10 Banking Insights from Dreamforce – The Rise of “Agentic Banking”

Love or hate Salesforce, but the one thing they get right is their vision for the future. They correctly predicted the widespread adoption of the cloud, mobile, API integrations, and enterprise AI. Now, their promoted vision is the “Agentic Enterprise.” No matter if you are a Salesforce bank or not, this article breaks down 10 lessons from their recent “Dreamforce” conference as it pertains to banking.

Like Salesforce the application, Dreamforce was once again chaotic, expensive for the value, not user friendly, and you had to work hard to uncover true insights. That said, Dreamforce is often considered the single best conference to understand the macro practical innovation trends that are impacting American business.

The Major Insight – Agentic Banking

The single largest takeaway from Dreamforce 2025 was what Salesforce calls the “agentic enterprise.” Agentic banking is a shift from predictive or assistive AI toward systems that can act autonomously (with guardrails) helping bankers execute tasks end-to-end rather than just making recommendations.

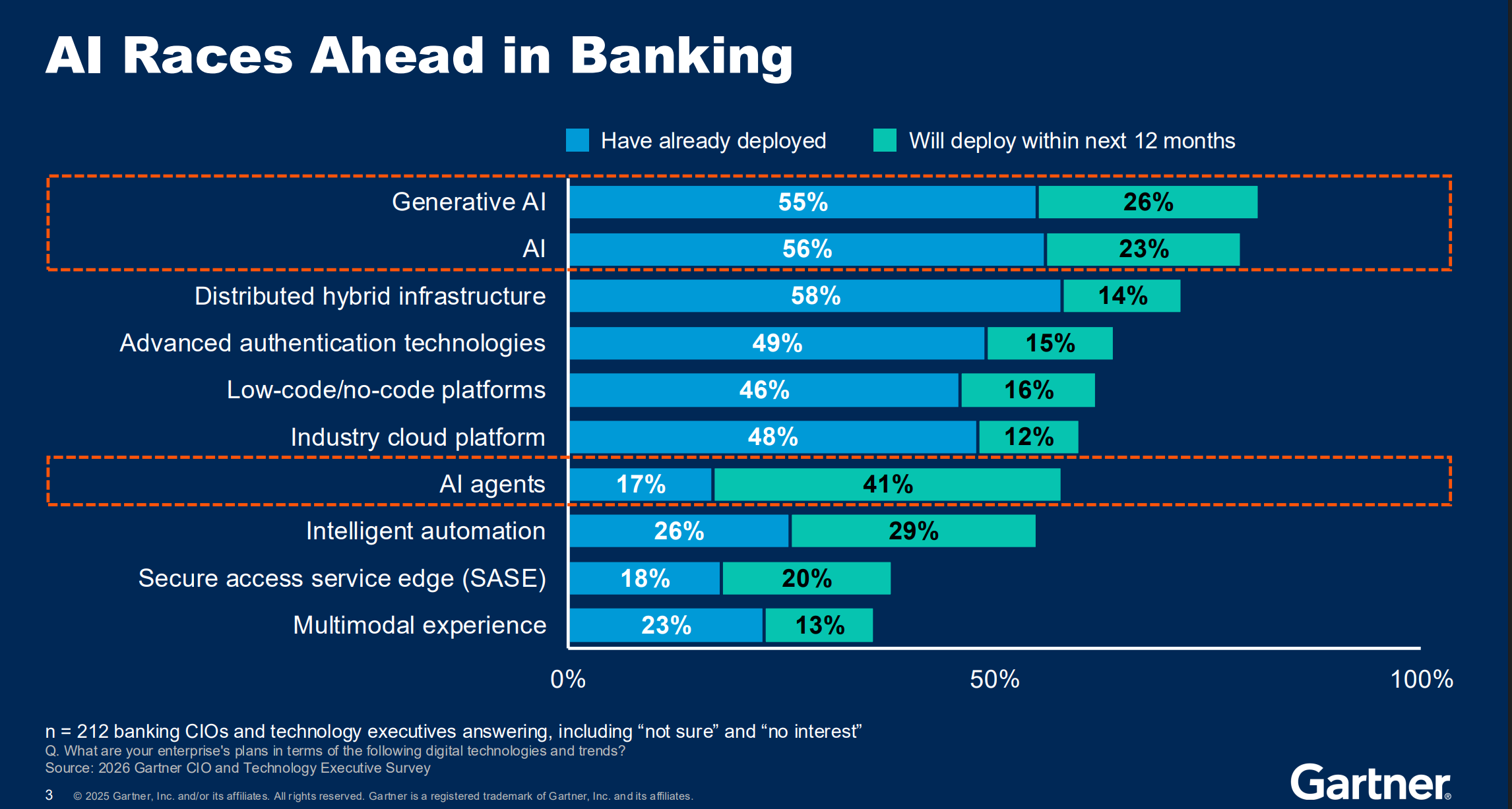

A recent Gartner poll shows that 48% of banks plan on deploying AI agents in the next year.

Where this year, agentic AI was on top or on the side of applications, now agents are embedded into the fabric. Where this year banks were focused on using AI to improve employee productivity, next year has banks focusing on an enterprise view with agentic banking targeting differentiating product, improving customer service (speeding credit approval times as an example), reducing fraud for the customer and making the customer smarter. Focus has shifted from reducing costs in the bank to making the customer’s life better.

One lesson learned in 2025 is that AI creates the most value when it is closest to solving problems for your customer, not the bank.

Like 2000 and 2015 when banks redesigned their manual processes to fit the internet and mobile, respectively, 2025 taught us to do the same for agentic AI. The difference this time is AI, itself, can help banks redesign their workflow. The clear lesson – don’t add AI onto a broken banking process; instead, use AI to reinvent the workflow itself.

Financial service agents on the Salesforce platform are growing 105% PER MONTH and have been for the past year. This is faster than any other technology at Salesforce and its evidence that American business is changing.

