Credit Stress Test Loans BEFORE You Book Them

When banks price loans, they stress the borrower’s ability to repay the loan under adverse credit conditions. For example, credit officers will underwrite to various interest rates, vacancy rates, revenue projections, EBITDA or NOI assumptions. However, most banks will not subject that same credit stress analysis to calculate that loan’s ROE. This is unfortunate because credit losses can change a loan’s (and loan portfolios) ROE significantly. While credit stress analysis can show that the loan performs under certain derogatory conditions, those same conditions may cause the ROE of the loan (or portfolio) to turn substantially negative. Banks should have the data to assess a loan’s desirability in both a base case and stress case by comparing the ROE in each instance.

Why Credit-Stressed ROE Matters

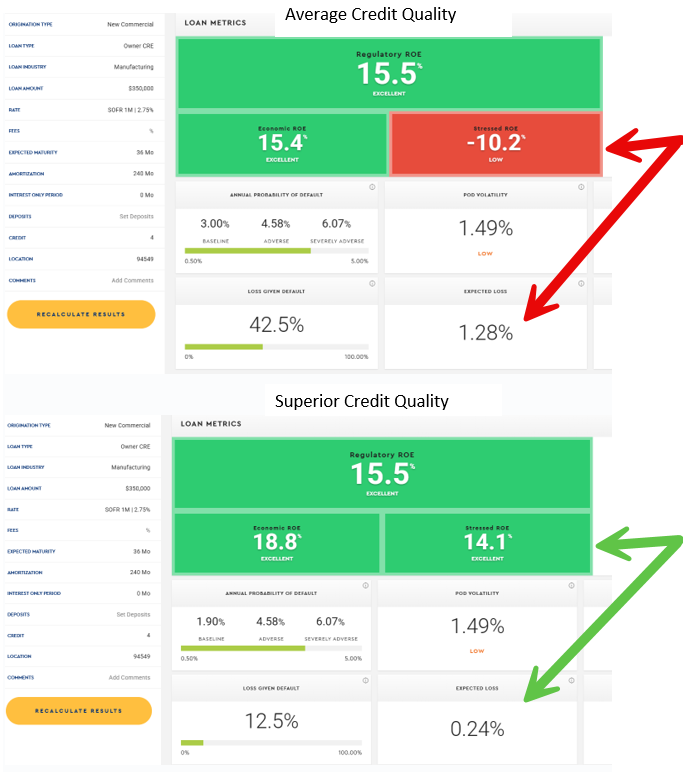

ROE measures the return to shareholders after accounting for various risks. The largest risk for commercial loans is credit risk. The magnitude of that credit risk can have severe impact on ROE. Loan losses (or expected loss (EL)) is the product of probability of default (PD), loss-given default (LGD), and exposure at default (EAD). Credit-stressed ROE will assume higher than normal EL based on historically observed standard deviation. For example, a loan might have a 1.28% EL and ROE of 15.5%, but under a two-standard-deviation credit-stress, that EL increases to almost 3% and the ROE becomes negative 10.2%.

But the most important reason to measure ROE using credit stress is to compare the performance of different quality loans in severe credit environments. Under normal conditions, average and superior credit’s ROE is similar, but in a recession, the superior credit retains ROE while average credit turns negative very quickly.

Below are two screen grabs showing two identical loans, with the same pricing, but the first loan is an average credit quality with 1.2X DSCR and 75% LTV, while the second loan is superior credit quality with 2.0X DSCR and 50% LTV. While the regulatory ROE is the same for both loans (not surprising), the stressed ROE is substantially different. In a credit downturn, we expect the superior credit quality loan’s ROE to decrease only marginally. Meanwhile the average credit quality loan’s ROE in a downturn becomes highly negative.

