The Customer Problem Resolution Secret

If your bank truly wants to be known for service, the very first step is to get your problem resolution process right. When it comes to problem resolution, the two metrics that matter the most are the number of interactions required to solve the problem and the time it takes to solve the problem. The less number of touches you have and the faster you can solve the problem, the higher your post-resolution customer satisfaction. In this article, we explore the data around customer problem resolution and show why measuring associated metrics may be the most important thing you can do to be able to deliver on your value proposition of service.

The Need To Improve Customer Problem Resolution

Ask almost any community banker, and they will tell you their value proposition around their bank revolves around service. They are local, they are close to the customer, and they have limited bureaucracy are all factors that get brought up as to why the bank can deliver on its promise. Unfortunately, the data reflects something different. Either all those factors don’t matter, or the bank is unable to execute on its promise.

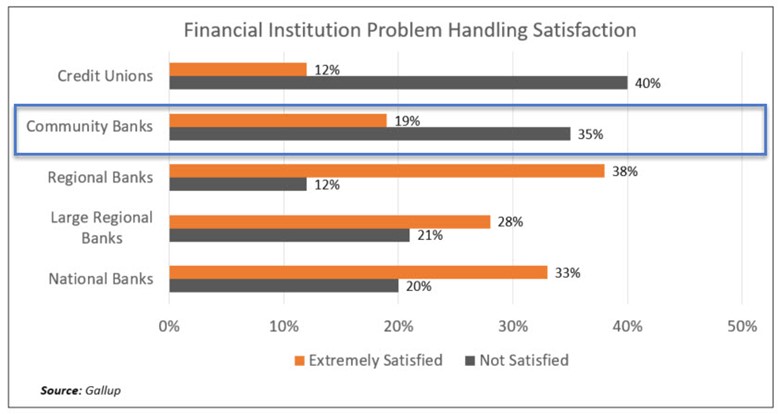

Consider a Gallup poll on customer satisfaction around problem resolution at banks and credit unions. As can be seen by the data below, size and being “Extremely Satisfied” are about 64% correlated. The larger your bank, the more likely your customer is going to be satisfied with how their problem turned out. Conversely, the smaller your bank, there is a 60% correlation to being unhappy with the outcome of your resolution.

At 19%, community banks ranked only above credit unions in delivering customers that were “extremely satisfied with the outcome of their problems and a whopping 35% that were “not satisfied.”

Now, we don’t know if there is causation in these statistics, but at some level, there likely is, as the larger your bank, the more formally you address the customer experience and problem resolution.

Why Customer Problem Resolution Matters

Solving problems is central to customer service. Banks can cut wait times in branches, speed up commercial loan approval times and eliminate fees, but it is problem resolution that has the most significant impact on satisfaction and engagement scores. Consider that 15% of all bank customers experience a pain that requires an intervention. As a baseline, those customers that don’t have problems have an average engagement score of about 30%. These are customers that pick up phone calls, participate in bank events, and open emails.

For those customers that do have a problem, if you exceed their expectations in solving their issue, engagement shoots up to approximately 45%. They start to look at other products, engage in events, and open emails at a greater rate. However, fail to solve their problem to their satisfaction, and the engagement rate drops to less than 5%.

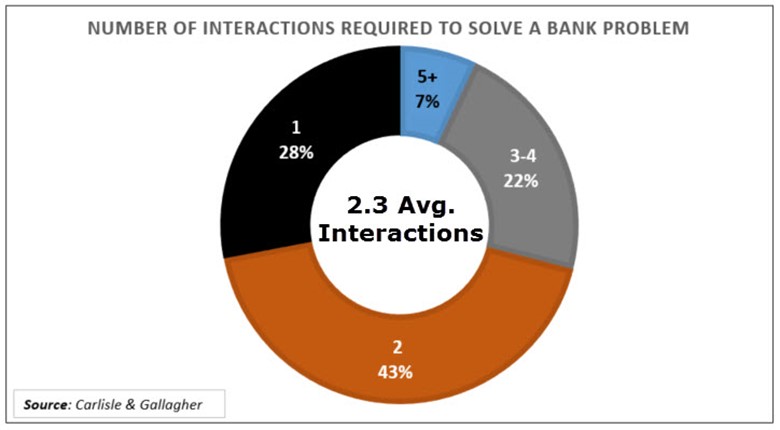

A customer satisfaction poll from Carlisle and Gallagher shows that 20% of bank customer problems are not resolved, and 18% are only partially resolved. While this performance is dismal, the good news is that there is ample upside for banks that can improve.

