7 Tactics to Implement in a Rising Rate Deposit Strategy

It is clear that we are not going to get a rate cut for the rest of the year. Unfortunately, most banks have built in two or more rate cuts into their budget. While a rate cut has been statistically off the table since January, many banks still have not adjusted their deposit strategy and tactics to optimize performance for the rest of the year. In this article, we highlight seven tactics to employ as part of a rising rate deposit strategy with the goal of increasing deposit value in a static to rising rate environment.

A Rising Rate Deposit Strategy in a Static to Rising Rate Environment

When rates fall, the strategy is to offensively lower rates while making your deposit base less interest rate sensitive. Falling rates are a time to restructure your deposit base to improve your performance by reducing your deposit beta when rates eventually rise.

When rates are threating to increase, banks should move from offense to defense with the goal of limiting higher deposit costs. One of the best ways to do that is to focus marketing and sales effort on higher balance accounts with the goal of limiting deposit cost and sensitivity.

This single strategy can be so effective, yet many banks overlook a distinct deposit strategy designed for a rising rate environment and a fewer number of banks focus on high-balance accounts.

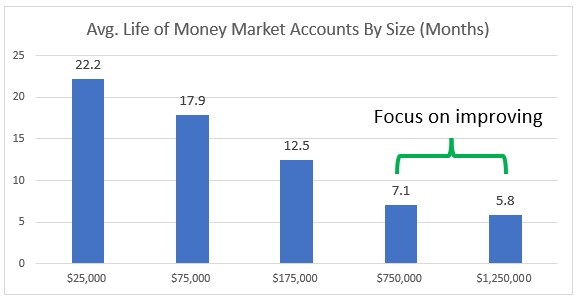

Deposit Performance by Balance

Below is sample decay data of money market accounts based on account size. As you can see below, without interventions, the average small balance account will stay with a bank for four to five years with an average life of almost 25 months. This is more than three times the life of a money market account that has average daily balances above $1mm.

When rates rise, money market rates are often above bank offered rates, not only taking balances away from banking, but pressuring banks to increase their deposit rates to compete. If that is not bad enough, banks often compound their problem by growing loans faster than deposits.

When interest rate sensitivity increases, it is likely to increase on larger deposit balance accounts first and most. Another way to look at this is that higher balance accounts usually shorten their average life quicker than lower balance accounts.

Given this defensive deposit strategy, banks may want to employ the following tactics:

Step 1: Improve Your Data

As Sun Tzu says, every war is won before it is fought. Like war, deposit gathering success lies in the preparation which starts with data. The best deposit gathering banks track deposit beta and runoff by engagement cohort. Data should be broken down at a minimum for customers with various balance tiers, direct deposit, multiple products, type of products in the relationship, app usage, service satisfaction/net promotor score, or advisory interactions.

This data can then be leveraged and analyze using machine learning techniques to determine what tactics work best for your bank given your customer base. Each cohort can be compared against unengaged, high-balance customers.

Step 2: Increase Marketing and Sales Effort

This data suggests that if you were going to spend money on customer retention, you might want to start by targeting those customers with over $500k in balances. This is the area where you can move the needle the fastest.

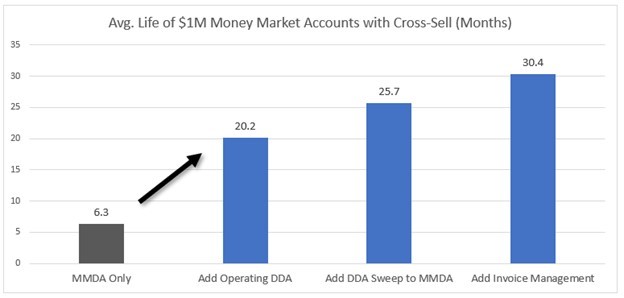

One of the best moves a bank can make is to increase cross-sell. Getting a customer to use your treasury management services has proven to be one of the best marketing and sales moves a bank can make. However, if you can’t do that, adding additional demand deposit, savings or money market accounts can also serve to increase retention and lower the interest rate sensitivity of the account.

For that matter, adding any additional services help this effort to include bill pay, invoice management, cash flow projections or alerts. Below is an example of the before and after snapshot of a $1mm money market account once you start adding other product connections that boost account longevity.