In the banking, the most successful use cases have been digital agents that can:

- Interact with customers (e.g., chatbots that can initiate actions such as payments, account changes, and change requests)

- Orchestrate systems cross-domain (KYC, fraud detection, credit scoring, multi-product bundling)

- Use real-time data with better context to make decisions, trigger workflows, escalate to humans when needed.

For banks, the implication is that AI is moving from “advisor to the human agent / banker” toward being a co-agent that can operate across silos (customer, operations, risk, compliance).

To pull this off, banks need to choose partners that can provide not point, or product-specific infrastructure, but enterprise infrastructure. Banks should choose these enterprise vendors by their ability to provide the framework that also give banks the ability to customize their workflow service level. Banks should focus on the “last mile” or the 20% of personalized service or technology that is going to be different than other banks and will make 80% of the impact.

Insight 2: Managing AI By Use Cases is a Problem

Banks started out governing AI by application and then realized that it was too broad. Then, banks started to manage by use case so that a bank would approve a specific AI application for a specific problem. Now banks are finding that a single use case is too narrow, and banks either need to broaden their definition of a particular use case or move to a “generalized use case application.”

Managing governance by a generalized use case application allows banks to group similar use cases together that use the same LLM and agentic workflow so that all document management applications that use the same AI tools can get approved at once no matter if it is for wealth or commercial lending. This is proving to be a huge governance timesaver for banks.

Insight 3: The Poetry of Human-to-Agent Flow

It is common to have a chatbot or voice agent as the first point of customer contact. You call a company, move along their workflow, and then ask for a human. This might be a mistake. In 2025, many mature companies using agents found that if you flip the script, the customer experience improves.

Instead of frustrating your customer and having them ask for a human, banks should consider starting with a human then quickly move to a specific voice agent that can solve a specific problem. One agent for items processing research and another to help change account information.

