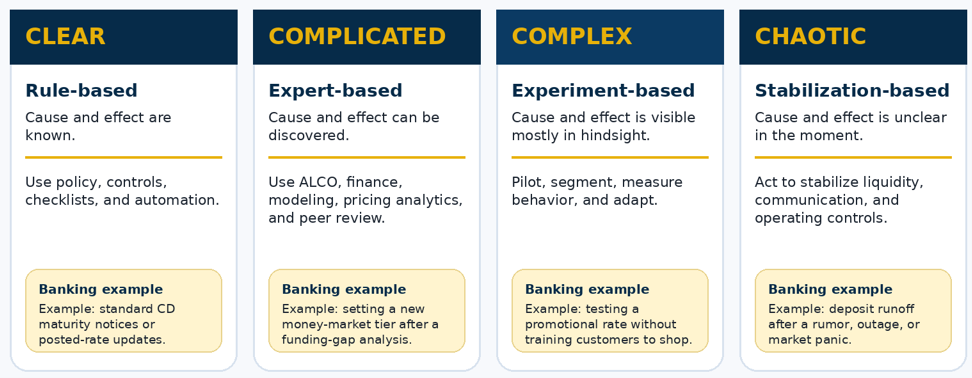

The Four Primary Systems

To recap, bankers often make decisions based on a single element instead of thinking about the impact to the entire system. A system has connections and patterns that are critical to understand to arrive at the best decision. To take the system into account, bankers must first recognize what type of systems they are dealing with and then apply the correct framework to each system. While we went into depth last week, the four systems are outlined below.

