Every Bank’s Deposit Vulnerability (Find Yours)

There is an explosion of entities waiting to become banks. In the last 60 days for example, no less than six bank applications were filed (including the formidable Revolut Bank). Behind that, there are a rash of new competitors coming to include banks by Affirm, PayPal, World Liberty, Mercury, NuBank and UKG. Most will create additional deposit competition. Add to that rising rates and greater competition from money market funds, plus the onslaught of tokenized deposits and stablecoin, and this formula adds up to more competition for bank deposits. In this article, we show which banks have the greatest deposit vulnerability and are the most vulnerable to losing market share.

Deposit Vulnerability Index Calculation

We teamed up with Amberoon to create a Deposit Vulnerability Score which adapts the deposit stress-dimension from the Basel III Liquidity Coverage Ratio. This is the same conceptual framework U.S. regulators apply to banks >$50B in assets. The Fed’s CCAR/DFAST stress tests use a similar set of inputs (depositor-stratified run-off rates, wholesale-funding mix, time-deposit reliance) to assess deposit-flight risk under adverse scenarios.

All inputs are standard regulatory measures sourced from FFIEC Call Reports and UBPR.

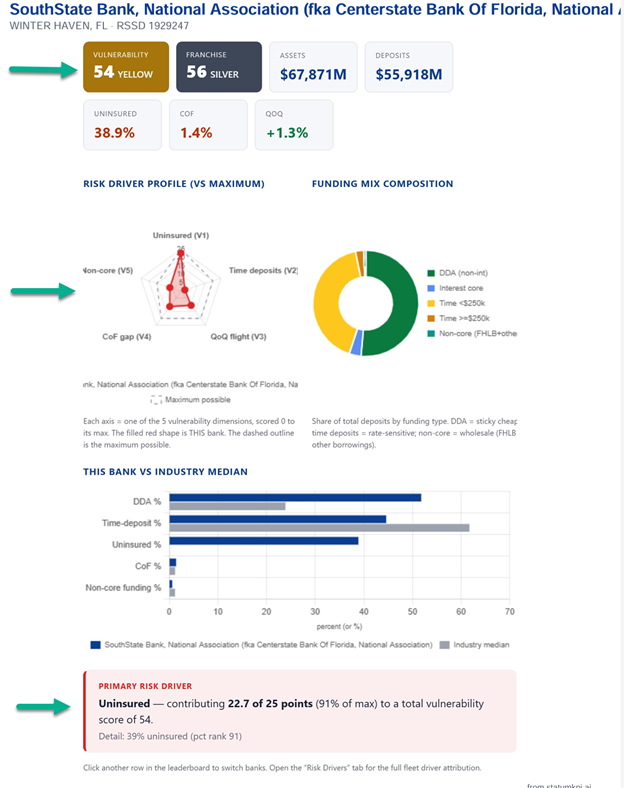

The Vulnerability Score takes into account:

- Uninsured deposit %

- Time-deposit %

- QoQ negative deposit balance change

- Cost of funds

- Wholesale / non-core funding

Weights were then applied to these factors to produce a Vulnerability Score from 0 to 100 (Most vulnerable). Bands of red, yellow, and green where then created off those bands.

We then look at similar metrics to arrive at the inverse of the above that is called the “Deposit Franchise Score.”

Franchise Score takes into account:

- DDA %

- COF below peer

- QoQ positive deposit balance change

- Low uninsured deposit reliance

- Low non-core funding percentage

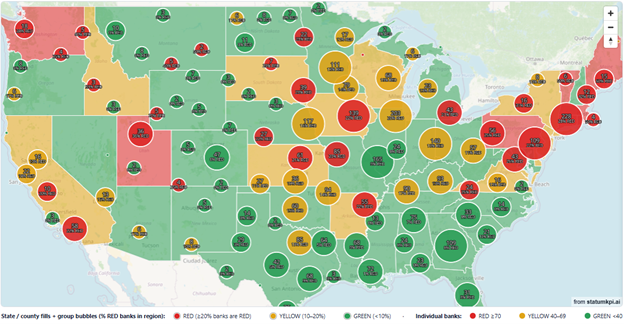

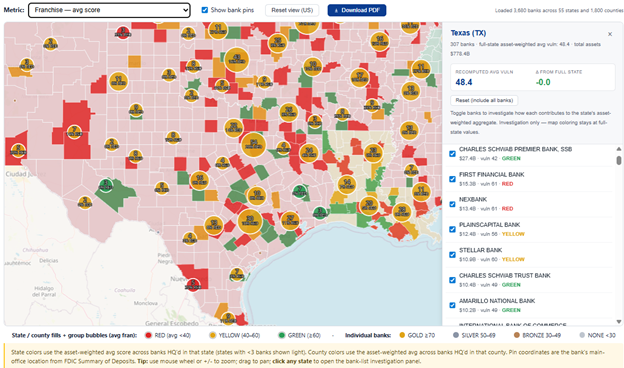

We have mapped each bank, their state deposit vulnerability plus you can also drill in to the county-level (Texas below):

In addition, you can look up your bank to see your score, the composition of that score, a graphic of the risk profile and the single most impactful item to make your bank less vulnerable to deposit flight.

Putting This Into Action

This is just one of many methodologies to assess vulnerabilities and deposit franchise value of banks. For banks looking to improve their position, in addition to the recommendations on this tool, we also published the 7 Tactics to Implement in a Rising Rate Deposit Strategy that can help any bank, regardless of score, improve their deposit franchise value.

To see your bank or your competitors, check out the Deposit Vulnerability and Franchise Analysis tool complete with 1Q 2026 data (HERE).