Preparing Your Bank For A Divided Congress

We might have a divided Congress. Pundits, economists, and the market provide economic forecasts such as GDP, interest rates, inflation, consumer and business demand, loan default rates and banks’ cost of funds. Unfortunately, people overestimate their competence even in areas where they possess experience and knowledge. Market forecasts represent the sum of all actors expressing their view of the future through actions that risk their resources. But markets are always in motion and predictions change rapidly. What was “certain” a few months ago is now obsolete. Further, time horizons do not match predictions – predicting the next three months is hard, but predicting the next three to 20 years is close to impossible.

However, there are some overwhelming indications in the market that are worth noting and, in this article, we will discuss them and their possible impact on banking.

Prediction Markets and November 2026 Elections

Prediction markets are being viewed by financial world as a real-time barometer of political probability, and the signals heading into November 2026 are striking in their expected probabilities. Platforms like Polymarket and Kalshi are pricing in a significant probability of divided government after the midterms.

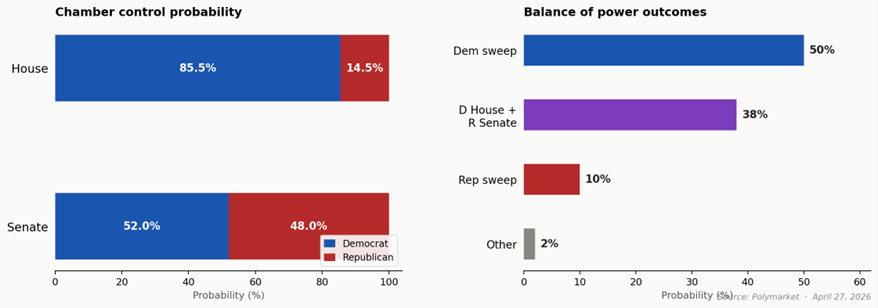

Predictive markets currently assign 85.5% probability that Democrats will reclaim the majority in the house. Republicans hold a razor-thin majority today, and the historical average loss for a president’s party sits at 28 House seats dating back to 1946. The President’s current approval rating is hovering below 40%. Recent Democratic wins in special elections and a wave of GOP retirements in battleground districts have only reinforced this consensus.

The Senate picture is far tighter, and markets imply a 51-52% probability of Democrats capturing the Senate. Prediction markets see a 38% probability of a split outcome – specifically a Democratic House paired with a Republican Senate – and a 50% probability of a full Democratic sweep of Congress. The graph below summarizes the current odds of chamber control.

Divided Congress and the Economy

For investors, business owners, and bankers, the prospect of a split government should not be a cause for alarm – in fact, history suggests it may be something closer to a relief valve. When legislative gridlock prevents large fiscal swings in either direction, economic volatility tends to decline. The Clinton-Gingrich era from 1995 to 2001 is a good example: a Democrat in the White House, Republicans controlling Congress, and the longest peacetime economic expansion in American history. Expansion will be expected to continue – albeit slowly. The broader lesson is that divided government tends to suppress fiscal ambition. Large tax overhauls, sweeping new entitlement programs expansion or contraction, and major spending increases all become significantly harder to pass. This fiscal restraint generally keeps deficits from expanding dramatically, which can be stabilizing for bond markets and long-term interest rates.

Recession probability under a divided government is historically lower than under unified governments that pursue aggressive and sometimes destabilizing fiscal stimulus or contraction. A divided government is more likely to produce smaller changes to the deficit trajectory, which tends to reduce the boom-bust amplitude of economic cycles. For community banks focused on credit quality over a multi-year horizon, this is meaningful context: a split Congress reduces the probability of sharp fiscal shocks in either direction.

What About Interest Rates?

Perhaps the most consequential variable for community bank and borrower/depositor strategy over the next two years is that the Federal Reserve, and the path of monetary policy, is in the hands of a new chair. The former Fed Governor Kevin Warsh has been nominated to replace Jerome Powell as Chair, and Warsh faced Senate Banking Committee questioning in April 2026. Powell’s term as Chair expires in May, though he retains his governor seat for two additional years and it is likely that he will remain on the committee in this reduced capacity. This will create the unusual dynamic of a former Chair remaining on the FOMC as a governor.

Warsh is historically known as a hawk who dissented in favor of tighter policy during his previous stint on the Board from 2006 to 2011. He has recently argued that artificial intelligence-driven productivity gains will suppress inflation structurally. During his confirmation hearing, Warsh emphasized that “monetary policy independence is essential”.