Use This Diagnostic Tool To Better Manage Deposits

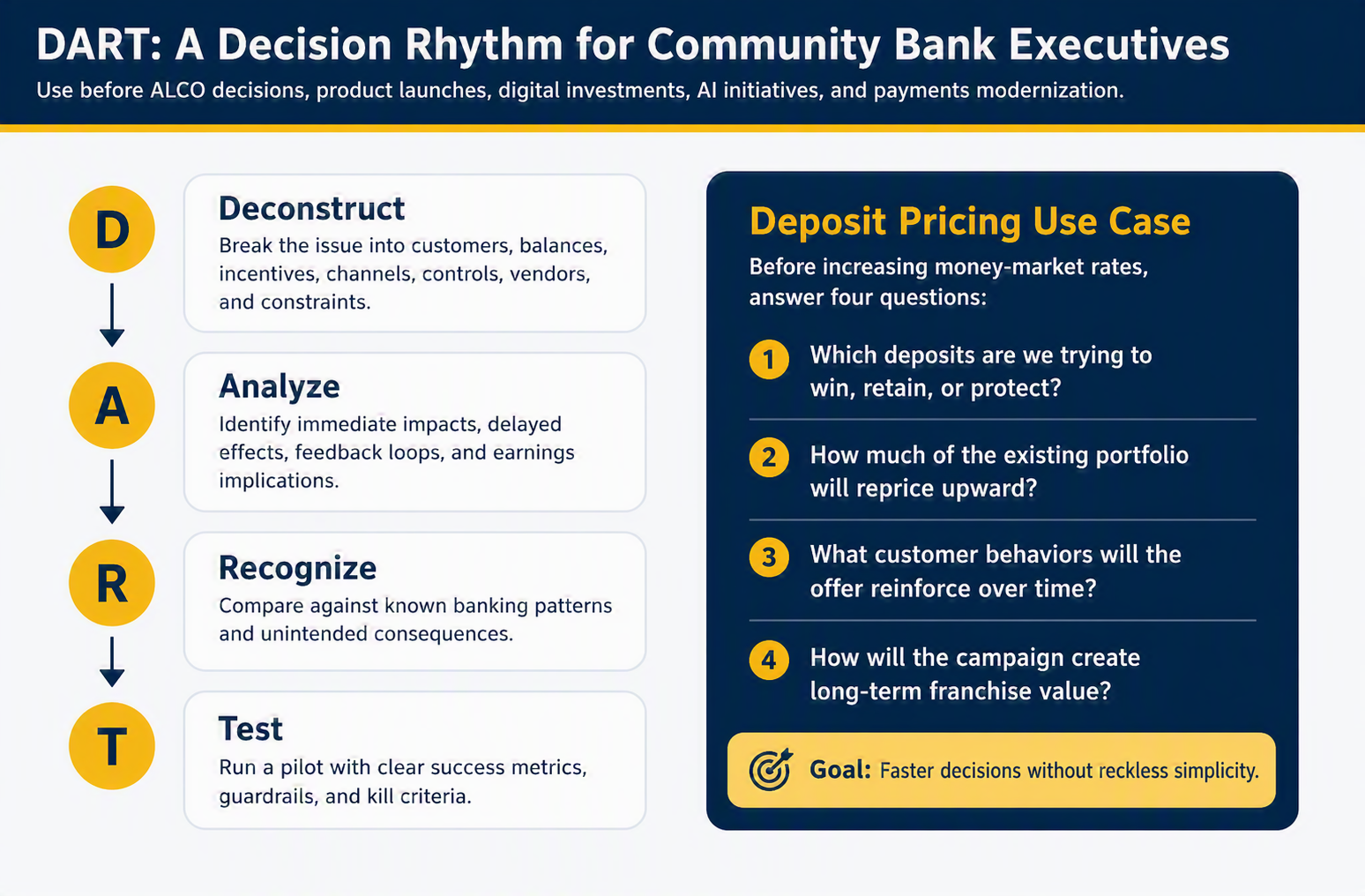

To figure out which type of system you are dealing with, a framework is helpful. This framework is known as D.A.R.T., and stands for (D)construct, (A)nalyze, ( R)ecognize and (T)est.

Deconstruct: Take a moment to understand the parts of the system. Are the parts stable, like a set of regulations, or unstable like market conditions?

Analyze: Next, ask yourself how all the parts are interrelated. This is done through the lens of an input. When you change one factor in the system, what is the cause and effect? If the causes and effects are obvious, then it is a Clear system. If the effects are not clear, but you can discover by observing data, then it’s a Complicated system. If it is difficult to tell the cause and effects because the effects change in different environments, then the system is likely a Complex one. Finally, if it is impossible to tell the cause and effects, then it is likely a Chaotic system.

Recognize: One you understand what system you are working with, then figure out are there patterns within the system or across systems that you can recognize. Past rate hikes and inflationary times are excellent starting points for understanding how to currently manage deposits during this current environment.

Test: Run a series of small tests to not only better understand the cause-and-effect relationship, but the sensitivity of those relationships. Once the data from these tests are analyzed, then you can commit to a full response. This applies to all systems except for a Chaotic system. In a Chaotic system, as we discussed, you need to shut down the entire system as best you can and then conduct the tests as you bring parts of the system back up.

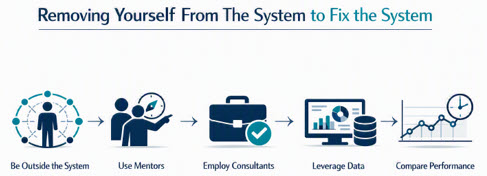

Don’t Be Trained By the System

To better manage deposits, avoid this major problem – since you are part of the system, the system influences you or trains your behavior to support the system. For deposit management, offering rate is the classic example. You offer a high rate, and you see deposit balances grow and you experience happy customers. The system becomes self-supporting.

However, this is an incomplete feedback loop since you are getting positive reinforcement from the wrong direction within the system. Because you are in the system, the system promotes balance and rate instead of deposit profitability. This is like sitting in a car trying to judge the speed of the car next to you. Unless you know the speed of the car next to you, it is difficult to comprehend the speed at which you are going.

To solve this problem, it is helpful to actually be outside the system to then observe it independently. This is why we often recommend that a bank board, CEO, or even the chief credit officer are not part of the credit approval process. They should not be part of the process so that they can better observe the process and be in a better position to opine on governance. Once you are in a system, you potentially lose impartiality.

In situations where you cannot be outside the system, then it is helpful to create a view as if you were outside the system and acknowledge your positional limitations plus your potential conflicts. Here you can use a mentor who is outside the system, or employ consultants to help provide an outside, objective view. Banks can also go to the data so they can learn what the system is doing instead of what they think the system is doing. Finally, bankers can compare themselves to what has happened in the past and then look for changes in the system to pinpoint better cause and effect relationships.

