Why Expected Average Loan Life Matters to Value

Expected average loan life measures the amount of time that principal is outstanding on a loan. This average life is driven by many factors, including amortization period, economic circumstances, nature of the loan and the expectations of the borrower, and most importantly, by contractual term and prepayment provisions. The biggest surprise for many lenders is how shorter average loan life affects the profitability of a loan portfolio. We modeled various $100mm loan portfolios and calculated the net present value (NPV) of income over a 10-year period. The results are surprising and should be considered by every community bank executive.

Our Loan Life Analysis

First, we want to establish a common finding in commercial loan lending. Almost all commercial loans are originated at a cost to a bank that exceeds the sum of borrower fees. Most banks’ origination costs (marketing, underwriting, documentation, and funding) are higher than the fees charged at origination. That means that the value of the loan is below par at inception. The issue is further amplified by smaller commercial loans (those under $1-2mm in size).

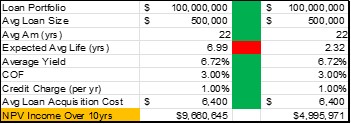

We developed a model that calculates the NPV of income for commercial loans based on expected average life of a $100mm loan portfolio over a ten-year period. Our model allows us to change various parameters of a commercial loan such as loan amount, amortization, loan yield, COF, upfront fees, annual maintenance costs, credit charge, and origination costs. We then make different assumptions on average expected life of individual loans in the portfolio and measure the NPV of income over a ten-year period. The outputs for one such scenario appear in the table below.

The results show two identical $100mm loan portfolios (same average loan size, amortization period, rate, cost of funds, credit costs, and acquisition costs), except that one portfolio’s expected average loan life is almost 7 years, and the other is 2.32 years. The NPV of income for the longer average loan life portfolio is 93% higher than the same portfolio comprised of shorter loans. The results are astonishing. The difference between the two portfolios is that the longer life portfolio is comprised of mostly 7, 10, and 15-year loans with strong prepayment protection, while the shorter loan portfolio is comprised of 2, 3 and 4-year loans with weak prepayment protection.

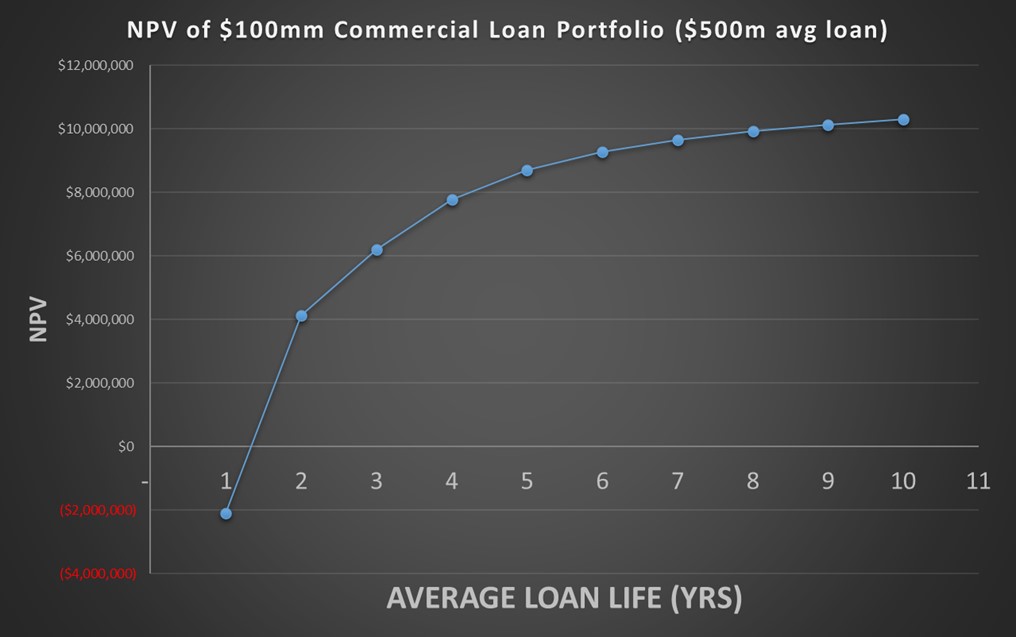

We then ran the model and plotted the NPV of income for the $100mm portfolio, $500k average loan size, for various average expected lives. The graph appears below. It shows that as the expected life of the loans in the portfolio shorten, the NPV of income decreases, and vice versa. The NPV of income dips below zero with 1-year average expected loan life.

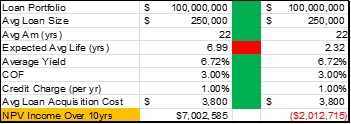

We wish to point out that the average community bank’s commercial loan is approximately $250k to $600k in size, depending on the bank and product mix. Therefore, we feel that using an average loan size of $500k is the correct example for our analysis. However, informative analysis was also gleaned when we decreased the average loan size of the $100mm commercial loan portfolio and ran the same calculations. Below is output assuming an average loan size of $250k. The NPV of income for the shorter, and smaller, average loan is negative over a ten-year period.

Key Takeaways

Expected life of a commercial loan is a major driver of profitability. Commercial loans have thin profit margins after accounting for ongoing costs such as COF, credit charges, and loan maintenance costs, but most importantly, commercial loans have high upfront origination costs. This behavior is especially pertinent for smaller credits – those below $1-2mm in size.

Some bankers argue that their overhead costs are fixed, and that the lending, credit, portfolio management, and loan operation staff is available to replace loan runoff. However, this argument is faulty, because all costs are variable in the long-run, and the strategic analysis by management must be based on the long-term business model of the bank. If the argument is “why not make these shorter loans, since I have the overhead costs regardless”, then the long-term outcome for the bank’s business model is not viable. Banks lower their efficiency ratio primarily through scale at the front line, not at the corporate level. Longer loan average lives reduces replacement costs of earning assets, increases assets per employee, drives efficiency ratio lower, and increases long-run ROE potential of the bank.

We believe that there are a few actionable items for community banks stemming from our research. How do community banks position their marketing, product mix, and sales force to extend average expected loan life? Even sophisticated loan pricing models do not adequately track, predict, or measure expected loan life, and bankers are left to their intuition to try to maximize profits. In future articles we will outline what actions community banks can take to increase average loan life, and build more stable, and more profitable loan portfolios.