Why the $3,000 Cash Bonus Offer Makes Sense

In the trenches of the battle for deposits, banks have ratcheted up their tactics. While some banks pay customers a 4.25% interest rate for funds in a money market, other banks, such as Chase, Citi, Capital One, PNC, and others, pursue a tactic of offering a near-up-front cash bonus to open the account. In this article, we will examine the effectiveness and profitability of a cash bonus offer in acquiring customers and generating deposits.

The Cash Bonus Offer Structure

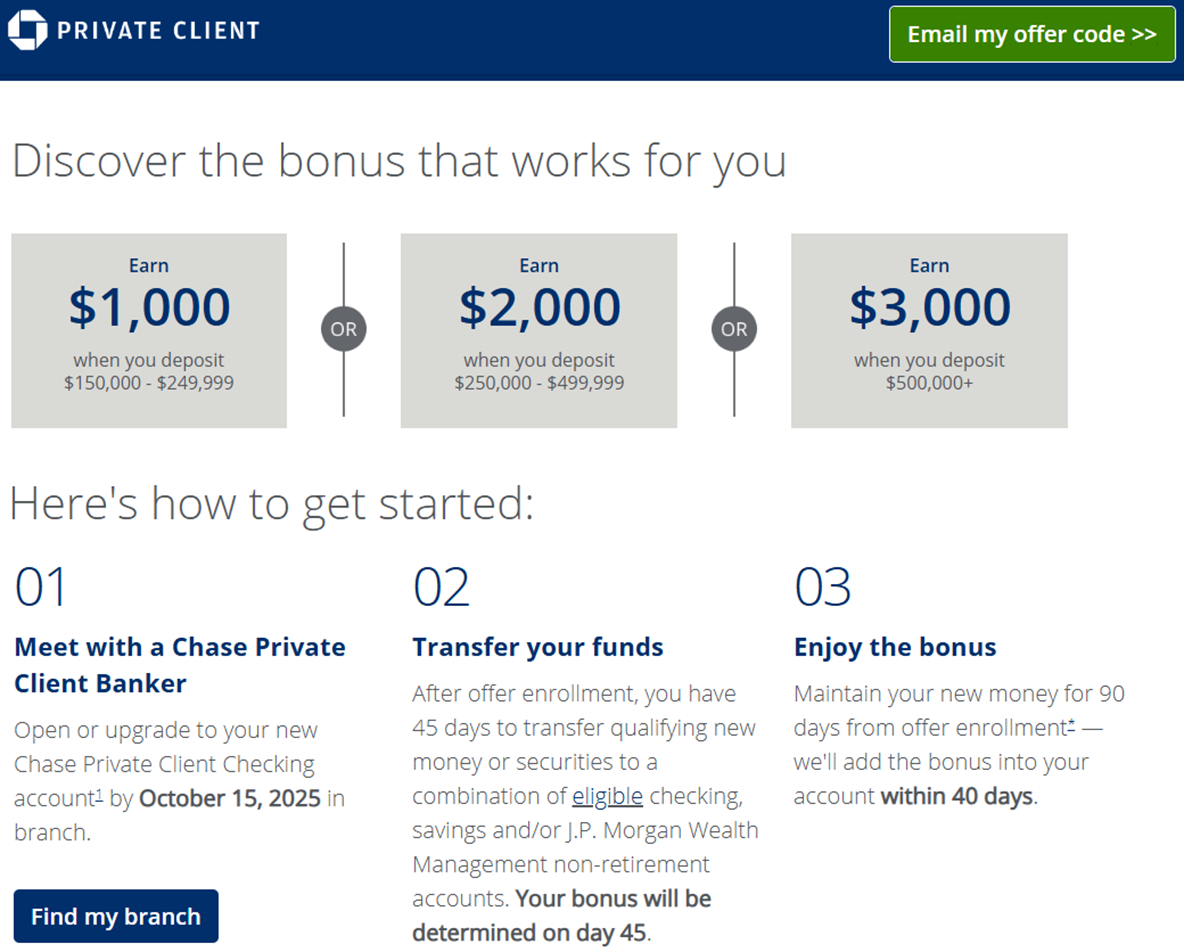

The success of the cash bonus offer hinges on the “headline number,” which can be an attractive incentive for potential customers. The competition started heating up about ten years ago around the $200 upfront cash bonus offer and quickly progressed to $400. Following the Pandemic and interest rates fell, offers declined until early 2024, when banks began to notice a quarterly loss of deposits due to higher money market rates and quantitative tightening. The $400 offer rose to $600, then $800, and finally to $1,000, where it remained for most of 2024. For 2025, Chase fueled the competition at $1,500, which is currently the most common non-private banking top offer. For private banking, Chase recently moved to offer a $2,000 and a $3,000 cash bonus.