Breaking Down The Systems Within Deposit Management

Deposit management is a perfect example of a complex bank system. The mistake is treating deposit pricing as one decision. It is more than just rate. Thinking in terms of “What rate should we pay?” is too narrow of a question. The better set of questions are:

What balances are we trying to protect?

What type of customers do we want to attract?

How much existing money will reprice?

Are we buying primary relationships or temporary balances?

What behavior will this offer train?

What will happen when the promotion ends?

How will the decision change our future deposit beta?

How will it affect margin over the next 36 months?

A bank can raise rates and immediately celebrate new balances. That is the easy metric to track but possibly a harder metric to live with. The more important question is whether the bank is creating durable franchise value or simply renting money at a higher cost.

Community banks have the advantage of knowing their local market and having stronger ties to the community compared to national banks or fintechs. However, that advantage can disappear when the bank copies a rate-board strategy from institutions with different funding models, different technology, different customer acquisition costs, and different balance sheet economics.

Systems thinking helps prevent that.

Reducing The Rule Set

Often, parts of any Complicated, Complex or Chaotic system can be reduced to a Clear system. To better manage deposits, understand the parts of the system. For some parts, the cause and effect of input compared to output are known.

Structuring and issuing CDs is an example. Banks need to make sure their maturities are sufficient so as to not to conflict with the duration of their money market accounts, their redemption penalties are sufficient, so a bank isn’t giving away optionality, and marketing is active as to promote the product to the right customer base.

As we learned with any Clear system, the right response is consistency. Use policy, process, controls, scripts, checklists, and automation to control the process.

Complicated Problems Need Expertise

For the parts of deposit management that are Complicated, the cause and effect can be discoverable, but only with analysis and expertise.

Managing product, pricing position, marketing, and interest rate sensitivity are all example of this this. Deposit management has such an outsize impact on bank value that most likely the bank’s effort requires at least one full-time dedicated person managing the effort across the bank.

In addition, a bank may want to bring in a consultant or third party to help manage the complicated system parts. For deposit management, a bank needs data, finance, ALCO input, market intelligence, segmentation, elasticity assumptions, and margin analysis.

The right response for these parts of the system is expert analysis, either internally or externally.

Complex Problems Need Experiments

In general, most of deposit management is Complex. Here, the cause and effect may only become clear in hindsight because customers, competitors, employees, and markets react to each other.

This is where deposit management becomes dangerous. A promotional money market rate may look successful after 30 days. Balances rise. New accounts open. The campaign works.

But six months later, the bank may discover that existing customers repriced upward, rate-sensitive customers left after the promotion, frontline teams learned to lead with rate, and the bank increased its future funding beta.

That is a complex-system outcome. The first-order effect looked good. The second-order effect weakened the franchise.

The right response is not blind confidence in a forecast. The right response is controlled experimentation to better understand the second order effects.

Test by segment. Test by geography. Test by balance tier. Test by relationship depth and customer type. Define success before launching. Measure behavior after the initial campaign period. Watch for cannibalization, churn, product mix shifts, and changes in relationship profitability.

Once these tests are complete, then expand the strategy or tactic to the rest of the system.

Chaotic Problems Need Reduction and Stabilization

Of course, some parts of deposit management can turn Chaotic such as was the case with the SVB and First Republic liquidity run. The immediate cause and effect was unclear at the time when panic set in. These banks knew they had a problem but were unclear the size and breadth of the problem.

The combination of the large depositor composition, rapid rise in interest rates impacting the mark-to-market on those banks loans and investments, social media, and short-sellers all gave indications to bank management that they were dealing with a Chaotic system.

In chaos, the first job is not analysis. The first job is stabilization. This usually means shutting down the system to its bear minimum.

Here, banks need to be prepared to create a command structure. The sole focus should be to protect the bank’s customers and protect the bank so you can live to see another day of protecting customers. Over communicate. Preserve liquidity. Establish facts and start to break apart the system.

