Community Bank Loan Performance Analysis

We conducted a loan performance analysis for over 5,000 individual hedged commercial loans originated by almost 400 community and regional banks across the country. We measured prepayment speeds, loan size, loan term, fee income, loan yield, credit performance, and return on equity (ROE) of hedged loans and compared this performance to community bank industry averages. Our analysis demonstrates that loan-level hedging has offered community banks a strong competitive advantage in the current interest rate environment and competitive landscape.

Universe of Banks

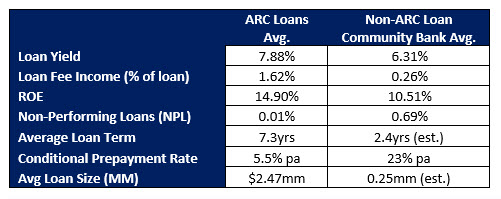

We analyzed the performance of hedged loans at community and regional banks with a total principal outstanding of approximately $12B. We looked at the instrument-level details of these loans and calculated various performance parameters to compare them to industry averages. We also looked at how these hedged loans track community banks’ funding costs. The table below shows a summary of our analysis (community banks are defined as banks under $10Bn in assets).

We note the following important loan performance analysis observations:

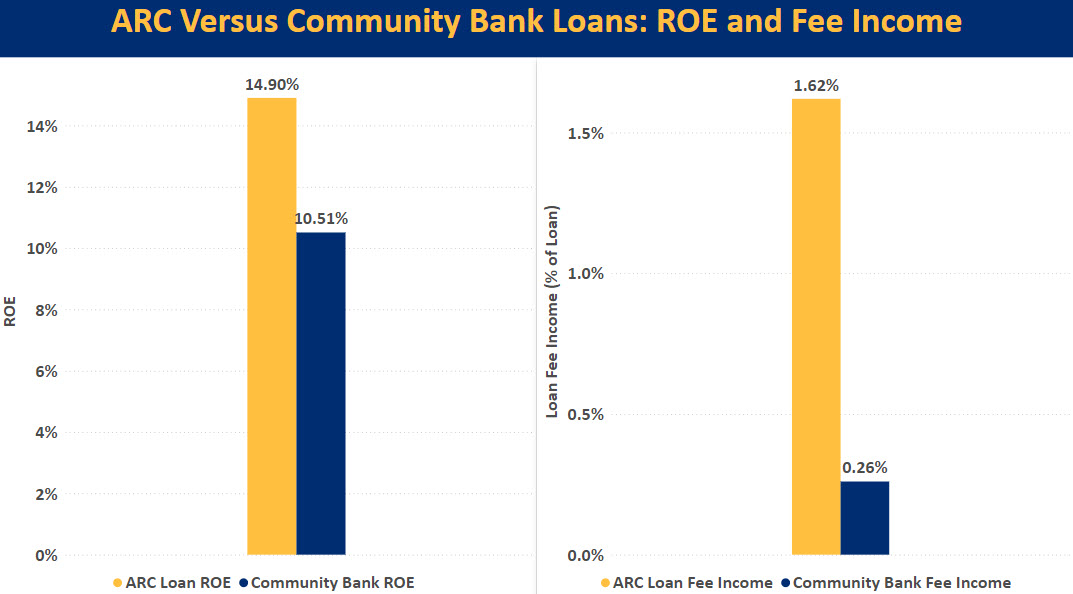

- Because of the inverted yield curve and origination dates of the loans, hedged loans demonstrate yields approximately 1.57% higher than the average community bank loan yields. This is a significant driver of profitability and performance for community banks.

- The average fee generated for hedged loans is 1.62% of the loan amount, which is higher than the average fee income for earning assets at community banks from all products and substantially higher than fees community banks generate on non-hedged commercial loans (a difference of 1.36% of the loan amount). While this hedge fee is a one-time upfront source of income, as with many commercial loans, future amendments, modifications, upsizes, and re-amortization afford banks additional hedge fee generation opportunities.

- The ROE for the average hedged loan is 4.39 percentage points higher than the industry average. This is explained by the higher yield on hedged loans, higher fee income, lower efficiency ratio, better asset quality, longer term, and lower prepayment speeds. Some bankers believe that to win a hedged loan, credit spreads must be lower; however, the average credit spread for hedged loans is 2.43% and ranges from a low of 0.75% to a high of 4.25% (excluding any hedged loans with tax exemption or other structural anomalies).

- Virtually all hedged loans are current. This is a reflection of both current economic strength and self-selection. Banks favor higher credit quality obligors for a hedge program. We also found that during recessions, hedged loans outperform average unhedged loans for similar reasons.

- The average hedged loan term is approximately three times the average term of a non-hedged loan. Longer contractual loan terms increase profitability, cross-sell opportunities (specifically deposits), make relationships stickier, and drive higher lifetime customer value. While the average loan term in the hedge program is 7.3 years, these loans range from a little under 1.5 years to as long as 30 years.