The structure looks similar to the following for most banks:

- Open a transaction account (i.e., new customers only)

- Reference or provide proof of the offer invitation

- Proof of a W-2

- Deposit the minimum required balance (outlined below).

- Maintain that minimum balance for a period of 90-120 days, and you will receive the cash bonus.

Some banks institute a direct deposit requirement, while others provide the earnings in a companion savings account, requiring you to open both a transaction account and a savings account. Card-oriented banks, such as Chase and Capital One, sometimes couple the offer with credit card spend, while regional banks may include a debit card requirement.

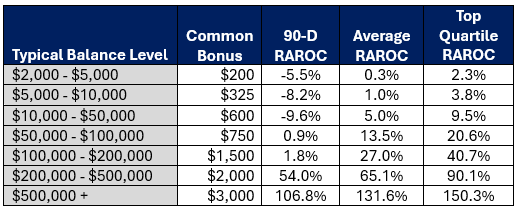

Cash Bonus Offer Account Profitability

Using our profitability model, Loan Command, we can model the minimum contractual risk-adjusted return on capital (RAROC), the average ROE for an account, and the top quartile ROE, allowing bankers to see the range of possibilities.

As expected, smaller balance level requirements are less profitable due to the cost of onboarding relative to the cumulative lifetime value of the account. If you assume the customer is going to quickly “promotion hop” and they are going to take their money out once they have fulfilled their obligation, then most offers below $55,000 lose money. However, that is not usually what happens.

