The Best Method for Pricing Commercial Loans

In a perfect world, when it comes to pricing commercial loans, banks would price customer relationships based on risk-adjusted return on capital (RAROC) and incorporate shareholder value-added (SVA). Banks would then measure profitability at the customer, product, branch, region, or manager level so that management may properly allocate resources to drive institutional profitability. Banks would create customer lifetime value ranking, and direct service at the relationship, product, branch, or manager that holds the highest potential return for the bank. But in the real-world banks price customer relationships very differently, and in this article, we will discuss the approaches we see and define the pros and cons of each.

Objectives When Pricing Commercial Loans

Most national banks use a RAROC pricing model, fund transfer pricing, and SVA measures. We estimate that about 50% of regional banks use some version of a RAROC loan pricing model. But only about 15-20% of community banks (banks under $10Bn in assets) are using a RAROC model. The national and regional banks originate about 85% of all domestic loans, and community banks hold the remainder; therefore, how national and regional banks price commercial relationships permeates the industry. Why should banks measure profitability of their relationships? The most common reasons are as follows:

- Increase granularity of credit pricing,

- Accurately allocate capital,

- Maintain lender discipline to minimize cover bid,

- Educate management and lenders,

- Become more attuned to prevailing market conditions,

- Standardize pricing across divisions, product lines, and relationships,

- Increase profitability,

- Decrease risk,

- Manage customer relationships, and

- Enhance reporting, control, and governance.

Pricing commercial loans or relationships is not intuitive and for most community banks only 10% of customers account for 120% of profits, and the remaining 90% of the customers subtract profitability from the bank. Furthermore, the cross-sell profitability for a commercial relationship may be much more profitable than the commercial mortgage – acceptable loan profiability may be 15-25% RAROC, but deposit and fee business RAROC may be multiple times higher.

How to Measure Relationship Profitability

Many community banks struggle to segment their customers based on relationship profitability. One hurdle is that many community banks do not use the tools to measure profitability at the relationship, product, branch, region, or relationship manager level. However, banks can develop their own tools or purchase pricing models from third-party vendors. Below is list showing how community banks currently price their commercial loans ranked from the most basic to complex.

Price to Competition

Banks match their competitors’ pricing regardless of risk and business alignment. This is the most basic pricing tactic and is the default strategy for many banks. The issue is that the bank is taking a competitor’s view of asset quality, cross-sell opportunity, and relationship return that may not be valid for that bank or the current environment.