Insight 4: Agents are Building Agents

Salesforce introduced a number of tools that allows business line bankers to build and test agents quickly by using natural language. By “vibe coding” agents, bankers can quickly build a multitude of agents for specific purposes. What used to take months building an agent and putting it into production, now takes days.

Insight 5: Data Quality Remains Foundational

If you thought clean data was important before, in this age of agentic banking, it just became 10x more important. Since it is now faster and easier to bring banking agents into production, having quality data sources becomes the limiting factor.

Banks need to do whatever it takes to centralize and manage the quality of their data if they hope to build efficiently for the future.

Insight 6: Context and Orchestration in Agentic Banking

It’s not enough to have an AI model, linking AI agents contextually and orchestrating actions across systems is where value emerges. Agentic banking excels when you wrap UI, logic, data, rules, and workflows.

Insight 7: The Rise of Voice

Several demos by Salesforce and vendors showcased how voice agents now sound more human, have less latency, and can learn faster than text-based bots. Unlike text, voice agents now capture voice tone and cadence to better help infer emotion. When given the choice between using online text or voice bots within a mobile banking app, many customers are choosing voice.

Insight 8: Modular Architecture Wins

Banks that were moving the fastest figured out that they can produce a single agent that is modular in nature that you can use across the enterprise. Instead of building an anomaly detection agent for instant payments, the agent can be built so it can understand what data is being analyzed and for what purpose and then evoke a series of tools/vendors that are best suited for the problem.

Having agents that can now know context and can orchestrate a variety of fraud tools help solve similar problems throughout the organization and is another reason banks need to evolve governance beyond managing a single use case.

Insight 9: Stewardship Matters in Agentic Banking

Throughout the sessions, trust, safety, model alignment, and being “good stewards” came up. In banking, where trust is a core asset, responsible AI is non-negotiable. Where other industries can get away with cutting corners, banking needs to take extra time to ensure the quality, accuracy and non-toxic answers are rendered 98% of the time.

Banks must move quick, but keep balancing innovation with regulatory compliance, best practices, transparency, and auditable workflow.

Human oversight remains important as you remove humans from the process. Having an agent gateway to manage inputs and outputs combined with an agent testing and documentation tool is the key to scaling agentic banking. Transparency dashboards, error mitigation metrics, audit logs, building in kill switches and fallback plans all play a role in the safe operation of agentic banking.

The other critical element for agentic banking stewardship is the need to train ALL employees on AI literacy and safety while building AI knowledge requirements into required job skills. Banks need to have a required course around the basics of using and developing agents while providing a set of advanced curricula for bankers that are building and deploying agents.

Bank CEOs also must be proactive in changing their culture to better adapt to agentic banking. Offering upskilling and governance is a good first step, but equally important is for executive management to foster an environment of collaboration and experimentation. A mistake would be to restrict the use of AI so that employees do not have the opportunity to learn about the promise and the dangers of AI. It’s far better to train employees on the safe use of agentic banking and then give them the tools to further learn.

Insight 10: Multi-agents for Agentic Banking

Instead of a single agent performing a task, specialized agents now form “swarms” that coordinate to solve complex, large-scale problems. For example, an AI agent could monitor branch traffic, another could track staff availability, and a third could handle communication in real-time. By having these three agents work together, branch staffing problems can be solved before they become a problem.

Conclusion

Dreamforce 2025 made it clear: the future of enterprise technology is training humans to work with agents and agents to work with humans while creating technology that improves the employee and customer experience. Moving to a mindset that focuses on agents executing tasks across systems, orchestrating flows, and collaborating with humans in real-time will soon be the new normal.

For banking, this shift is especially consequential. The institutions that master data, integrate systems, and build trustworthy agentic experiences will gain a competitive edge in customer experience, cost efficiency, risk management, and innovation. There was much talk around the “agentic divide,” or the pressure that banks that can get their data and infrastructure modernize will outpace those that do not. Banking institutions risk being left behind if they are delayed.