The Secrets of Good Loan Commitment Letters

Good commercial lenders use commitment letters and proposal letters to their advantage. A proposal letter (or letter of intent) expresses interest from the lender before credit approval is obtained. A commitment letter evidences the lender’s commitment to lend. It is only furnished after preliminary credit approval and typically contains the following language: lender commits to provide the loan on, and subject to, the terms and satisfaction of conditions set forth herein.

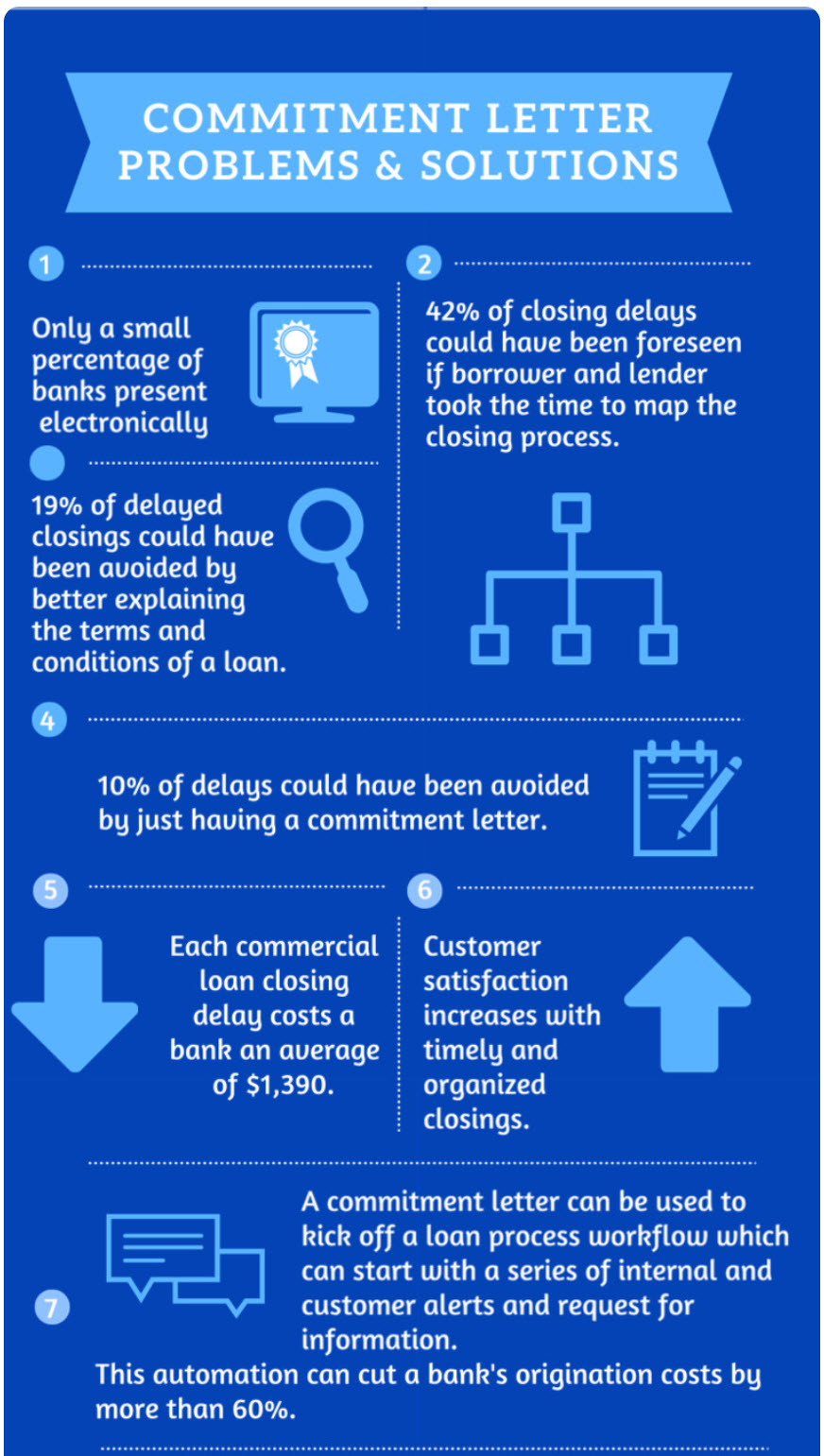

Well-crafted commitment letters can help lenders close loans quicker, eliminate more competitors, secure better pricing, and obtain the desired credit structure.