Churn, Retention, and Survivability

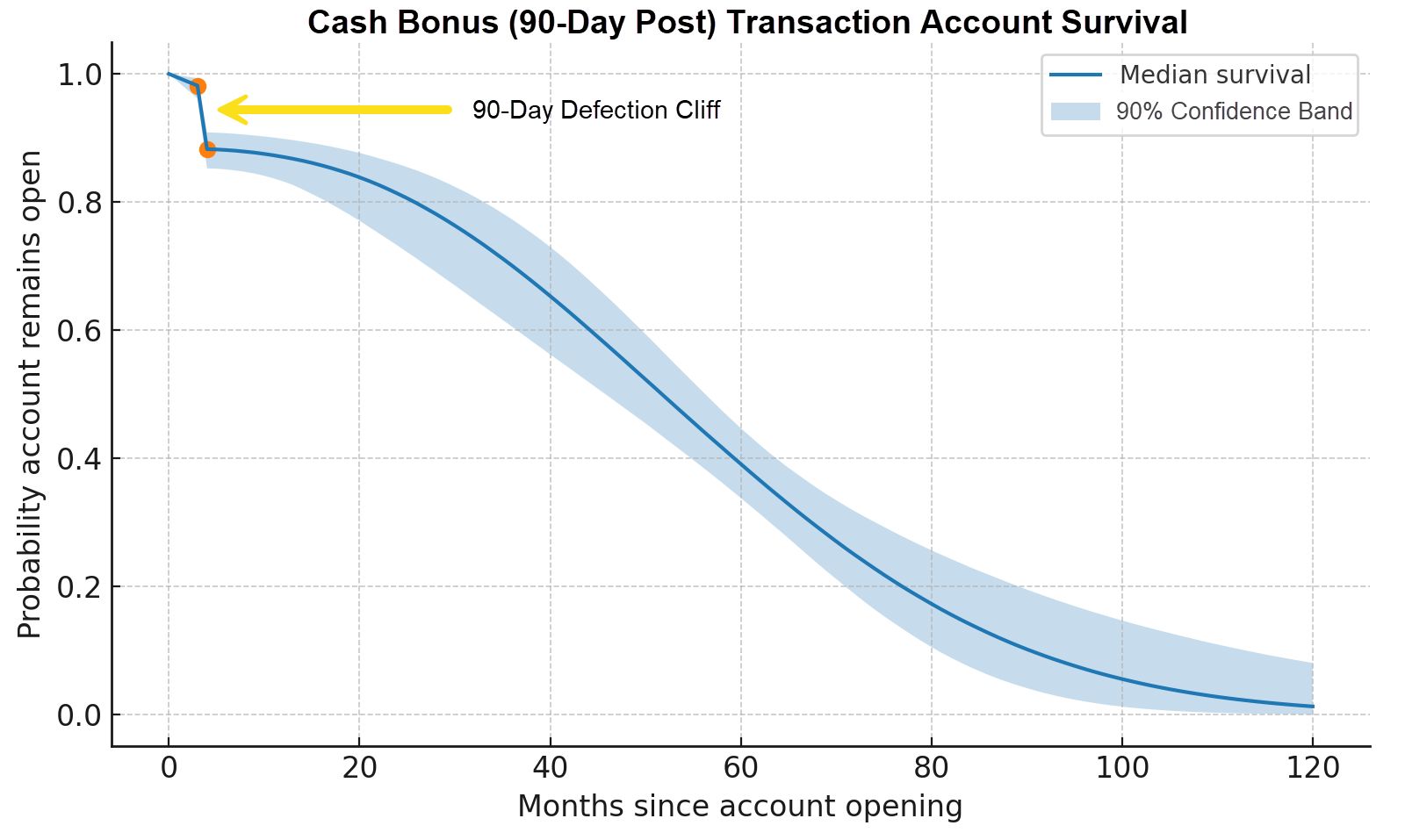

Luckily, a combination of a bank’s brand, service, and account moving friction keeps the customer at the bank. While the 90-day churn rate depends on the posting date, bank, initial balance deposited, and geography, on average, only between 10% and 13% leave the bank once they receive their cash bonus (note the 90-day defection “cliff” below). Interestingly, customer satisfaction goes up after the cash bonus is deposited, aiding in retention. As such, customer retention looks like the following (based on the cash bonus earnings date and posting date, which are at 90 days):

Once you past the cash bonus posting period at the bonus-sensitive customers defect, the remaining customers follow a similar path as other non-rate product promotions with most customers lasting an average of 47 months.

Of course, like any deposit promotion, the goal is to onboard customers and then have a plan to cross-sell other products, not only for profitability but to increase retention and lower churn. This is one reason why having a federated onboarding application (additional onboarding data HERE) is critical in banking to be able to add products and services during the account opening process. If you do, cumulative lifetime profitability dramatically improves.

Outside of the onboarding process to increase cumulative lifetime value and retention, banks need an automated marketing campaign or a manual sales effort to cross-sell direct deposit, debit swipes, instant payments, loyalty programs, balance building, savings accounts, and credit products.

Another simple tactic that is free and provides an outsized return on effort is a brand campaign. Remarkably, many banks lack a standard drip marketing campaign during the first six months of onboarding, which could promote their brand, culture, and community service. The first 90 days are statistically critical (More on the Recency Effect in banking HERE) to encourage both the bank’s brand and other products. An educational series is almost effortless and can dramatically increase satisfaction scores while slowing churn and increasing transaction account survivability.

Banks that can build their brand and cross-sell products early often move their customers into the top quartile of profitability and achieve the RAROC numbers on the right of the above profitability matrix.