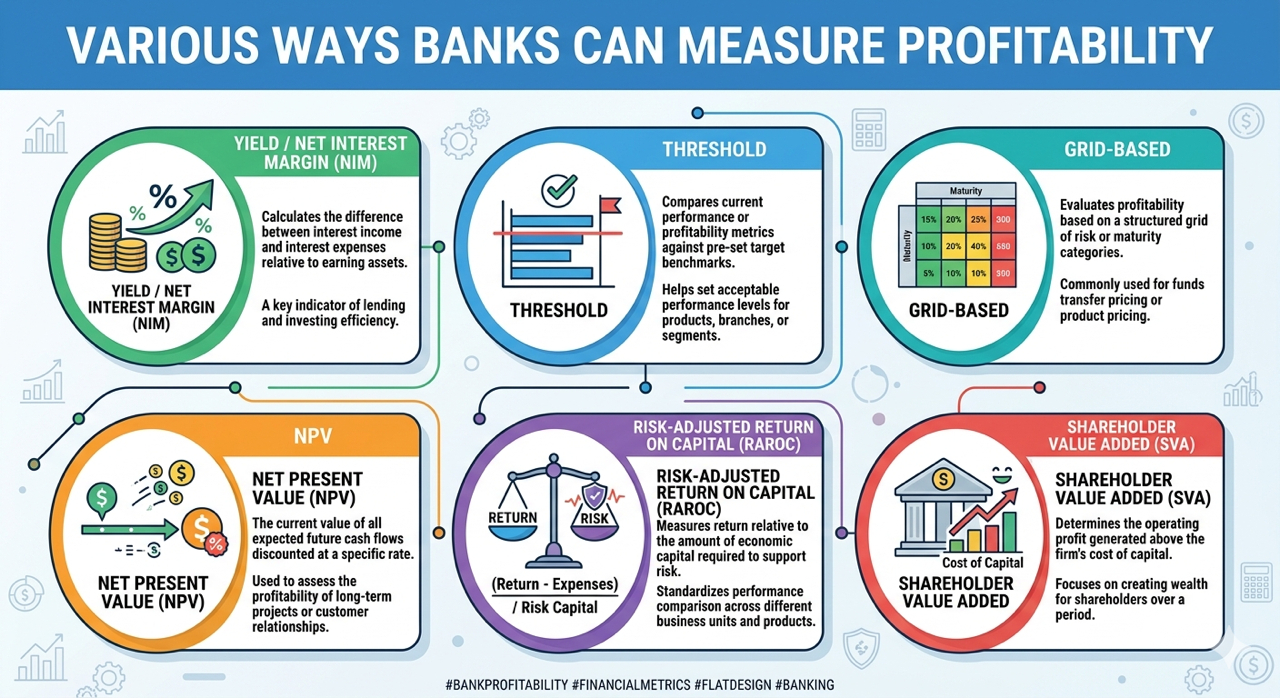

Yield – NIM

Banks measure apparent revenue or margin, without considering variability around revenue, risks, or costs. This is a rudimentary pricing method and results in poor bank performance over credit cycles and leads banks to make suboptimal pricing decisions.

Threshold Pricing

Banks create thresholds (minimum NIM or credit spread). This is a simplistic view of relationship pricing because it does not consider enough inputs, it also does not measure dynamic changes in the market, and this method does not measure cross-sell opportunity, lifetime value of the relationship, and optionality of prepayments. We will publish a further article delving deeper into the mechanics of this pricing method.

Grid-based Pricing

Pricing grids are a prelude to RAROC pricing, but they lack the myriads of inputs that distinguish sources of risk, acquisition and maintenance costs, fees, interest rate and credit risk, and cross-sell opportunities (some of the most important drivers of banking profitability). However, they present a straightforward way for community bankers to have pricing discussions with prospects instead of chasing competition to the lowest priced offer.

Net Present Value Calculation

Banks measure the net present value of cash flow, incorporating revenue, costs, and cross-sell value. Banks can build their own NPV models or purchase ready-made models from vendors. While this pricing method considers revenue and costs, it does not dynamically measure capital deployed (risk-based or economic capital), prepayment speeds, optionality, or economic return to the bank. However, this method forces banks to adopt fund transfer pricing for better return measures.

RAROC Model

Banks measure risk-based or economic capital, prepayment speeds, optionality, and total relationship return. Very few banks have the resources to build such a model in-house, but many vendors offer such models at low costs (we offer a free version of this model to community banks). The drawback of this model is that it does not calculate SVA and does not allow management to make customer lifetime value ranking (CLVR).

SVA Calculation

SVA is the measure of a bank’s net operating profit after tax for each client over the bank’s cost of capital for that client. For example, two customers may both show a 15% ROROC for the bank, but customer A has $1mm in loans and $1mm in deposits, while customer B has $5mm in loans and $5mm in deposits. While both customers have the same ROE, customer B has five times the SVA compared to customer A.

Using the SVA methodology, each customer is ranked from highest to lowest in profitability. Banks can then allocate resources based on highest SVA – also known as customer lifetime value relationship segmentation. National banks use this pricing method, but the few largest banks that utilize this method control the majority of loans in the industry.

Conclusion

We feel that all community banks should allocate capital based on highest return and this philosophy applies to individual loans, clients, business lines, geographies and branches. To allocate capital appropriately, management first needs to understand the achievable RAROC from various products. Community banks can develop or easily purchase models to price relationships and segment customers based on customer lifetime value ranking. Our free version of the Loan Command model (HERE) allows community banks to measure profitability nearly as robustly as the national banks do.