5% of Loans. 16% of Profit: The Case for Commercial Loan Hedging

Our data and analysis strongly suggest that banks that can measure instrument and relationship level performance for ROA and ROE can improve simply by reallocating capital and resources to more profitable relationships and improve performance by strategic cross-selling. We measured how commercial loan hedging, where interest rate risk is removed, credit margin is properly determined at inception, and maintained through the life of the loan, compares to that same bank’s non-hedged commercial loans.

Our results are insightful for community banks who may be considering commercial loan hedging or those that are questioning the merit of continuing such a program. When examining client profitability data, one conclusion emerges clearly: a meaningful portion of negative profit accounts are not the result of bad credits – they are the result of unmanaged interest rate risk and pricing erosion.

The Bank

Our case study is a bank with approximately 100k clients and $34Bn in funded commercial loans. We reviewed each instrument, for each client and measured the 12-months profit after funding costs adjusted for fund transfer pricing (contribution to overhead). This bank has booked fixed-rate loans on their balance sheet and serves as a good comparison since their fixed rate loans are both hedged and unhedged.

Results on Commercial Loan Hedging

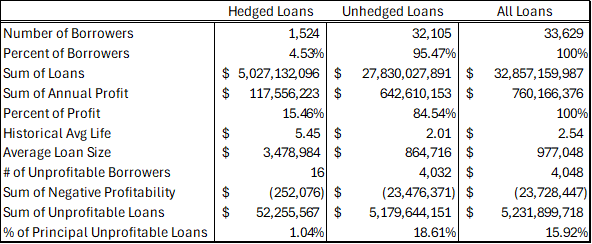

Of the total 33.6k loans, 4.5% are hedged loans. The hedged loans are on average $3.5mm in size compared to $864k in unhedged loans, and the hedged loans contributed 15.6% of annual profit for the bank. Also striking is the historical average life of the hedged versus unhedged loans. The table below summarizes this bank’s hedged and unhedged loan portfolios.

The important takeaways from the table above are as follows:

- While hedged loans represent a minority of total relationships, they contribute a disproportionate share of total profit. The hedged loans are significantly larger and more unprofitable.

- Hedged loans are less likely to be negatively profitable. Hedged loans are more resilient to profit erosion during interest rate movements.

- Hedged loans are stickier and lead to more cross-sell opportunities. The average life of a hedged loan is 5.5 years versus 2.0 for unhedged loans. For this bank, the hedged loans are more correlated with higher profit for the bank and higher cross-sell.

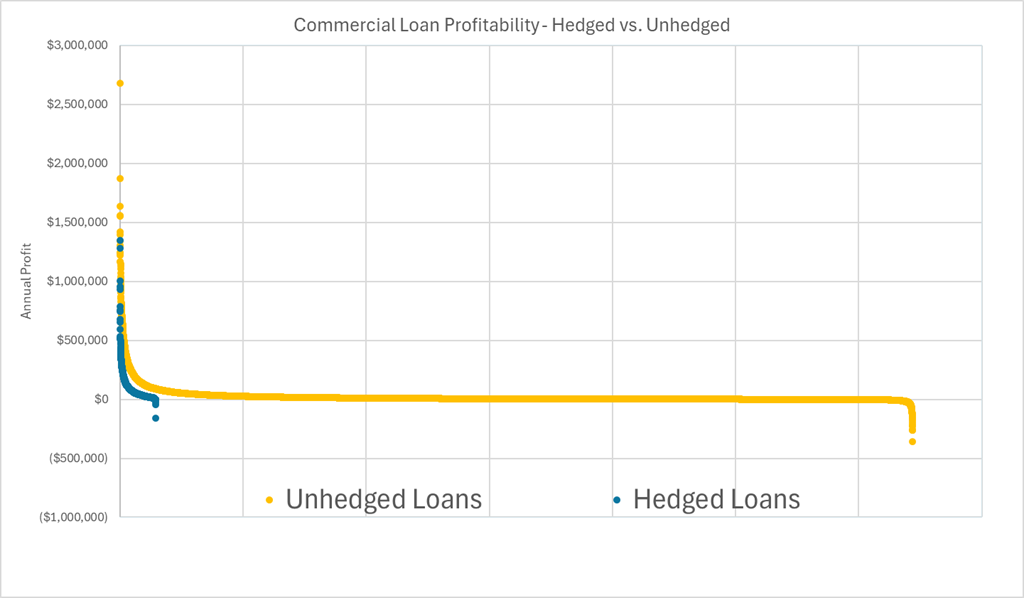

- The most important observation is that hedged loans are less likely to demonstrate negative-profits. Measuring the number of negative-profit by number of loans, principal outstanding, or sum of negative profitability, we conclude that hedging is not merely a growth tool, but a risk management mechanism for relationship economics. Only 16 out of 1,524 hedged loans demonstrated negative profits (1.0% of principal), versus 4,032 unhedged loans generating negative profits (18.6% of principal). The graph below shows the distribution of hedged vs. unhedged loans and annual contribution to profit.

The largest drag on banks’ performance is the amount of capital allocated to unprofitable loans/relationships. Principal committed or outstanding to unprofitable clients represents poor use of a bank’s capital. For this bank, $52mm in hedged loans were unprofitable versus $5.2Bn in unhedged loans. The hedged loans subtracted $252k in annual profit from the bank, but the unhedged loans subtracted $23mm in profit.

Why are so many of the unhedged loans so unprofitable for this bank? There are four main culprits:

- Many of the unhedged and unprofitable loans are fixed-rate loans priced in a lower interest rate environment. These loans are now unprofitable because of the bank’s higher COF as the result of an upward shift in the yield curve.

- Hedged loans demonstrate larger balances.

- Hedged loans are correlated with greater treasury and deposit engagement.

- Most importantly, clients willing to participate in loan hedging are committing to long-term partnership with this bank as evidenced by historical average life. This is likely to create relationship vs. transaction accounts.

At some community banks adoption of loan hedging is low. We see common barriers to loan hedging as lenders discomfort with explaining hedging (especially the prepayment provision), the misconception that hedging complicates deals, lack of internal alignment between credit, treasury and lenders, and short-term focus on deal closing over long-term economics. However, many community banks are reaching similar conclusions to our analysis: clients that adopt loan hedging are larger accounts, more profitable, more stable, and more engaged with the bank. Therefore, the opportunity cost of not promoting loan hedging can be substantial.

Conclusion

Our current analysis should be of interest to all community bankers. Commercial loan hedging demonstrates a broader truth about commercial banking: profitability depends less on volume and more on risk-adjusted stability. By protecting margins, improving pricing discipline, and reducing negative-profit exposure, hedging may play a pivotal role in sustainable commercial banking profitability. But we believe that banks should view commercial loan hedging not as a niche or defensive product but as a core structural tool that may reduce reduce earnings volatility, improve client-level returns, and build healthier, longer-lasting relationships.