Purpose of the Commitment Letters

There are various reasons why a borrower seeks a proposal or commitment letter. The borrower may need to refinance a project or make an acquisition. The proposal or commitment letter assures the borrower that financing will be available when required. A third party may want the proposal or commitment letter because it relies on the borrower having the funding for payment – in the case of a contractor for a construction project or a seller in a purchase and sale transaction. Lenders must be mindful that they deliver tangible value when issuing a proposal or commitment letter and should be compensated equitably for that value.

The lender has several reasons to issue a proposal or commitment letter. The lender wants to ensure that the borrower will reimburse the lender for out-of-pocket closing costs leading to the loan documents. The lender also wants to know that when the credit approval is obtained or due diligence is completed, the borrower will accept the loan on the conditions of the proposal or commitment letter.

However, the most crucial reason for the lender to issue a letter is to eliminate competition. The faster a lender can get the borrower psychologically and financially committed to the bank, the more likely the borrower will stop soliciting other offers, the more likely that the lender will get better terms and conditions, and the more likely that the lender’s pricing will not be undercut. When properly structured and applied, a proposal or commitment letter will get the lender a better-structured loan at better pricing for the bank and with less competition.

Fees For Commitment Letters

Both parties should not fully execute a commitment letter without consideration from the borrower. The fee may be earned upon execution of the letter, and an additional fee may be earned upon closing of the loan. If properly used, the commitment letter will dissuade the borrower from continuing to shop the loan to other banks. The fee on the commitment letter must be a substantial disincentive for the borrower to continue discussions with other banks. The lender must understand how the fee translates into basis points on the loan spread. For example, consider a $10 million term loan for ten years where the borrower paid a $50,000 commitment fee. Some lenders would conclude that the 50bp fee would create a strong disincentive for the borrower to continue to shop the loan. However, that $50,000 fee represents only 7bps of spread for the credit term. Therefore, if approached by another bank offering similar terms at more than 7bps lower spread, a rational borrower would easily walk away from the $50k fee.

Lender Strategies

The best way to create borrower stickiness at the proposal letter stage is to understand what the borrower needs and, assuming you can obtain approval from the bank, convince the borrower that you will deliver the terms, conditions, and pricing the borrower seeks. A competent lender will convince a borrower not to approach other banks if the lender can promptly provide everything the borrower requests. We make it clear to our borrowers that if they want to seek other bank alternatives, they may do so, but we will not issue proposal letters for the borrower until they have verbally committed to our offer. We feel strongly that we will not give proposal letters if the borrower seeks proposals from other banks. If the borrower wants to keep shopping, they will do so without our commitment.

At the commitment letter stage, we always charge the largest fee the market will bear. The borrower is also charged all closing costs, including legal. However, the best way to create borrower stickiness at this stage is to play the psychological card. Lenders close many deals each year, but most borrowers close very few loans. Lenders who demonstrate knowledge of the closing process and offer sound advice to the borrower establish themselves as trusted and insightful advisors. Emphasize your ability to add value to the borrower’s needs and de-emphasize any adversarial relationship with the borrower (even though some negotiations will pit the bank against the borrower).

Another psychological strategy is to play up the bank’s concessions to the borrower on structure and price. In today’s market, bankers should not dilute credit structures beyond acceptable boundaries. But that does not mean we can’t communicate to the borrower that their credit approval required hours of credit adjudication and management dissent, and they are getting the deal of a lifetime just because the bank likes the borrower’s business and is looking to establish a long-term relationship.

Conclusion

The best lenders deeply influence their borrowers because they understand the borrower’s needs and provide sound and insightful advice. Borrowers pay attention to trusted advisors. The proposal and commitment letter stage is an excellent opportunity for lenders to assess their relationship with and influence the customer. A lender wants to convince the borrower that the bank’s commitment reflects the financing that the borrower sought and that seeking additional financing options is unnecessary. In a future article, we will identify some of the mistakes bankers make in their proposals and commitment letters.