Once stable, banks can revert to a Complex system and start to turn parts of the system back on so that they can learn, model, and adapt.

Banks sometimes struggle here because banking culture rewards deliberation. Deliberation is valuable in Complicated situations. It can be dangerous in Chaotic ones. Every bank should have a workable emergency liquidity plan to include the daily, and even hourly limits where you recognize you have moved from a Complex to a Chaotic system. Once limits are reached, liquidity outflow is halted.

Using The Feedback Loop To Better Manage Deposits

For everyday deposit management, look to improve your current management of the system. The deposit pricing system usually works like this:

- The bank raises a rate or launches an incentive.

- The immediate signal is positive: balance growth, account openings, customer retention, and production wins.

- Then the system responds: existing customers ask for the same rate, rate shoppers arrive, bankers begin leading with price, competitors react, and the bank’s future rate sensitivity increases.

The delayed result shows up later: margin pressure, cannibalization, promotional runoff, higher beta, lower relationship value, and weaker pricing discipline. This is why the deposit executive should not only ask, “Did balances increase?”

The better question is, “What customer and employee behavior did we create?” That question changes the entire conversation.

A deposit campaign that attracts operating accounts with treasury services, payments activity, lending relationships, and stable balances is vastly different from a campaign that attracts rate-only balances from customers who have no intent to build a broader relationship. Both may produce the same initial balance growth. Only one improves the franchise.

To Better Manage Deposits – Use DART Before Changing Rates

The DART framework is useful because it gives executives a simple operating rhythm: Deconstruct, Analyze, Recognize, Test. For deposit pricing, that rhythm looks like this:

Deconstruct: Break the pricing decision into its real components.

- Who are the customers?

- Are they existing or new?

- Are they retail, small business, commercial, municipal, nonprofit, HOA, property management, professional services, or wealth clients?

- Are balances operating balances, excess liquidity, investment alternatives, seasonal funds, escrow funds, or pure rate-shopping balances?

- What channels will source the money?

- Will the offer be branch-led, digital, relationship-manager-led, treasury-led, or marketing-led?

- What are the constraints? Liquidity need, margin targets, capital plan, local competition, digital competition, customer expectations, operational capacity, and board risk appetite all matter.

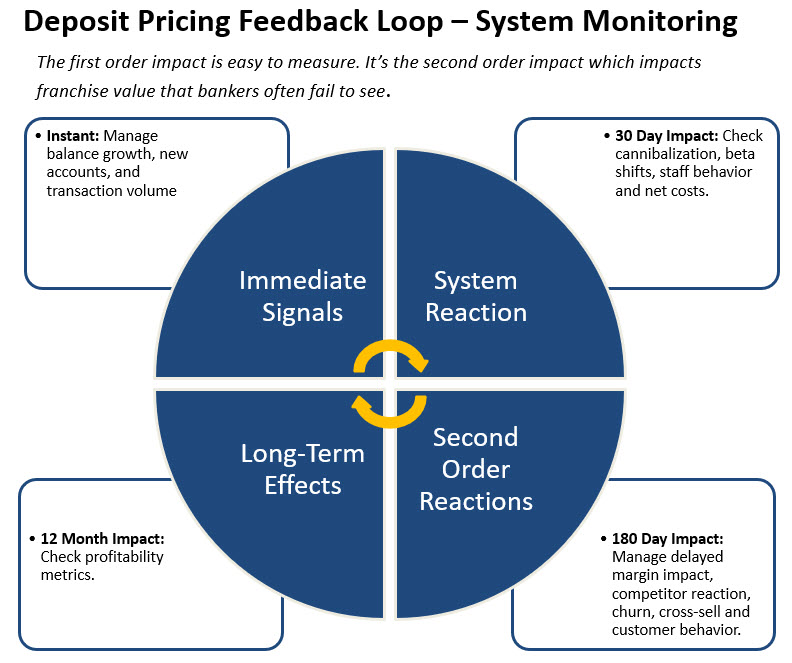

Analyze: Map the immediate and delayed effects.

A strong deposit-pricing analysis should include more than expected balance growth. It should estimate cannibalization, repricing existing balances, decay, promotional cliff risk, cost of funds, marginal profitability, and relationship value.

