7 Rules To Improve Total Experience Using the “Time-on-Task” Methodology

We covered various frameworks to “wow” your customer HERE. We covered why “Time-on-Task” (or the companion Customer Effort Score) is the ultimate metric in banking HERE. In this article, the last in the series, we give you seven rules to improve your bank. While these rules were derived from improving time-on-task, they can enhance bank performance no matter what metrics a bank uses for customer, employee, or total experience (the combination of employee and customer experience).

1. Design or pick the fastest customer experience.

When designing or choosing new technology, select the one that employees or customers can complete the fastest. We have seen this a thousand times, and it is ALWAYS a mistake – banks do demos of technology but rarely try to use it themselves before purchasing it. Before any banker agrees to a user interface or chooses a vendor, they should clock themselves to complete a task with the application and figure out a roadmap for improvement. We don’t care if it is an ATM, a new branch design, a fraud database, a deposit account opening product, or a core system, time matters. The fastest technology isn’t always the best, but it usually is.

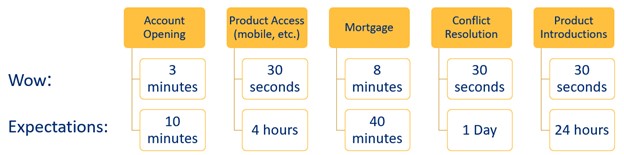

Usually, speeding up technology comes down to intelligent design around a thoughtful process and using existing or third-party data to limit input time. Below are some benchmark times for popular products or events and the difference between “wowing” and meeting expectations.

2. Figure out how to fix the critical path of problems to improve time-on-task.

When speeding things up – don’t just fix the problem; fix the problem that led to the problem. A classic example of this rule is the need for the customer to call back or stop a process to go get information. A customer gets stuck during the digital loan application process because the bank did not provide adequate education before or during the process.

Any bank’s call center is a pantheon of neglected critical problem paths. We estimate that almost 25% of a bank’s calls stem from a problem other than what the customer said their stated problem was. The situation is worse because the bank thinks they are doing a good job. Bank call center managers often pridefully point to their “first-contact resolution” (FCR) performance. By far, the most common problem a bank has are password issues. The call center usually expertly resolves these issues. However, few banks stop and think, are there better ways to handle authentication and identity validation? Can the bank move to a new system to utilize biometrics and behavioral science to limit the requirement to change passwords so frequently?

Although bankers are well-equipped to “forward-resolve” and anticipate downstream issues, they rarely do. This is often because a task is outside of their responsibility, requires cross-functional effort, or from a personal lack of focus on total time-on-task.

Even when the banker does think like a customer and anticipates issues, solutions often come at the expense of employee effort. As stated before, time-on-task needs to incorporate the total effort expended by both the employee and the customer.

Data and artificial intelligence are now coming to the rescue at banks. By mining customer interaction data, bankers can understand the relationship between various issues. These “event clusters” often uncover employee training and customer education gaps.

For instance, banks have many adjustable-rate commercial mortgages coming due. Event data shows that customers will have a variety of issues due to higher rates, broader than current credit spreads, poor loan structures, and Libor index issues. Many banks will send a notice and wait for the customer to call if there are any problems. When they do, they will resolve the issue just fine. However, many customers will not call and instead will go to another bank. Intelligent banks anticipate these issues and reach out to borrowers with a pre-designed solution. The result – time-on-task is dramatically reduced.

Another classic example comes when a customer is onboarded for a particular product, such as treasury management services. Customers often call asking questions about specific procedures or features. Innovative banks not only provide quick tutorials upfront during the onboarding process but have pre-built customer journeys that follow up with automated educational material around anticipated events such as month-end reconciliation or tax time. Further, they show where the customer can access their self-help section, complete with videos and frequently asked questions.

The result? Banks can reduce their “calls per event’ by around 16% while increasing customer product churn rate by 6%.

Financial institutions are also now making greater use of personalized websites and marketing, offering “suggested next steps” to customers AND employees during particular transactions. Call or go online to change your address at Fidelity Bank, and you will receive a prompt with information about how to order new checks and/or update your loan insurance forms. To recap, they not only resolve the problem the customer came to solve, but they are solving all the event clusters around that problem, thereby preventing future issues.

The result? Fidelity has reduced follow-up problems and calls by 5% and has reduced time-on-task.

3. Train bankers to solve the emotional problem rather than just the problem.

A Harvard Business School study uncovered that 24% of repeat problems stem from either generalized anxiety or lack of trust. Chase solves the fear of technology by making the customer take out their phone to walk them through account opening. While branch reps could do it themselves, the more significant issue is that the customer hasn’t taken the time to understand the technology. They build confidence by holding their hand and helping the customer solve their own problems. That confidence translates into fewer problems in the future.

Often, a customer doesn’t trust the banker’s information. This usually occurs when a banker evokes “Bank policy.” Instead of taking the time to explain why the bank has the policy, the response often generates distrust causing a whole string of problems and increasing the time-on-task for both customers and employees.