- Conditional Prepayment Rate (CPR) is the portion of a loan or pool of loans that pays principal ahead of the loan’s preset amortization schedule. Small differences in CPR can drive large changes in loan portfolio ROE/ROA. We note that in periods of declining and increasing interest rates, the CPR on hedged loans is substantially lower than non-hedged loans.

- Finally, the average loan size of a hedged loan is almost ten times larger than the average non-hedged commercial loan. This improves the bank’s efficiency and allows better servicing of larger and more profitable relationships.

Additional Observations on Our Loan Performance Analysis

Aside from the loan performance analysis and the numbers, we would like to share some other, more qualitative, reasons why community banks decide to use a loan hedging program.

- Mitigate Interest Rate Risk: Banks’ cost of funding and liquidity can change rapidly, and offering fixed-rate loans beyond a few years, when the average cost of funding is unknown, may be dangerous. A loan hedging program can mitigate that risk.

- Improve Credit Quality: Bankers are aware that any commercial real estate (CRE) borrower repricing in the next two years may be subject to roll-over risk. Certain loan categories may be under credit pressure, and no one can predict where future loan rates may be. Locking a borrower now with a comfortable debt service coverage (DSCR) cushion may be a bank’s safest bet, and a hedging program can both lower the borrower’s rate and bridge the borrower’s credit facility well beyond the risk horizon.

- Protect Existing Loans: Most community banks are not aggressively growing loans, but it is especially painful to lose an existing, large, and profitable relationship. Existing borrowers can be highly profitable clients for community banks. We observe that a significant percentage of community banks are offering hedges to their best existing customers. Community banks approach current borrowers with six to 24 months remaining on their existing credit commitments and offer longer-term fixed-rate hedged loans, sometimes at rates that are lower than the borrower’s existing coupon. Losing a new loan to a competitor may be a positive or negative ROE event for the bank (depending on the winning price/structure), but losing an existing loan to a competitor is almost always a highly negative ROE event for a community bank.

- Instilling Lending Discipline: Community banks face pressure to train lenders, maintain consistent underwriting standards, and instill sensible pricing methodology when the cost of funding continues to be under pressure. One positive aspect of a well-designed loan hedging program is that it highlights the importance of pricing loans to credit, interest rate risk, and the term structure of rates. Lenders who are taught to use hedging programs quickly appreciate the importance of disciplined pricing and prepayment provisions.

- Decrease Loan Prepayment Speeds: One of the most significant determinants of loan profitability is the prepayment rate. More stable loans with longer maturities are more profitable for banks. The number of resources banks expend in sourcing, originating, and underwriting credits makes the initial day the loan is booked the least profitable in the life of that credit. Every periodic interest payment that the borrower makes increases that loan’s value to the bank. The prepayment rates on hedged loans are much lower than the average at community banks (some banks experience CPR greater than 35% per annum, thereby almost guaranteeing negative loan portfolio ROE).

- Generate Fee Income: Net interest margin (NIM) will continue to be under pressure for banks for the near future even if short-term interest rates decrease. Additional hedge fee income is a great way for banks to generate substantial non-interest income and offset contracting NIM.

Why Banks Hedge Now

Some bankers think that they have missed the loan hedging window. Now, with short-term rates expected to decrease, why would banks want to hedge their commercial loans? The answers to this question are as follows: 1) few are able to predict the path of interest rates, not even the Federal Reserve can do so, 2) hedged loans are generally two to 30-year term loans, and interest rates will decline and increase many times over those long periods (all of these changes are unpredictable), therefore, banks use hedging tools to mitigate this risk, 3) when rates decline and increase, the bank’s NIM is stabilized when loans are priced to an adjustable index to match the bank’s cost of funds ( COF) – the industry average correlation between COF and Fed Funds or term SOFR is an R-squared of 0.89 (a very high statistical relationship), 4) the borrower’s longer term fixed payment obligations mitigate the bank’s credit risk by stabilizing DSCR and allow more loan amortization, thereby increasing the borrower’s equity in the project, and 5) the present income in the form of hedge fees is almost always more profitable than future NIM since most loans prepay before the contractual term.

Conclusion

The loan performance analysis is clear – larger loan spreads, greater fees, lower risk and longer terms with ARC Program hedged loans contribute to a 40%+ better ROE. The ROE difference between unhedged loans and hedged is the difference between producing just at your cost of capital or materially above your cost of capital. It is no surprise that more community banks are finding loan hedging programs a valuable tool in not just managing risk but also generating additional income, meeting their loan structuring terms and obtaining their pricing goals. Best of call, for customers that desire payment stablity and don’t want to manage interest or refinancing risk, the ARC Program allows for a better customer experieince.

Loan hedging is not typically a solution for every community bank customer. However, not having a loan hedging solution and not having experienced lenders trained in such a program can be a competitive disadvantage for a community bank. Contact us if you would like to see your bank’s ROE and fee income using a what-if analysis assuming various volumes of hedged loans.