The bank should analyze the impact around three time horizons:

- 30 days: balances, account openings, funding mix, and production.

- 180 days: repricing, cannibalization, retention, and early runoff.

- 12 months or more: beta, churn, margin impact, relationship expansion, and lifetime value.

The 30-day dashboard tells the bank whether the offer moved money. The 12-month dashboard tells the bank whether the offer created value.

Recognize: Once a test or full-scale production is implemented (depending on the strategy), look for familiar banking patterns.

- Is this a rate-shopper problem?

- Is this a cannibalization problem?

- Is this a liquidity gap problem?

- Is this a frontline incentive problem?

- Is this a competitor-response problem?

- Is this a customer communication problem?

- Is this really a product design problem masquerading as a pricing problem?

Community banks have deep institutional memory. The problem is that memory is often scattered across finance, retail, commercial, treasury, marketing, operations, and ALCO. Systems thinking turns that scattered experience into a shared executive conversation.

Test: Do not make the first move the biggest move.

A community bank can test a pricing strategy by market, customer segment, product tier, balance threshold, channel, or relationship depth. It can cap the offer. It can require operating-account behavior. It can limit the offer to new money. It can pair rate with treasury services. It can reward relationship expansion instead of raw balance growth.

The bank should define the kill criteria before launch.

For example:

If more than a certain percentage of balances come from existing money, stop. If balances decay faster than expected after the offer period, stop. If the cost of funds exceeds the modeled threshold, stop. If new accounts do not produce cross-sell or operating activity, redesign the offer. If frontline teams begin leading with rate instead of relationship value, retrain.

Testing is not hesitation. It is disciplined speed. Deposit testing is a 365, always-on effort. Banks should always be running multiple deposit tests in the background. Even if a bank doesn’t need to raise deposits, the data is invaluable the day you want to move to deposit raising or deposit mix changes.

Using System Thinking Beyond Deposits

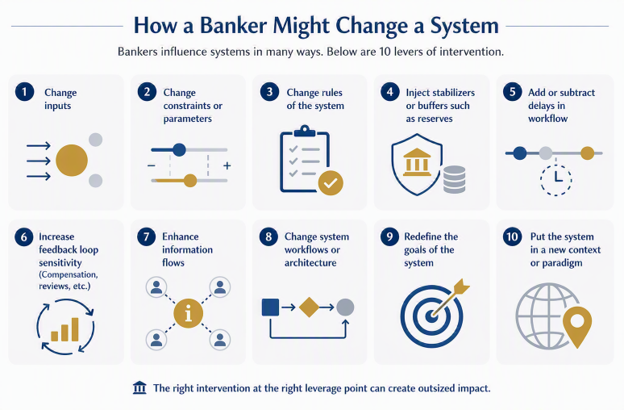

Deposit pricing is the clearest example, but the same thinking applies across the bank. For money movement, instant payment rails create new customer value but also change fraud speed, exception handling, liquidity timing, and operational risk. In stablecoins and tokenized deposits, the question is not only whether the technology works. The question is how customer behavior, liquidity, settlement expectations, and regulatory treatment may change the deposit franchise.

In AI, productivity gains are real, but adoption changes workflows, quality control, training, vendor risk, and accountability. In fraud, a control that reduces one loss type may push criminal activity into another channel. In digital strategy, a new payment feature may complicate the movement to a payment hub thereby hurting adoption, usage, fees, and balances.

The executive banking skill is not simply solving the visible problem. It is understanding the system that produces the problem.

Putting This Into Action

To better manage deposits, turn to strengthening your systems thinking. Managing deposit performance is just one of many bank systems. Deposit pricing is not just a math problem; it is a system problem. Having a system view will help banks understand the various decision options to help more effectively manage deposit performance.

Systems thinking gives executives a way to move quickly without becoming reactive. It helps the bank distinguish between a temporary funding need and a permanent shift in customer behavior. It helps leaders decide when to use a rule, when to use expert analysis, when to run a pilot, and when to stabilize a crisis.

Intelligence helps a bank solve problems, but system thinking provides the wisdom to help recognize which problems you’re solving.