Don’t Make This One Critical Mistake – These are Not Rate-Sensitive Customers

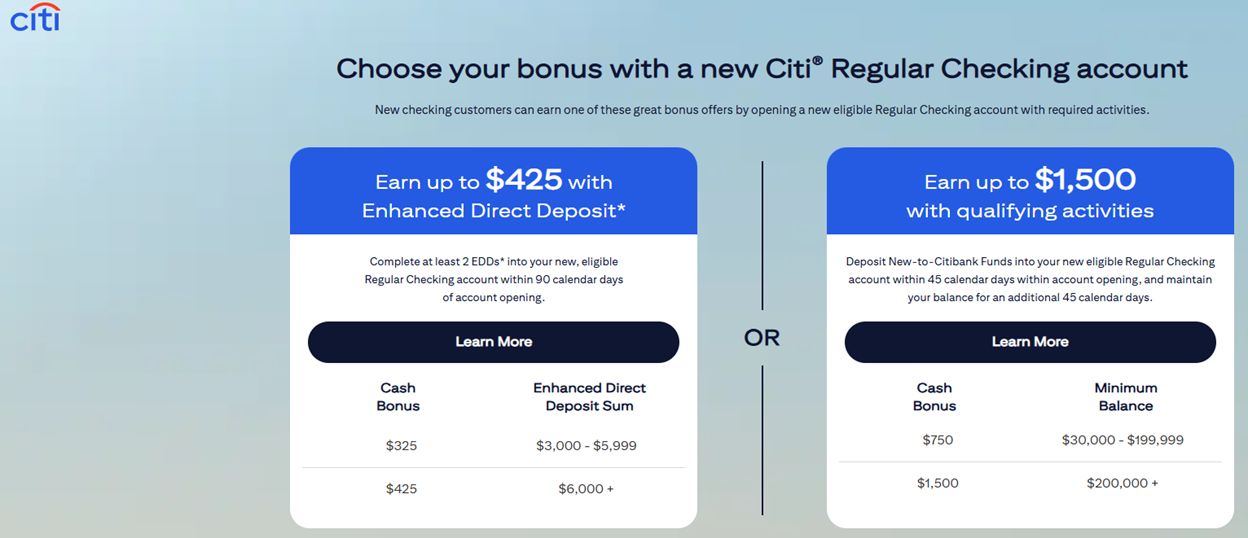

Occasionally, banks will get in their own way and want to offer a high rate of interest similar to the promotion below, where not only do you earn $425 cash bonus for opening an account with $11,000 minimum balance, but you also earn a teaser rate of 4.25%. This not only makes the account less profitable, but it also undermines the strategy.

The critical element to the cash bonus offer is that you are attracting a non-rate-sensitive customer. Although attracting a customer with a cash bonus isn’t significantly better, it is an improvement. What you don’t get is the rate chasers that moves money at will. You don’t incur the additional cost of managing customer complaints when you ultimately drop the rate to improve profitability. The majority of the cash bonus customers are those accounts looking to change banks anyway, and your bank provided them an extra catalyst. By offering a high rate of interest, you now attract a different customer with a higher deposit beta, a higher maintenance cost, greater churn, and lower cumulative lifetime profitability.

The other problem that banks run into when they offer both a cash bonus and a high rate of interest is that it confounds your interest rate sensitivity model (HERE), so it takes additional time and effort to see the customer’s reaction at the next rate change.

When offering a cash bonus to open a transaction or treasury account, it is best not to also add a high rate of interest.

Banks That Use This Strategy

Because of the success of this strategy, a host of banks have jumped on this promotion either with a single cash bonus set of offers or using a “progressive tactic” whereby they send a targeted mailing or email. If the prospect doesn’t bite on an offer, they increase the amount of the bonus (BMO does this well).

Below is a sampling of the most popular cash bonus marketing efforts by banks.

Chase: $100, $300, $1,000, $2,000 & $3,000 (also uses it for business accounts at the $300, $500 and $1,500 levels HERE).

Citibank: $425 & $1,500

PNC: $460 and $600 for consumer, $400 and $1,000 for business

Bank of America: $100, $300 & $500

BMO: $460, $600 & $750

Capital One: $250, $450, $500 + Up to $2,000 for credit card usage

Huntington: $400 & $600

KeyBank: $300 & $500

US Bank: $250, $350 & $450

Wells Fargo: $325 for consumer and $400 for business

Putting This into Action

If you need to attract customers and deposits, consider the cash bonus strategy before offering a high-interest rate. While your cost of acquisition is higher compared to a high-yield offer, your performance is markedly better. A $600 cash bonus offer for a $25,000 has the equivalent of a 0.60% per annum cost of funds. With no cross-sell or retention effort, that cash bonus account has an average ROE of 5% vs. a 0.6% ROE for a high-yield money market account indexed to Fed Funds.

If you are looking to build deposits and still achieve superior deposit performance, consider the cash bonus offer.