Using the Hybrid Term Loan

For decades, community banks have structured term loans as 5-year fixed-rate facilities. In the last six months, the percentage of 5-year fixed-rate loans at community banks has increased by approximately 25%, but this same bucket has held steady at larger banks (those over $25B in assets). We believe that now is the right time for many community banks to abandon adding five-year fixed-rate term loans and start adding hybrid term loans.

Industry Trends

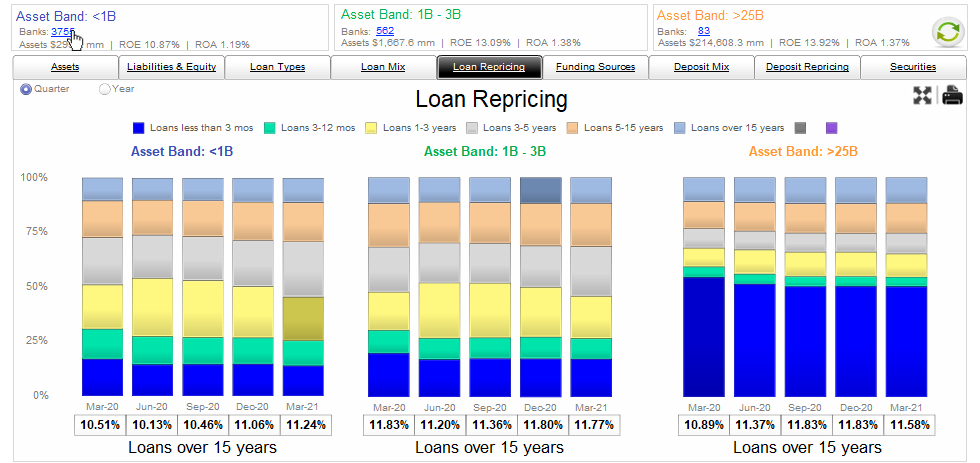

The graph below shows loan composition for three groups of banks based on asset size. The grey band in the graph represents three to five-year fixed-rate loans. This grey band has been expanding rapidly for community banks (under $3B in assets) for the last six months. The same grey band has held steady for larger banks.

Some of the reasons for this development are obvious. In a low-interest rate environment, customers would prefer to lock in their cost of borrowing for as long as possible. While most banks are reluctant to extend the balance sheet duration for seven years or longer, many lenders are accepting five-year fixed-rate loan duration. Banks are also reaching for yield, and lenders can currently obtain 78bps in additional yield by offering a 5-year fixed-rate loan – so the five-year bucket tends to fill up fast.

Now is Not the Right Time

There are a few reasons why now is not the right time for banks to book fixed-rate loans beyond three to four years.

First, extending asset duration when interest rates are normal may be a prudent strategy. But extending asset duration when interest rates are at historic lows, and the economy is recovering from a pandemic lead recession is problematic. Historically, bankers have argued that interest rates may rise or fall depending on future events. However, in today’s market, there is substantial downside risk (where interest rates rise and hurt banks’ NIM) and very little upside benefit for these loans (where interest rates fall and banks can expand NIM).

Second, many banks have room to add two to three-year asset duration on their balance sheet. Unfortunately, that is not the reality of the commercial loan market today. Borrowers who are financing long-term business or real estate assets are looking for fixed-rate locks for longer than three years – borrowers commonly request 7, 10, 15 and even 20-year fixed-rate commitments. Many community banks would benefit from extending their balance sheet duration slightly, but not in the 5 to 20yr loan buckets.

Third, the Federal Reserve has continued to keep monetary policy accommodative, and the economy has been successful in stoking current inflation and even higher expectation of inflation. Because inflation decreases real return for lenders, the nominal yield must be adjusted for expected inflation over that period. Real yields are equal to nominal yields minus the expected inflation for that period. Given the current five-year Treasury yield and the current five-year Treasury Inflation-Protected Security yield, the real five-year yield is currently negative 1.77%. The graph below shows real five-year yields from 2003 to the present.

Over the last 20 years, inflation has been around 2.0% per annum (with some temporary variation caused by economic events). But current and expected inflation has flared up. What does that mean for lenders? Most bankers would ignore this reality by stating that they are not buying treasuries but rather making loans. However, real yields are as much a consideration for fixed-rate loans as for securities. A five-year fixed-rate loan priced today at 3.00% is expected to yield the bank a real yield of only 44 basis points. That is the expectation, and if inflation is higher than expected, the bank’s yield would be lower, and vice versa. This real yield is not enough to cover credit costs or origination and maintenance costs of a commercial loan. Now is the wrong time to expand the balance sheet with five-year fixed-rate loans because nominal yields are low and inflation expectations are at an inflection point.

The Solution

Banks need to manage the cash flow on a loan so that a borrower can achieve loan payment stability, and the bank can choose the appropriate upfront fixed-rate period. This concept has been around for a long time. We have been structuring hybrid loans where the borrower can lock in a fixed rate of financing for up to 20 years, and the bank can structure an initial fixed rate of interest, and thereafter the loan converts to an adjustable-rate to eliminate inflation risk for the bank. We urge community bankers to investigate how they can structure a similar product for their bank’s balance sheet, and we are standing by to share our ideas further by email or by phone.