Payment Products – 14 Ways Banks Will Make Money

In the future, banks will make money on payment products by DELAYING settlements. That vision is ironic considering financial institutions are spending billions of dollars moving payments from one to three-day settlement to real-time. However, in the next three years, many banks will have the bulk of their payments settling in real-time, and delaying payments will be the added value. This article delves into 14 products that banks have that will create more customer and franchise value.

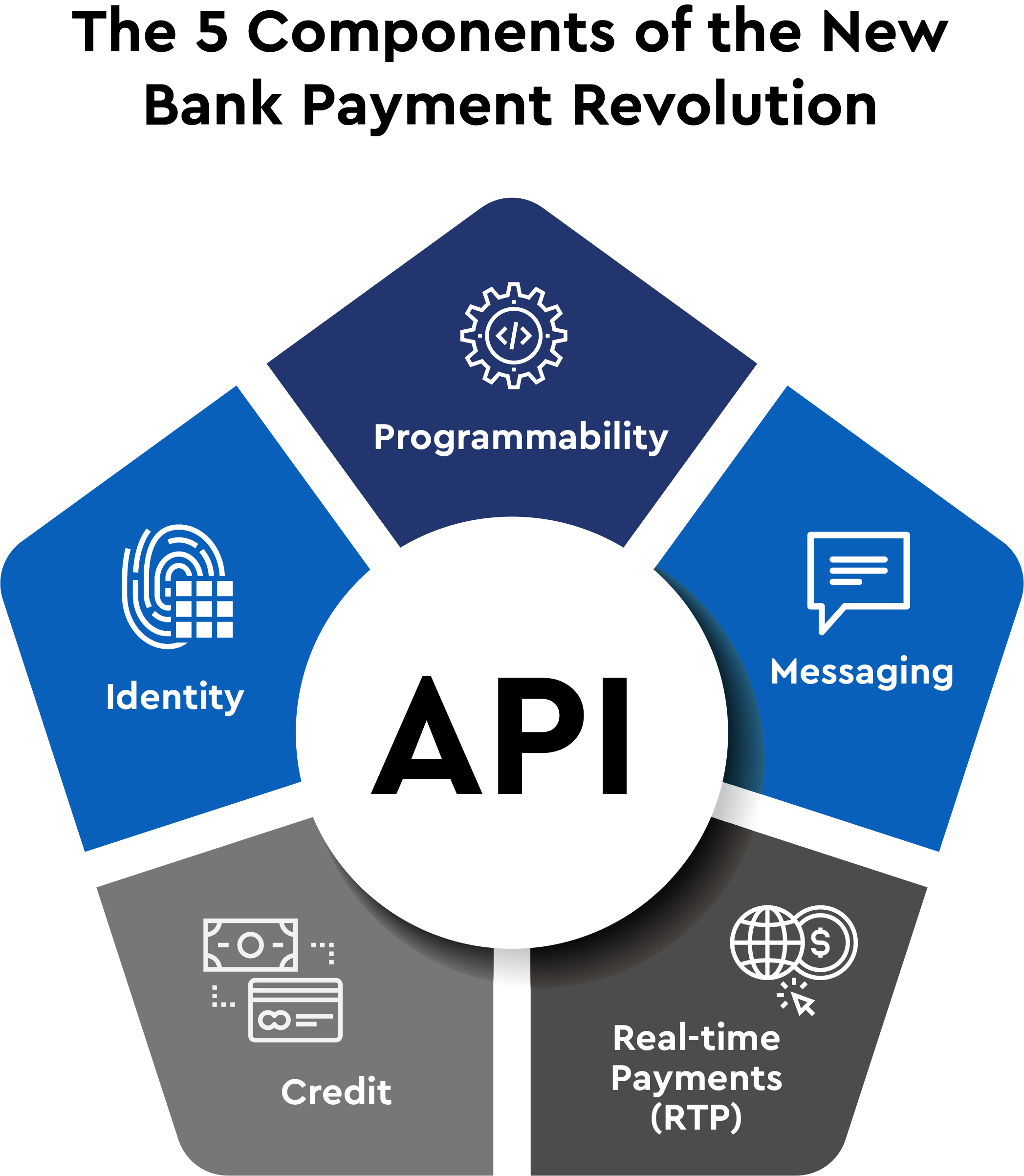

The Five Pillars of The Payment Product Revolution

Payment products are now in a rare confluence of trends that is a paradigm shift back to banking. These trends received more support this month when the President signed an Executive Order supporting the legal and equitable use of technology around a digital currency and digital assets (HERE). By way of background, we gave bankers a primer on how to work with defi and blockchains a while back (HERE). As we pointed out, banks are in an ideal position to take advantage of these trends and grab market share back from the traditional card networks and fintechs. By combining these trends, banks will be able to create an endless supply of specialty payment products that will be able to generate fees and/or float balances.

