Should Congress Increase FDIC Insurance Limits?

In the wake of regional bank failures, one potential answer to equity shorting and bank runs is having the FDIC increase deposit insurance. The regulators are considering three options: raising the limit above $250k, raising the cap for only certain accounts (such as banks’ business accounts), or eliminating the cap entirely. Increasing insurance coverage on bank deposits will have unintended consequences and results contrary to what those in the banking industry want and what the U.S. economy needs.

Bank Failures and Uninsured Deposits

Strong, vibrant, and broad credit availability are essential to a thriving capitalist economy. The U.S. private and public lending markets are the world’s envy, with a wide availability of financing options for many capital seekers across the entire capital stack. We believe any change to the FDIC insurance coverage should aim to maintain and advance our credit markets.

The proper function of a free-market economy is to allow outperforming managers to succeed in their businesses and underperforming managers to exit their businesses. While the economy needs to provide consumer and commercial clients with banking choices, five thousand banks are probably too many. However, the ordinary course of acquisitions and mergers provides a safe and orderly redistribution of capital from underperforming to outperforming managers. Unfortunately, it is disruptive and costly when banks fail and Congress, regulators, and the public fret over the continued operation of the banking industry. We want to continue to see outperforming banks acquire underperforming ones while continuing to provide consumers with alternative banking choices.

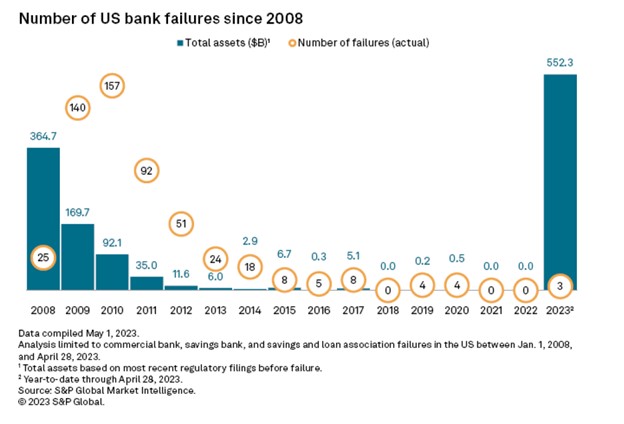

After the recent bank failures, the FDIC will soon publish a report detailing how they plan to replenish their fund. The plan will likely involve charging the biggest U.S. banks substantial fees while sparing banks with assets under $10 billion. With the collapse of First Republic Bank, the 2023 total of failed bank assets is now a new annual record – as shown in the graph below. We have witnessed more bank failures by asset size in 2023 than in 2008 and 2009 combined.

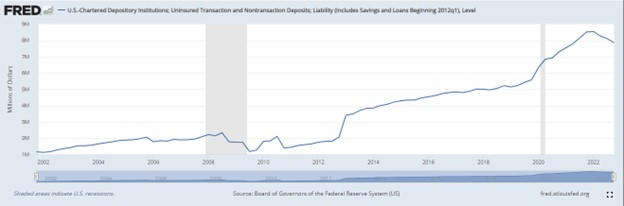

The percentage of uninsured deposits in the banking industry has been increasing steadily since 2002 but has surged in the last ten years, as shown in the graph below, and is now $8T across all chartered institutions.

Agency Problem and FDIC Insurance Limits

The FDIC receives no appropriations but is funded by premiums levied on banks. The FDIC insures trillions of deposits at banks and thrifts, but the fund currently holds only enough cash for about 1.30% of all deposits it insures. When the fund covers the loss for depositors at a failed institution, the cost is borne by the industry and passed along to customers, who must then pay a higher price for products and services. Ultimately, as FDIC insurance becomes more active, the entire economy suffers as the intermediation of funds becomes less efficient.

The question that Congress must address is how to balance the promotion of capitalism (where outperforming banks survive and underperforming banks do not) and minimize the use of FDIC payouts (because bank failures are disruptive and costly to the economy and society).

The answer lies in minimizing the agency problem in banking. The obvious agency problem in banking is the conflict of interest between bank managers, who are almost always stockholders, and our industry (and ultimately our economy and society). Humans are designed to maximize personal outcomes and will take more risk if the cost is borne by another party (FDIC insurance). There is no escaping this conclusion: FDIC insurance promotes risk-taking by managers. Expanding deposit insurance creates more incentive for greater risk-taking by managers.

Can Regulators Help

The banking industry needs regulations and regulators to review banks. However, more regulation and supervision will not outweigh the moral hazard of providing additional deposit insurance. The more than 500 bank failures in the last 15 years (all regulated and supervised) are witness to that fact.

Further, regulators favor expanded deposit insurance for business accounts because those accounts pose greater financial stability concerns than other types of accounts. Again, this may be short-sighted. Deposit insurance should be available for those who cannot assess the risk of their deposits or cannot access that risk when balancing the at-risk deposits versus the resources needed to do that analysis. Businesses that make credit decisions in the ordinary course (for example, on accounts receivable) can make that assessment. Deposit insurance makes sense for grandma and grandpa, who should not be expected to pour through a 10K to safeguard their life savings.

FDIC Insurance Conclusion

Regardless of how the FDIC recommends changing bank deposit coverage, an increase in coverage will come with a cost. Banks bear that cost (unfortunately, both well-run and poorly-run), consumers bear that cost, and ultimately society bears that cost because we will have a less efficient lending market. Regardless of where the insurance limit is set, some deposits will exceed that limit, and the confidence problem will persist. We promote more confidence in our banking system by having fewer underperforming banks and not hiding underperforming managers by increasing their access to insured deposits.

No reasonable deposit limit would have prevented the failures of Silicon Valley Bank, First Republic Bank, and Signature Bank. These banks failed because the market changed (interest rates increased rapidly), and the management teams at those institutions did not choose to react and manage risk accordingly.