That increase in retention by more than five times is worth almost $18,000 to the average bank in a static environment and multiple times that in a rising rate environment. Spending sales and marketing dollars on these accounts can provide one of the better returns in bank marketing.

Almost all additional services help deposit performance to include wealth products, mortgage, payroll, card programs, or fraud tools.

To accomplish this cross-sell, there are several different tactics in addition to increasing marketing and sales effort.

Step 3: Bundle Relationship Value

To entice customers to open additional accounts or use additional services, banks should move to relationship pricing so that the customer, and the banker, are incented to open additional accounts or use additional services. To promote this cross-sell, banks should consider lowering fees, offering fee waivers, bundling free services, increasing analyzed transaction account yield, or as a last resort, offering higher rates for not only more balances but more accounts.

By offering bundled relationship pricing, banks move their product offerings away from being commodities and towards rewarding customers for the entire relationship.

Step 4: Segment High-Balance Accounts Further

A $750,000 retail savings account, a small business operating account, a municipal deposit and a wealth client’s emergency liquidity reserve all behave differently. Once you have segmented by account size, banks should also review their data by intent to include operating accounts, investment balances, emergency liquidity, specialty accounts, and uninsured deposits.

When it comes to specialty accounts, bankers can suggest and assist in bifurcating balances for specific needs such as to pay taxes, to establish a capital expenditure replacement fund, or to set up emergency reserves. Each one of these specialty accounts is not only likely to increase duration, but it also helps bankers better gauge the interest rate sensitivity of the remaining balances by better isolating those funds that are most susceptible to leaving or demand higher rates.

Step 5: Increase Advocacy

Customer engagement can reduce interest rate sensitivity when it creates trust and value. Now is the time to increase outbound calls and visits to not only increase the frequency of touches, but to deliver advisory quality to each account. A quarterly “cash optimization review” can help increase communication with the client while better understanding how the customer thinks about their excess liquidity.

While conducting these reviews, each customer should be scored as to their expected rate sensitivity, the output of which can be added into a sensitivity metric such as we advocated for HERE.

Step 6: Help the Customer Ladder

While we are not fans of certificates of deposits, this is where they have their place. For customers that insist on yield, then build them a CD ladder starting at 14 months and extending out. This helps protect money market and savings accounts while forming a contract with the customer. Banks need to make sure they had adequate prepayment or cancellation structures, but if they do, then a bank gives away yield now in anticipation of higher future rates and increasing deposit sensitivity. A bank also improves funding stability and extends duration of their deposit structure.

If an above market rate is demanded, then a bank can move to a puttable CD structure where the bank retains the option to redeem the CD thereby providing better convexity and deposit performance.

Step 7: Develop Deposit and Payment Products

The goal here is to drive deposit value with attributes other than rate. Tokenized deposits allow banks to leverage the blockchain as their modern core and create an infinite amount of specialty deposit products leveraging smart contracts. Payment products that release funds upon the receipt of products, loyalty rewards, accounts that pay higher rates of interest when you don’t withdraw funds, senior accounts that require payment approval for payments above a certain level and many more ideas are examples of what banks are creating now in preparation for higher rates.

In addition to tokenized deposits, instant payments, request for payments, pay-by-bank, international P2P payments and many other payment products can be used to drive non-interest rate sensitive balances.

Putting This Into Action

The time to institute some of these tactics is now BEFORE rates start moving up. Banks cannot make high-balance accounts insensitive to rates, but they can make them less rate driven. The winning tactic here is to leverage data and analytics to identify rate sensitive accounts, while increasing sales and marketing efforts on those at-risk accounts. Banks need to institute retention pricing while increasing relationship depth through engagement and advisory effort.

Some banks, for example, do nothing more than having their CEO call the largest depositors twice per year to check-in and thank them. This alone can have a material impact on retention and is inexpensive.

Before you spend your sales and marketing resources haphazardly, all the while being concerned about slowing deposit growth, consider getting more focused on how you spend your effort. Targeting high balance accounts to improve their average life is one of the best uses of bank marketing dollars there is in a rising rate environment.

Do this now before rates do go up.

For more ideas, and execution plans, attend our upcoming deposit conference HERE. One idea will pay for itself.