Setting Commercial Loan Rates – Part II

In our previous article (HERE) we discussed differences between how various banks price commercial loans. When it comes to setting commercial loan rates, we contrasted “ideal” and real-world pricing strategies employed by banks. We highlighted the objectives of loan pricing and summarized seven tools that community banks can use to price commercial loan relationships. In this article, we would like to further discuss threshold pricing (minimum yield) and how this method may erode bank performance.

Setting Commercial Loan Rates – Discipline and Threshold Pricing

We estimate that over 75% of community banks impose some form of thresholds pricing (minimum NIM, asset yield or credit spread). Unfortunately, subjecting loans to threshold pricing regardless of size, term, cross-sell opportunities, lifetime value, and credit quality leads to misallocation of capital and substandard ROA/ROE. However, the strategy of threshold pricing leads to the following additional unintended consequences:

- Despite management’s best efforts, lenders interpret the minimum spread as a race to the bottom because their customers are top quality. The starting point that is meant to be a floor (the minimum credit spread) inadvertently becomes the pricing ceiling. In the long term, this strategy may decrease the average credit spread at the bank instead of increasing it.

- There are three ways that managers can price their loans (or any product or service, for that matter):

-

- Price to the competition. Banks determine where competitors charge for similar loans in the marketplace and price accordingly.

- Cost-plus pricing. Here, banks calculate their cost of capital, funding costs, and all direct and indirect costs and add a margin to determine the price.

- Perceived value to the customer. While more subjective, the bank determines the maximum a borrower will pay for the perceived value of the banker’s expertise and the problem the bank is solving. This is the optimal way for banks to price their loans to increase ROE.

But when banks institute a minimum credit spread, that minimum spread is typically based on what the competition is pricing (or above if the bank wants to minimize loan growth). Managers look at the average spreads in the market and set their minimum spread relative to that industry average. However, pricing to the competition is the worst pricing choice for banks. Pricing to the competition is an abdication of management’s duties because it effectively transfers important corporate power to the competition. While bankers should be aware of the prevailing pricing in their market, that information is used correctly to make a buy-or-sell decision (make a loan or buy a security), not to match or follow the competition. The above is true in most industries, but in banking, pricing to the competition is even more derelict because the decision is not just about revenue but also the extension of credit. The better way for banks to price loans is based on perceived value to the customer, and minimum credit spreads force bankers away from that pricing principle.

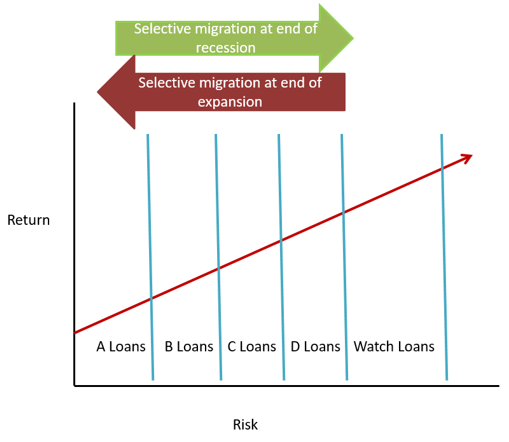

- To optimize loan portfolio profitability, community banks must recognize how to migrate through the credit spectrum (see an example of the concept in the graph below). During extended periods of expansion, banks misprice credit risk more severely. In a recession, better credit-quality loans have a higher risk-adjusted ROE. Banks want to capture better credit-quality loans when the economy is expected to slow and liquidity to decrease. Banks can avoid negative selection bias by selecting the correct credit quality in anticipation of the change in the economy. For example, suppose a bank is not anticipating changing economic conditions and generates credit quality across the spectrum in a downturn. In that case, the competition will scramble to steal high-credit quality loans and avoid the lower credit quality loans, naturally decreasing the average credit quality of the portfolio for that bank. A minimum credit spread strategy is inherently set up to capture lower credit quality credits because management typically sets the minimum spread to capture more yield, not to funnel high credit quality at a lower yield.

- The minimum credit spread strategy magnifies survivorship bias in banking. Survivorship bias is the logical error of concentrating on outcomes that made it past some selection process and overlooking outcomes that do not make the selection process. The issue for many banks is this: the performance of all loans should be measured over the life of those credits, but most banks only measure performance quarterly on financial statements looking backward. However, the profitability of an individual loan going into the portfolio is not measured at inception because minimum credit spreads are not a measure of profitability, and minimum credit spread has no actual causal relationship to profitability.

Survivorship bias occurs at banks using minimum credit spread because the more profitable loans (the ones with the lower credit spread and better credit quality) are heavily underrepresented in that bank’s portfolio. Managers are then challenged to increase the bank’s ROE and choose loans with an even higher yield but, unfortunately, lower collective ROE. The profitable/lower-risk loans are not even vetted by management because lenders follow minimum credit spread guidelines.

Example Loan Scenarios

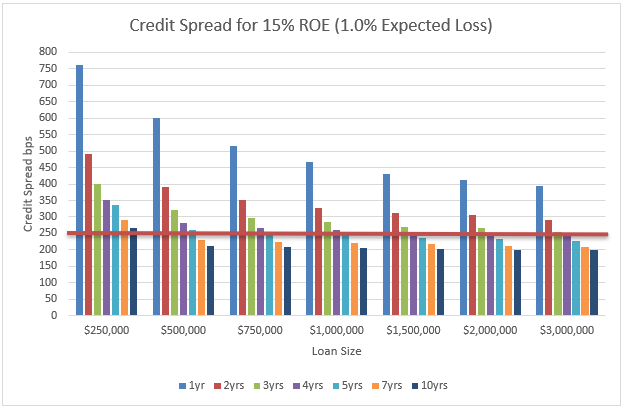

The below graph shows credit spreads on the left axis required to achieve 15% RAROC with 1.0% expected credit loss (average loan quality) and varying loan size and loan terms. The red line represents threshold pricing of 2.50% credit spread.

When banks are setting commercial loan rates, a bank that imposes a 2.50% threshold credit spread, is de facto favoring smaller credits and shorter-term loans (consider the X axis). The vertical distance between the threshold price of 2.50% and the various bars in the graph (representing the credit spread needed to achieve a minimum 15% RAROC) measure the suboptimal return for the bank. Essentially, this bank would prioritize smaller and shorter credits at the expense of more lucrative, larger, and longer relationships.

Conclusion

We advocate that all community banks should allocate capital based on highest return – this should apply to individual loans, clients, business lines, geographies and branches. To allocate capital appropriately, management first needs to understand the achievable RAROC from available various product sources. When setting commercial loan rates, pricing discipline requires the ability to assess and forecast credit quality, credit usage, relationship cross-selling, and lifetime value of the customer. Unfortunately, threshold pricing may be counterproductive to this goal.