7 Reasons To Focus More on Hedge Fee Income

Many community banks are searching for ways to increase fee income, and many bank CEOs have concluded that fee income is a significant driver of revenue and profitability. We argue that larger banks do not have an inherent advantage over community banks in generating fee income because of their scale. Most fee income generated by larger banks is not related to investment banking, wealth management, cryptocurrency, or Fintech. The majority of fees generated by larger banks is related to deposit and loans – business lines that community banks already maintain. Community banks do not need to buy new businesses to increase fee income; instead, we think they have to analyze where additional fee income possibility exists, focus on customer acquisition that generates additional fee income, and structure loans to take advantage of substantial hedge fee potential in today’s market.

Industry Comparison For Fee Income

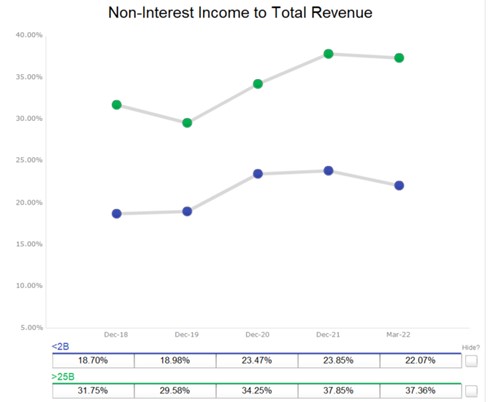

Larger banks have historically generated thinner NIM but higher fee income. The graph below compares fee income (non-interest income) to total revenue from 2018 to Q1’22 for banks over $25B (81 largest banks) and banks under $2B (4k community banks). On average, the national banks generate about 70% more fee income as a percentage of total revenue.

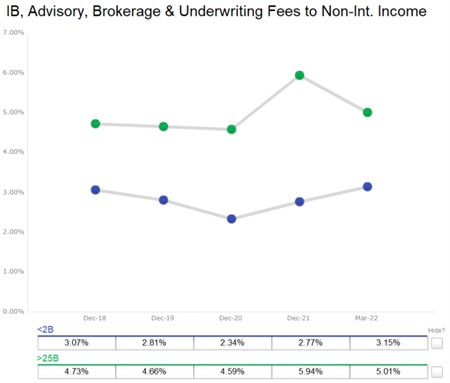

However, the larger banks generate a small fraction of fee income from business lines that community banks do not maintain. The graph below compares fee income from investment banking, advisory, brokerage, and underwriting to total fee income for the same two bank groups. Larger banks generate less than 2% more of total fee income than community banks from these lines of business (an insignificant difference).