Here, banks sometimes unconsciously train their bankers to use words that trigger negative reactions and deteriorate trust. Words and phrases like “policy,” “that can’t be done,” “we never do that,” or similar must be modified to be more solution oriented. Instead of “we can’t reverse those fees,” the solution is reframed as “if you can consolidate another bank account, we can move you to a different product where you won’t incur those fees.”

The result? By just reframing the solution and using more positive language, one company reduced their Customer Effort Score by 19% for their commercial customers.

We know one bank teaches bankers how to listen to certain customer personality types. They then teach how to respond with the best tone and level of information that is fit for someone that is a “controller,” a “thinker,” a “feeler,” or an “entertainer.”

The result? This institution reports that repeat problems are reduced by 40%.

4. Look for, and eliminate channel disconnects.

While allowing the customer to solve their problems is a counter-intuitive surefire method to reduce time-on-task and improve the overall experience, banks often get sideways. More than half of bank customers usually try to solve their own problems but can’t. They get stuck trying to figure out an online solution, go to the website first, or even go into a branch only to get redirected to someone on the phone.

Many banks do not prioritize improvements to their website and building it out with more functionality to solve problems. Huntington Bank built its website to handle a variety of customer service issues after authenticating the customer, and customer satisfaction improved greatly. Banks that go down this path can leverage data to figure out what is the likely problem. For example, a customer has a mortgage and comes to the website. Personalization automation on the website, recognizes the customer and then checks the status of the last payment and the next payment date. If the mortgage payment is past due or the payment is coming up in the next ten days, the website engages with the customer to direct them to the proper place, which may be the payment mortgage section, chat, or the call center.

Here, online chat can be a powerful tool as it can provide information to the customer and record the customer’s path and sentiment to derive intent. Few other customer service channels can do this. By looking at repeated problems and solutions, banks can materially increase the number of issues that can be resolved through self-help channels. Banks that roll out online chat and use chatbots can often quickly reduce calls by 10% and speed time-on-task.

As a side note, banks that look at their customer data know that customers who go to the website first to try to resolve a problem don’t want a series of automated emails to help solve their problem. Once they try self-help via a website, an in-person call is almost twice as fast to resolve the issue as trying to solve it with website education or emails.

The overall result? Banks that take the time to build out their website’s self-service capabilities can go from handling an estimated 30% of problems through this self-help channel to managing 80% or more. Just having better search functionality on our website reduced problems dramatically by getting the customer to the right area for the required information.

5. Use negative customer and employee feedback to fuel solutions.

Many banks send out surveys to benchmark satisfaction and performance. However, many of these banks often act on the information they collect without rigor. One bank developed a “special weapons and tactics team” that was empowered to call customers that gave the bank low scores and then solve the downstream problems leading up to those scores. They had the authority to change processes, marketing, training, and customer service response. The result – they report that issue resolution has increased by 31%.

6. Don’t confuse speed and quality when improving time-on-task.

Bankers should not trade speed for quality. Time-on-task must be calculated to solve the customer’s intent, not just the direct problem. While solving a challenge about opening up a savings account is good, solving a challenge about saving for retirement is better. Make sure your bankers ask enough questions to get to the “real” objective, not just the stated objective.

7. Provide more authority to front-line workers to reduce total time-on-task.

Many customer-focused banks make the mistake of emphasizing productivity metrics such as average call time (we are picking on call centers only because that is where the best data is). While a bank may feel they are improving time-on-task, they are not only often ignoring the customer’s intent, but they are not giving their bankers enough space even to try to solve the intent or emotional layer that comes with the problem.

One company removed its call metrics only to find that time-on-task increased initially. However, repeat calls fell by 58%. This company moved to a Customer Effort Score (similar to the example question below) to rate performance instead of relying on call metrics.

Ameriprise Financial, for example, recorded every time their bankers said some derivation of “no” to the customer. It was no surprise when the company found that many of the policies resulting in the “No” were outdated. Either the regulation was modified, bank policy didn’t keep up, or technology arose to solve the problem and reduce the inherent risk of the desired action. After one year of recording these “No’s,” the bank changed or eliminated 26 policies.

Similarly, another bank developed a service and branding campaign around “AskOnce.” The promise is that the banker that picks up the phone stays with the customer from start to finish. If the bank had to get their “Tier 2” IT group on the line, instead of Tier 2 calling back as an independent action, the original rep stayed with the customer to facilitate the call and ensure the problem was resolved.

Putting This Into Action

Above are just some of the many examples banks have focused on to reduce total effort and dramatically cut total time-on-task. A massive shift is taking place in customer and employee preferences where time is more valuable; friction directly correlates to disloyalty, and ease of use is amplified on social media. Although most bankers feel that face-to-face or telephonic interaction is the best way to make the customer happy, our data shows that customers and employees are indifferent. Everyone is out there just trying to solve problems in the most efficient way possible. Amazon built its whole business model on this.

Banks that can reengineer their processes and improve their technology in order to reduce time on task will be the winners. Use speed as a proxy for satisfaction. Measure every internal process by the time-on-task metric and make it central to choosing vendors and partners. This trend presents an opportunity for enterprising bankers to rebuild banks around self-service, increase total experience satisfaction, and improve bank performance.