Real-time Payments (RTP): Either using The Clearing House, FedNow, or the crypto rails, all banks will need to clear payment transactions in real-time in the next three years. It will become a minimum expectation for both consumers and businesses, like how the ATM and remote deposit capture evolved. It will be hard to compete for payments and transactional accounts if you don’t have RTP. By clearing in real-time, banks will not only be able to appear to provide real-time settlement but clear and process the payment in real-time, thereby providing confirmation and eliminating credit risk.

Expanded Messaging: The Clearing House and FedNow will allow an extended amount of data to be transferred with the payment, while the crypto rails will have an unlimited amount of space. Expanded messaging will be able to hold billing information, invoices, and metadata (data about the transaction). These additional messaging capabilities will make the new payment channels superior to the current card, wire, and ACH payment rails that dominate today.

Programmability: To create “smart” money or a smart contract to transfer value is an epochal event. Instead of making a platform where we program a set of procedures to transfer money, now the money itself can be programmed and customized to deliver laser-like value without human intervention.

Instant Credit: As the buy-now-pay-later trend moves from innovation to maturity, banks are now starting to harness this technology and extend credit instantaneously within the payment process. Given our funding base and ability to apply leverage, banks can now incorporate credit into various products and be hyper-competitive with fintechs.

Identity: We now have the technology to instantly know who the right person is to send/receive payment to, but we also know if that right person is on the other end of the payment process with a high degree of certainty. By using a culmination of third-party validated data, biometrics, device information, and behavioral data, we now have all the tools in place, for the first time in history, to have a better than a 98% probability of delivering a payment successfully as intended.