Reducing Interactions In Customer Problem Resolution

To solve the average problem in banking, it takes a little over two interactions with staff which is one more than banks should have. Another way to look at this data is almost three-quarters of problems take two or more interactions. This is a problem as with each interaction, both confidence, and satisfaction with the institution drop.

Feeling like a valued customer, trust, and confidence in a bank are all highly correlated to the number of interactions required to solve the problem. As can be seen below, after having two or more interactions with bank staff to solve a problem, customers feel less valued, less trustworthy of their institution, and less confident by more than half.

Further, if you solve the problem with one interaction, the likelihood of that customer doing business is approximately 22%. If it takes two or more interactions, that probability drops to 10%. If you fail to solve that problem, the likelihood of gaining additional business is about 1%.

How Wells Fargo Attempted To Solve The Problem

Wells Fargo set out to solve customer problem resolution a few years ago and sought ways to improve bank customer service. The plan called for more consultative selling, more resources devoted to customer training on technology, and reduced wait times for all bank services. In addition, the Bank rolled out new protocols to handle customer disputes. The new framework calls for getting closure to the issue in a single session without a full handoff to another person, office, or call center.

Solving Problem Resolution Issues

To take Wells Fargo’s initiative further, community banks can also take the following steps to improve problem resolution:

Single Interaction Empowerment: Restructure your training, policies, procedures, and approach to have the employee that takes the problem solve the problem. Provide enough information, technology, freedom, and authority to ensure the issues get resolved quickly and without further interactions. Doing so not only increases satisfaction but would likely result in overall cost savings by reducing collective staff time on each issue.

Workflow & Track: Create a defined process for problem resolution, then track problems through the workflow. Tracking the problem type, time to resolve, and the number of interactions helps increase the probability of improving the problem resolution process over time.

Connect the Customer: While mapping branch interaction is straightforward, it is worth investing in online and mobile chat functionality that connects the customer to the best person or department to solve the stated problem (One of the keys to Nubank’s success as we detailed HERE). The advents of chatbots and artificial intelligence have made this technology affordable, efficient to deploy, and effective.

Solve Problems Before They Are Issues: You likely already know where the problems will occur in your bank. Statistically, they have to do with checking fees, misapplied loan payments, credit/debit card issues, and mortgages. These areas are great places to enhance each product, service, and policy to eliminate problems. Further, both the staff and customer can be trained so issues can be spotted early and solved before they become formal problems. If you don’t already have one, create a customer and employee listening program where product and service improvement ideas can be captured, evaluated, and executed.

Monitor and Leverage Social Media: These days, the first sign of a disgruntled customer or employee usually occurs on social media, most likely on Twitter and Facebook in that order. Make sure your problem resolution team monitors and has the ability to respond early. It is better to handle the issue quickly and early through electronic channels instead of forcing the customer to come into a branch or use a call center to spend even more of their precious time. A good McKinsey & Co. report on this topic can be found HERE.

Putting This into Practice

Technology makes it easier and easier to solve customer problems if the bank is willing to listen and respond. Social media, for example, is free for any bank that wants to train their staff on how to handle problems over this channel. Video conferences, messaging apps, webinar applications, and similar technology platforms make it easier than ever to connect internal specialists to help solve a customer’s problem as fast as possible.

The biggest thing that holds community banks back from delivering world-class problem resolution is culture and the desire to apply a quantitative approach to solving customer problems. If your bank is serious about standing out, be sure to take another look at your retail and commercial problem resolution process and see where you can improve. Banks like Wells Fargo know that doing so isn’t a “nice to have.” It is a must-have.