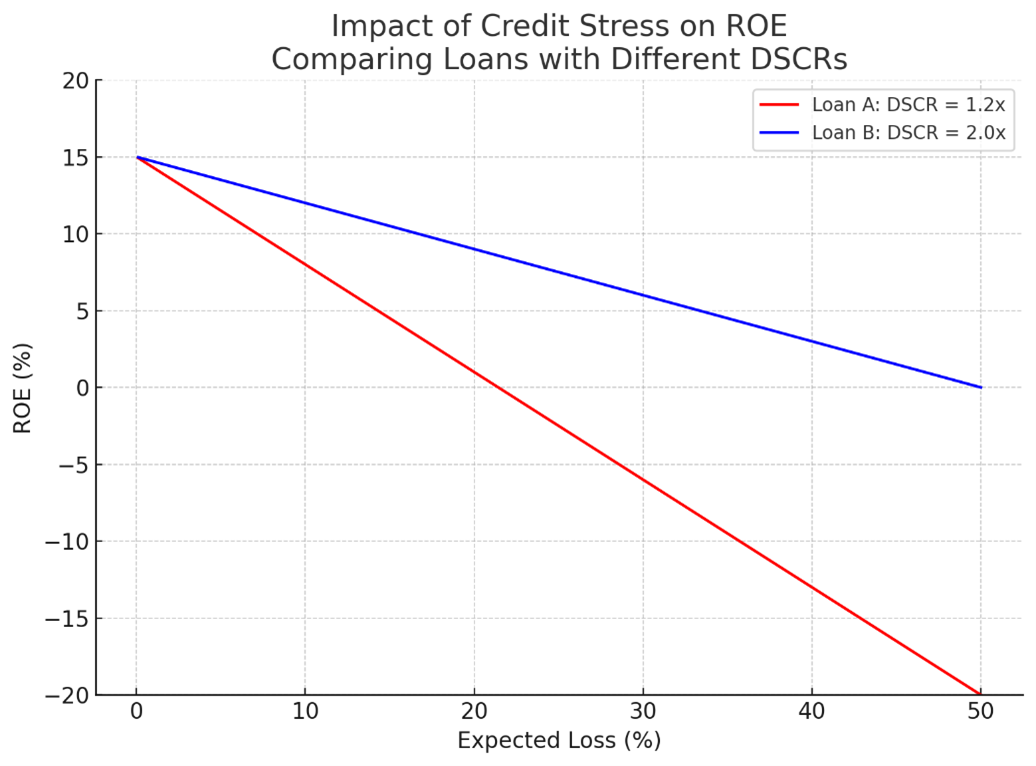

This ROE/Credit quality relationship can be summarized by the graph below. Higher credit quality loans retain their ability to service loan payments in adverse credit conditions, resulting in higher bank profits. The higher leverage of average loans amplifies the downside risk, causing ROE to decline significantly more as EL increases with credit stress.

If we believe that an economic slowdown is likely during the period of the loan’s commitment, then bankers are much better off to compete for less risky loans because those borrowers better compensate banks for credit risk. Of course, these customers usually command a lower credit spread.

Conclusion

Historically, bankers have underpriced higher risk loans and shied away from higher credit quality because of lower yield. This makes sense for the following reasons:

- Riskier credits have a wider dispersion in performance (the distribution around the expected probability of repaying is wider), leading to more possibility for mistakes. This is why lower credit quality loans have much lower expected ROE in a downturn. Unfortunately, most bankers do not measure this risk.

- Credit risk is a distant cost, while yield is immediate gain. Humans tend to favor immediate gratification at the expense of a remote cost.

- Bankers are typically paid incentives for higher yield, but the bank’s shareholders must pay for future credit mistakes. This is a classical agency/principal dilemma.

- Competition is continually leading us astray in pricing. The adage in the industry has been that you can only perform as well as your dumbest competitor. If your competition is underpricing risk, the borrower is more than willing to take someone else’s capital, and your only choice is to lose that loan. It is more likely that many lenders will inevitably make a risk analysis mistake on the riskier average loan than the less risky superior loan.

Measuring a loan’s credit-stressed ROE allows bankers to optimize lending decisions especially after extended periods of economic expansion or with the expectation of a credit downturn. We believe that community bankers should be targeting the best credits for long-term retention, and those clients are highly contested, translating to lower yields for lenders but higher long-term ROE especially in a downturn.