A Better Deposit Marketing Framework

Like a carpenter with a hammer where everything looks like a nail, to a deposit gather, all too often the world looks like a rate. Commonly lost is a discussion around marketing expense. In this article, we explore a deposit marketing framework that describes how bankers might want to think of the trade off between rate, deposit performance, customer profitability and marketing expense.

The Challenge of Marketing on Rate

A high-rate CD or money market offer can look cheap in terms of customer acquisition because the rate itself does the marketing. If you are a frequent reader, or have come to our annual Deposit Conference, you know we consider this “lazy banking.” Marketing on rate without product development, strategy, tactics or even a marketing plan is the easiest thing to do but it is not true “banking.”

When marketing on rate, little value is created for the franchise and oftentimes rate is the single largest destroyer of franchise value outside of credit problems. When acquiring customers with rate, the cost is paid every day on every retained dollar. A lower-rate product can look expensive upfront because of the higher customer acquisition cost (CAC), but those balances are sticker, bring better performance and have greater relationship value. As such, lifetime economics are usually dramatically better.

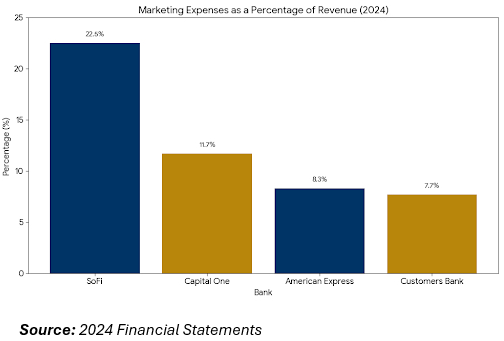

How Much Money Do You Spend on Marketing?

It often surprises bankers how much they should be spending on marketing. Unfortunately, many a bank CEO has taken the industry benchmark average of 2%-3% of revenue and have allocated a marketing budget accordingly.

That process is completely backwards. What another bank spends on marketing is largely irrelevant and possibly counterproductive. Every bank has different goals and strategies and some of the most successful banks spend 22% of their revenue on marketing and it’s not uncommon for a fintech to spend 30%.

A more effective way to think about bank marketing expense is to determine what you need to spend to accomplish your strategy. For example, when it comes to raising deposits, your alternative, with zero marketing costs, is to access the brokered or wholesale funding markets.

In similar fashion, you may decide to put a 3.85% rate on a money market account out there and for little marketing expense gather deposits via your branch and digital channels. This would come with low, sub-$2.00 customer acquisition costs but is that the right move?

To answer that question, you can be more quantitative and have some creativity and market a 2.25% money market rate. You could provide loyalty points, give away a toaster, structure a partnership with a local merchant or launch a campaign around putting your tax refund to work.

A Quantitative Framework for Bank Deposit Marketing

To decide if you are going to market a 3.85% rate with low marketing expense (Option 1) or a low rate with higher marketing expense (Option 2) we turn to this formula where we look at the present value of balances over the life of the account and adjust for acquisition cost, servicing, cross-sell value and cannibalization cost.

Lessons From the Formula

If you use the formula, a couple lessons quickly pop out that should be on the forefront of every depositor’s mind. We will break these down in order of importance:

- Cannibalization Can Kill You: Every time you market a deposit product, you run the risk of cannibalizing your deposit base. For a money market account, for example, a customer might take money out of their transaction account and move it into the 3.85% or the 2.25% money market account. Of course, a customer is both more likely to do this if you offer a 3.85% and are more likely to move larger balances than compared to the 2.25% offer. Cannibalization cost can overwhelm the economics of ever offering a higher rate account as you are raising your cost on new money while repricing your lower cost money. This is the largest single factor when deciding between two deposit marketing alternatives and needs to be quantified and designed around by limiting marketing to new money only (which creates its own set of external and internal marketing issues).

- Deposit Performance Matters: Note that by using this methodology, we are capturing deposit performance on a prospective looking basis as we take the forward curve and look at our expected beta, or interest rate sensitivity of the product. Balance gathered at a 3.85% tend to have a much higher beta (almost double) than balances gathered at 2.25% since the customer that was attracted at 3.85% is much more interest rate sensitive by design.

- Cross-sell Matters on the Margin: Behind deposit performance, cross-sell has an impact. That 2.25% of customers likely is more interested in service than rate. This customer is more likely to be loyal to your bank’s brand because of their longevity with the institution, your community service, your service, your branch network or because they like your product. This customer is about 30% more likely to try other products. In comparison, while you can market that 3.85% customer, that customer is looking for rate over product or service. They may or may not care if you have a branch near them, particularly if it is a digitally acquired customer. As such, cross-sell revenue is likely higher with that 2.25% customer. Not only that, but more products also usually means longer retention, so their cumulative average lifetime value is much greater.

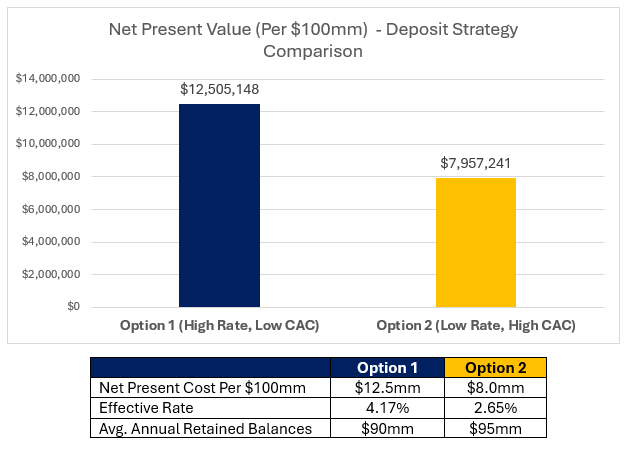

Looking at the Math

While we look to provide our calculator in the future, if you plug the inputs into the formula, you arrive at the following comparison:

As can be seen, the cost difference between Option 1 and Option 2 is a stark $4.5mm for this one campaign. Option 2 costs almost $1mm more in marketing expense than Option 1 which might make a lot of banks gulp. However, that one-time expensed is recouped through better deposit performance and improved cross-sell. In fact, a bank might economically want to spend up to that $4.5mm value difference to achieve Option 2’s deposit performance.

We also want to quickly point out that we used a static rate assumption, should rates move at all, either up or down, Option 2 outperforms even more due to the lower beta.

Putting This Deposit Marketing Framework Into Action

Before you market your deposits on rate, consider the alternative. We have our annual Deposit Conference coming up (Register HERE) where we will go much more in depth into the math and the concepts with the objective of optimizing deposit performance no matter what your strategy is.

In addition, look for more calculators and more support coming up as we look to provide community banks with more tools and frameworks to improve bottom line performance.