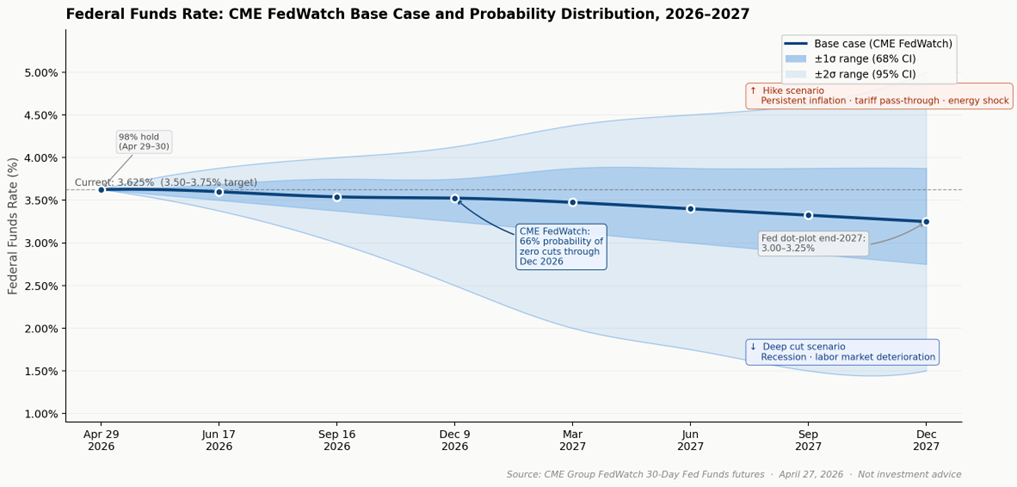

The market’s Fed Funds futures verdict is clear: traders currently price a 66% probability that the Fed makes zero more cuts through the end of 2026. The June 17 meeting is 97% certain to be a hold at 3.50–3.75%. March CPI surged to 3.3% annually – the highest reading since May 2024, driven by a 10.9% energy spike, while the unemployment rate edged to 4.3%. The Fed’s own March 2026 dot plot projects just one additional 25bp cut this year, and the market currently prices roughly a coin flip on whether that single cut materializes before year-end.

With Powell remaining on the FOMC as a governor, there is also a non-trivial probability of policy friction. Powell has consistently advocated a data-dependent, patient approach to cutting. That voice – held the most experienced member of the committee – may serve as a moderating influence on any pressure from the White House to accelerate cuts ahead of the 2026 elections.

The graph below shows the market’s current forecast for Fed Funds rate and one and two sigma distribution around the expected path of short-term rates.

How Community Banks Should Prepare For a Divided Congress

The prospect of divided government and consistent short-term interest rates carries specific, actionable implications for community bank balance sheet management, ALCO strategy, deposit pricing, and loan portfolio positioning.

Balance sheet and ALCO: Community banks should use the window ahead of the election to stress-test their investment portfolios against a “higher for longer” rate scenario. ALCO committees should model net interest margin sensitivity across multiple rate paths.

Deposit strategy: A divided Congress tends to produce a more cautious consumer and business environment. Businesses, especially small and mid-sized enterprises, may hold more liquidity than they would in a hotter economy. Community banks should lean into this behavioral tendency by deepening non-interest-bearing and operating account relationships. Core deposit retention becomes a strategic priority and certificate of deposit specials should be structured conservatively, avoiding locking in high costs across a long duration.

Loan portfolio positioning: A divided government historically slows both infrastructure stimulus and regulatory rollback – the two most common fiscal levers that drive C&I and commercial real estate lending cycles. Community banks should expect a softening in loan demand from sectors that benefited from unified Republican fiscal policy, particularly energy, defense supply chains, and government contracting. Conversely, consumer lending and small business credit may hold up well if the labor market remains resilient. Underwriting standards for commercial real estate deserve scrutiny: in a flat rate environment with slower growth, cap rate compression reverses, stressing LTV ratios on recent vintage loans. Stress testing CRE portfolios at cap rates 150–200 basis points higher than origination is prudent. Ensuring that most important relationships are sticky through correct pricing, enforceable prepayment provisions, and appropriate cross-sell of treasury management products is paramount.

Customer communication: Bankers should get ahead of the narrative with their business and agricultural customers. Uncertainty is the enemy of investment decisions. Proactive outreach explaining the balance sheet positioning of the bank, its approach to credit and its capacity to be a reliable lending partner builds the trust that translates into deposit stickiness and cross-sell opportunities when competitors are distracted.

Conclusion

The confluence of a likely divided Congress, historically moderate fiscal outcomes, and a Fed locked into a prolonged pause creates a specific operating environment for community banks: one of constrained margin expansion, sustained credit quality vigilance, and competitive deposit warfare. Institutions that use the next six to twelve months to fortify their funding base, stress-test their loan portfolios, and deepen customer relationships will be best positioned to navigate whatever political configuration November delivers. The prediction markets have spoken, and the era of unified-government policy acceleration is likely ending. Community banks that prepare accordingly for a divided Congress will be the beneficiaries.