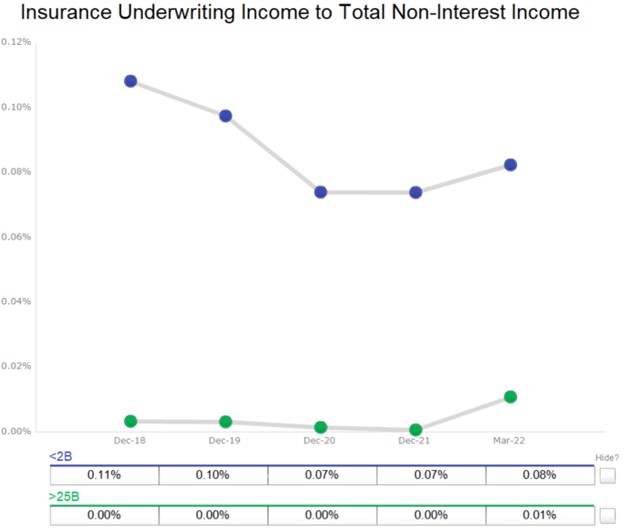

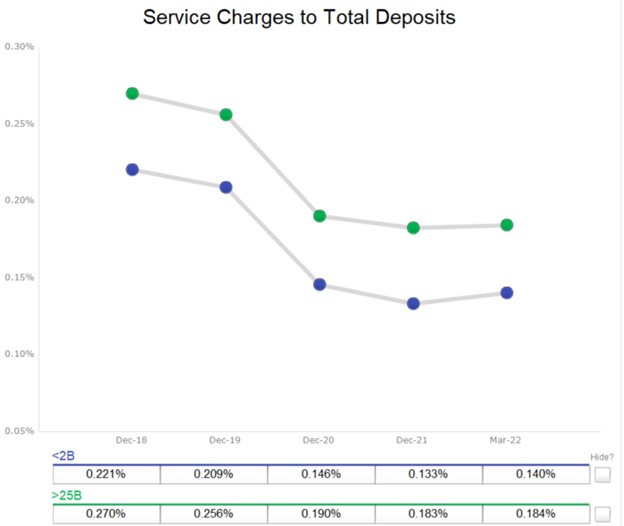

Community banks generate more of their fee income (proportionally) from insurance and almost the same amount of fee income from deposits (only a few bps difference on the percentage of deposit base), as shown in the two graphs below.

We also looked at fee income from investment in Fintech, securitization, and other sources, and none of these business lines showed significant divergence in fee income. In fact, surprisingly, smaller banks generate more fee income (proportionately) from investment in Fintech than the larger banks.

It appears that most of the fee income difference stems from loan fees, and we believe that the majority of that difference stems from hedging programs. For example, 40% of JP Morgan’s commercial banking revenue is derived from fee income, and JP Morgan’s commercial banking division is composed of middle-market and CRE lending (standard community bank offerings). We deduce that JP Morgan is driving this fee revenue from loan hedging and foreign exchange services to domestic middle-market and CRE clients.

Loan Hedging Fee Income For Community Banks

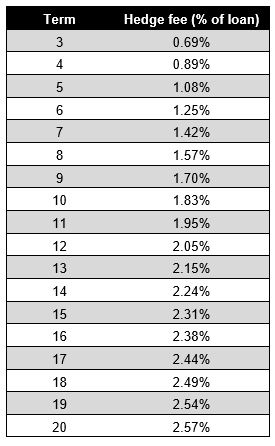

Hedge fee income on commercial loans is compelling because it magnifies the value of the fee over the life of the loan. The hedge fee is the cumulative sum of a spread on a loan and is paid in a lump sum and may be recognized by the bank upfront. The hedge fee can vary from 50bps to about 3% of the loan amount, depending on the term, amortization, and market competition. The table below shows loan terms in the first column and the corresponding hedge fee as a percentage of the loan that community banks can generate in the second column.

However, the fee numbers above understate the benefit of hedge fee income to community banks for the following seven reasons:

- Hedge fee income can be an important substitution for community banks for an industry-wide move to eliminating service charges on deposits and the end of PPP loans.

- When loans prepay, the loan margin goes away and must be replaced with new earning assets. However, the fee income is retained by the bank regardless of if or when the loan prepays.

- Loan prepayments increase the value of fee income. If a community bank can replace the loan with another loan and another hedge fee, the fee income becomes magnified over a constant-sized loan book.

- Each time a loan is upsized, extended, or otherwise modified provides an opportunity for banks to generate additional hedge fee income. This creates a steady stream of potential new fee income without the substantial cost of new business acquisition.

- In higher interest rate environments, upfront income is more valuable than future sources of income (loan coupons). Hedge fee income becomes even more profitable for banks.

- When inflation is higher than current interest rates (as is currently the case), hedge fee income is more beneficial to lenders. Hedge fees are discounted at the term rate, whereas future NIM will be discounted as received, and interest rates in the future are expected to rise to the level of inflation.

- In a rising interest rate environment, loan hedging becomes more meaningful as banks’ cost of funds increases and borrowers want to lock loan rates for as long as possible. The applicability and acceptance of loan level hedging to both lenders and borrowers creates ample opportunity to drive additional fee income.

Conclusion

The majority of community banks already possess products and customers that can allow them to generate substantial fee income. Today’s high inflation, and rising interest rates, create an opportune time for many community banks to develop hedge fees on their commercial loans.