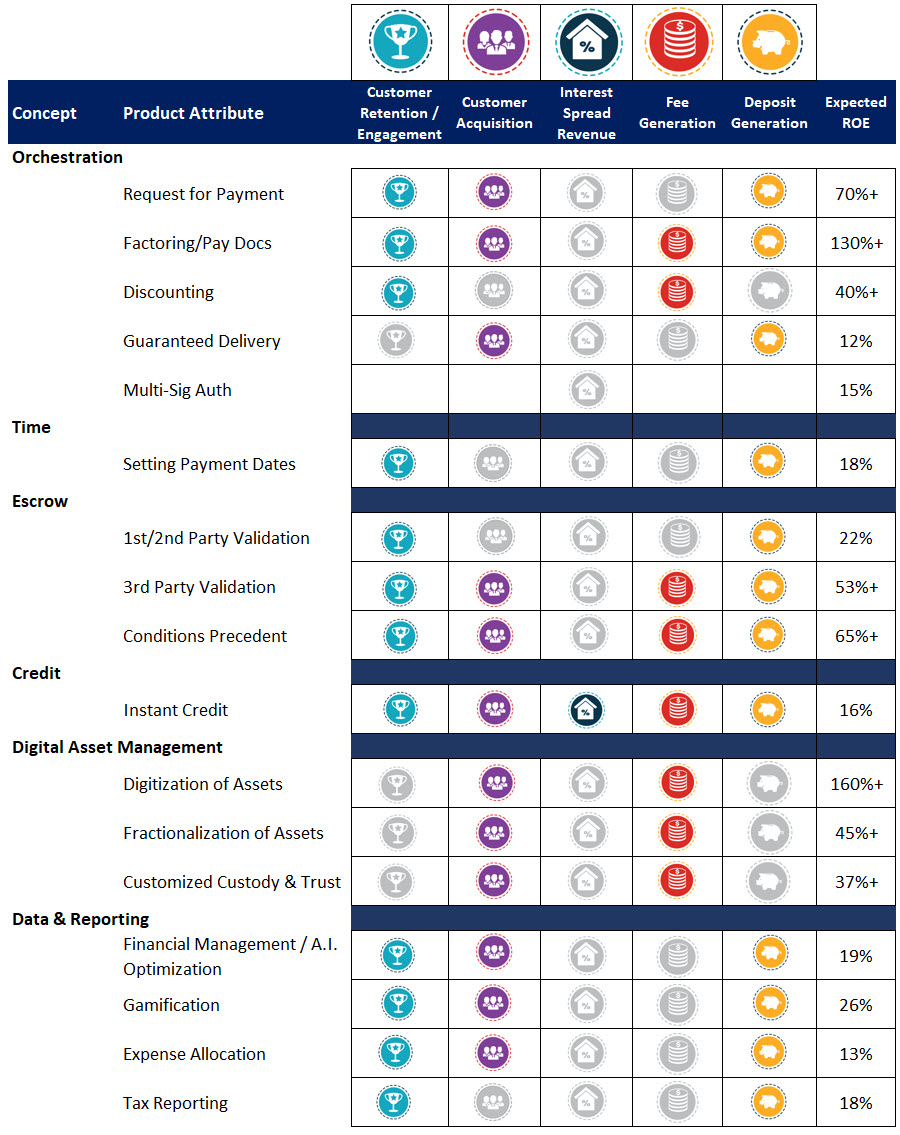

Combining The 5 Components into Payment Products Along 6 Dimensions Covering 14 Product Attributes

- Customized Payment Orchestration

In our banking history, payments have been a single event – Party A sends a payment to Party B. With the advent of programable money and RTP basics, payment can now be rendered to include several linear or simultaneous steps. Many elements of the new payment revolution are already a reality.

- Request for Payment – Businesses can now issue a “Request for Payment,” or RFP. Here a utility, municipality, or other organization can send a message and request payment with the workflow already embedded or closely linked to the message. Similar to P2P, this B2B or B2C application allows less friction to notice and collect payments.

- Factoring/Payment Documentation – Monetize an outstanding invoice to speed up cash flow, and the payment workflow will automatically update the beneficiary’s information. Similarly, contact information for any payment can be validated, approved, and updated on the payment chain while the payment is in the process of being settled. This payment product has one of the highest risk-adjusted returns since allowing for more efficient ownership of receivables and allowing near-frictionless transfer of an existing business line will face quick adoption, increase liquidity and decrease risk.

- Discounting – A payment period and discount can now be incorporated and programmed in real-time. If a business needs cash flow, it can immediately offer a discount for payment for all outstanding invoices. In a similar vein, companies can also send payment messages to handle prepaid services in exchange for a discount to the customer.

- Guaranteed Delivery/Fraud-as-a-Service – A little-discussed fact in banking is that about 3% to 4% of payments fail to reach their desired recipient. Banks are now in a position to outsource their identity verification and authentication as well as their fraud, AML, and KYC capabilities. This can allow banks to guarantee delivery in near-real-time as the payment is occurring. In some cases, 100% verification may slow down the payment process and take more time. However, the ability to create a separate, parallel workflow and be able to handle this is the evolutionary concept here.

- Multi-Sig Authorization – Now, instead of a contract and payment being separate events, they can be combined. Banks now can require multiple validated digital signature approvals, in a specified order, on payments to allow the release of value.

2. Shifting the Timing of Payments

- Setting Payment Dates- While billing applications can set a specific payment date, there will soon be a new level of customization that can now take place. Customers will be able to set alerts and reminders if certain events occur. This could be as simple as asking if a monthly payment should be made to your housekeeper and then verifying the amount or as complex as making a series of payments over time to different parties.

3. Escrow – Conditions Precedent

Digital payments will reach a new level of sophistication by being able to inject a set of business rules or conditions precedent to the release of payment value.

- First/Second-party Validation – In the simplest form, some payments may require a higher level of digital acceptance, such as an agreement on a digital contract’s terms and conditions. These can be embedded in the payment stream so the buyer or seller can record their authorization and/or acceptance. This product can be used for any simple sales or agreement and will reduce friction by combining the terms and payment into one object.

- Third-party Validation – Similar to multi-sig authorization, third parties can perform certain services within the payment workflow. Smart contracts already automate the checking of clean title, the presence of insurance, a person’s criminal history, or if a certain credit score is met. More third parties will be coming online every day to help validate transactions via an API or digital connection. Sell a product or service (like an event ticket), and the smart contract will automatically reach out to the creator of the event or manufacturer to validate the authenticity of the ticket or product.

- Other Conditions Precedent – There are many specialty payments that banks will be able to customize for individuals and businesses. Individuals, for example, can set and make automatic payments to their mortgage (like an additional loan paydown) or non-profit charitable donations if certain balances are achieved by a specific day. Other payments can be made should certain events happen, such as weather (think insurance), sales production, or other quantifiable action.

4. Instant Credit

Say what you will about buy-now-pay-later (BNPL) as an asset class, but the technology and methodology are critical for incorporation into the payment workflow to grant instant credit. In the past, credit was static. Banks underwrote credit and largely held an amount they would lend a consumer or business fixed until the next review – usually for a year. Now, using a foundation of transaction data and aggregated account data, credit can be dynamic and change day-to-day. This aspect is critical for not only controlling credit exposure but leveraging credit as a product attribute similar to how BNPL has become so popular. As evidence of BNPL technology’s importance, Apple, Visa, and Mastercard have all purchased BNPL companies primarily for their technology.

While RTP eliminates the need to credit, credit will still be required for some transactions, and banks are in the perfect position to provide it while still protecting the borrower. Instead of having various fintechs provide credit through the merchant, banks will be able to incorporate credit into their banking-as-a-service functions.

In this manner, payment products and credit can go together, and more banks can participate, should they choose, in what was formally the sole domain of credit card banks. Instead of just being able to survive off interchange fees, banks can now get back into the consumer and small business lending game. If these banks choose not to participate, credit can be quickly enabled by any number of providers connected to the payment workflow.

Improving on today’s BNPL structure, banks can help manage debt repayment by analyzing a customer’s cash flow and adjusting payment accordingly through analytics to present the lowest cost to the borrower and the lowest credit risk to the bank.

5. Digital Assets

At present, few assets are digital, and those assets that are digital, like an NFT, are usually outside the realm of the banking industry. Within the next year, look for banks to play a role in the digitization and custody of both digital and physical assets as the payment flow is the ideal place to capture those assets and add value. Banks will create payment products that monitor transactions and allow the easy creation of digital assets.

- Digitization of Assets –Purchase a good or service, and your bank will ask you if you want to turn it into a digital asset and make the purchase part of the public record like a Uniform Commercial Code (UCC) filing. Digitizing the asset will be automatically validated since the transaction included the receipt details and the confirmed transfer of value. Banks will be able to provide this service both to customers and as a banking-as-a-service application to their merchants as a white-label solution to their customers. The programable nature of the payment stream will be able to handle specific business rules and workflow support for different types of customers to allow for both cloud storage and cold storage (off-network or air-gapped). Banks will be able to store, report and assist in the maintenance records of these digital assets. Assets will gain a new level of liquidity, all facilitated by a trusted bank. This payment product will be fantastic for customer acquisition and will generate fee income on very little risk thereby resulting in a high return on investment.

- Fractionalized Assets – With the digitization of assets, the natural evolution is the fractionalization of assets. It has been historically impossible, or at least inefficient, to divide up fractional ownership in most asset classes like real estate, art, or collectibles, to name a few. Banks can now create payment products around the buying and selling of fractionalized assets that customers own.

- Customized Custody & Trust – Of course, once the assets are digitized, banks will be in a natural position to provide custodial services for these assets. The innovation here will be that banks will be able to provide a level of automation and customization not previously seen. Update your name or address, and a bank’s third-party report will alert your bank, automatically confirm with the proper authorities on the account, and then update the trust or fiduciary agreement. Depending on the circumstances, the jurisdiction of the digital assets can be changed to suit the needs of the trust or involved parties. This product will be handy for corporations, insurance companies, family offices, foundations, endowments, foundations, municipalities, and public funds.

6. Data and Reporting

The expanded capabilities of the payment’s message will develop the ability to analyze, suggest, report, and quantify a customer’s transactions. Personal Financial Management (PFM), corporate spend management, and business analytics will significantly expand. Every customer will have A.I.-informed suggestions that will help optimize payments and reveal ways to improve their financial position by providing a series of choices. “Do you want to save this excess money in your account, move to your brokerage account for investment or prepay a portion of your car loan? Here is how we score your choices based on past performance….”

Now that we are all accustomed to our fitness apps, banks will be able to also reflect payment counts, streaks, closed rings, and other financial behavioral motivations. The technology, driven by payment data, will increase the engagement of customers to new levels. Money will become fun again as customers can make more informed decisions yet remain firmly in control of their financial future.

Customers will be able to get easy tax and accounting reporting that is elusive today. If a payment includes several components, such as payment for products, services, tips, and taxation, each will be itemized and reported separately and in aggregate. The detail will allow new reports to be created, such as carbon offsetting or an environmental, social, and governance (ESG) scorecard.