Negative Rates and How to Manage Inflation Risk

In April 2021 we published an article (here) where we argued that the Federal Reserve was overlooking the possibility of serious inflation threats and we questioned the characterization of inflation as transitory. Shortly after that time we published numerous other articles outlining defensive postures that community banks should take in an increasing inflationary environment, from asset management, loan structuring and deposit strategies. At that time the Federal Reserve and various economic models were predicting that inflation would not surpass 2.0%, we wrote that “inflation at 4.0% pa should be the standard and not the stress case.” We also outlined in that article how banks should be underwriting credit and structuring asset duration risk considering higher future inflation and interest rates. Many bankers held a different view and added asset duration in the belief that interest rates would stay low for much longer – some of these bankers have regretted those decisions. In December 2025 we published an article (here) outlining 9 prevailing economic, business, political and demographic forces that persuaded us to expect that the Fed will either be neutral in 2026 with a stronger possibility of a rate hike than a cut. We wrote that “Sticky inflation, rising term premium, fiscal/structural demand, and political credibility risk are clearly present in the data” increasing the possibility of higher inflation and higher interest rates.

So far in 2026 the market expectations have turned in our previously stated direction. However, more recent developments have only strengthened our belief that we are entering a prolonged period of higher inflation and interest rates. We will cover a few recent persuasive developments that bode for higher interest rates for longer periods and in future articles we will outline what steps community banks may take to structure their balance sheets for success.

Price of Oil Contributing to Inflation Risk

The market correctly anticipates that tariffs (especially prolonged negotiations, and continuing imposition and re-imposition of such tariffs) would add to inflation expectations. Deglobalization and immigration restrictions are also viewed as inflationary. But the war in Iran has added another layer to global inflation pressure. While the energy costs are likely to eventually retreat, these developments are sure to trigger structural changes in wages, production costs, and consumer behavior that will be felt for years in the form of higher inflation.

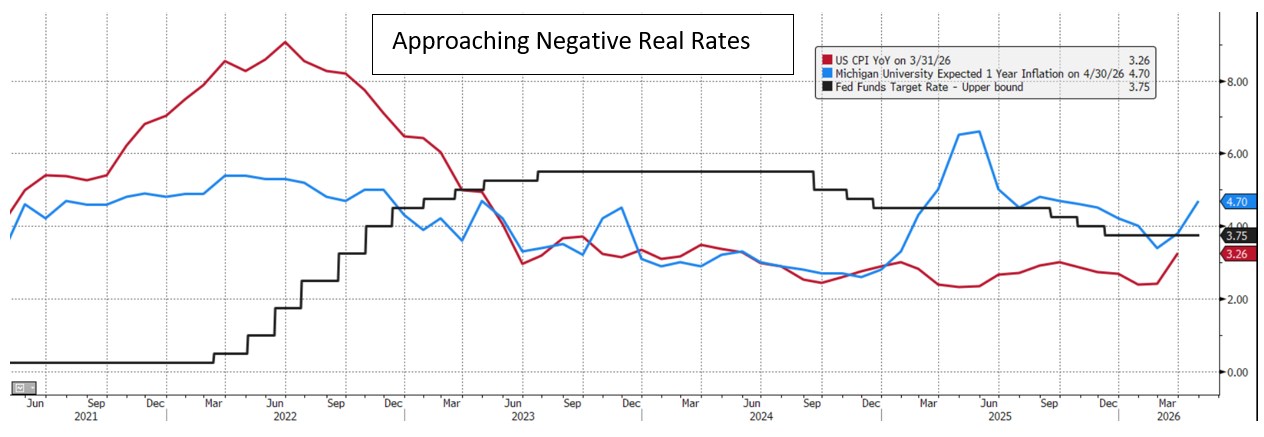

Real Versus Nominal Interest Rates

Real interest rates are already falling without the Fed taking any action. Consider that nominal interest rates are not potent indicators of monetary policy, and instead real interest rates (nominal interest rates adjusted for inflation) are more determinative of monetary policy. As we all recall from recent experience, 5.75% Fed Funds rate is not restrictive when inflation is above 9.0%. So where do real interest rates stand today? Consider the graph below.

This graph shows that inflation – measured as YOY CPI in the red line, and future expected inflation in the blue line are now approaching the Fed Funds target rate in the black line. Keeping short-term rates constant in 2026 will effectively create looser monetary policy because inflation is increasing. This is precisely one reason why in the last Federal Reserve meeting held on April 28-29, 2026, three regional bank presidents favored changing the “bias” of the policy statement from “easing bias” to “holding interest rates steady.” Most current market forces will work to stoke inflation, versus temper it, and this will lead the Federal Reserve into another tightening cycle.

Specious Argument for Lower Interest Rates

One vociferous argument made by some is that because of the high national debt, the US Treasury cannot afford to service the debt with higher interest rates and to lower servicing costs the Federal Reserve will be forced to lower rates. This argument is not without merit, but practically it is incorrect on a few fronts. First, the market will ultimately set the cost of the debt and not the Federal Reserve (which directly controls only short-term rates). Creditors will seek equilibrium pricing of US debt based on perceived risks, and the Federal Reserve cannot use abracadabra to cancel cost of sovereign obligations. In fact, lowering interest rates generally leads to increased inflation expectations, and higher debt premiums. Second, and most importantly, historically the fastest way for governments to shrink debt was to promote inflation. To prevent runaway inflation, interest rates must rise. The vast majority of government interest payments are fixed in nominal terms, and inflation makes the existing debt less burdensome in real terms. The U.S. has used inflation this way before. The average inflation rate from 1946 to 1955 increased to 4.2%, reducing the debt/GDP ratio by almost 40% within a decade. We will discuss this strategy for the current period in future articles.

Conclusion

For the first time since 2023 we have observed community banks increase their appetite for fixed-rate loans in the three-to-five-year repricing bucket. We feel now, as we did in 2021, that this would be an inopportune time for community banks to increase asset duration. There are sound long-term economic, geopolitical and demographic developments that we believe will cause inflation and interest rates to be higher in the next few years. Inflation has not glided to 2.0% and has recently started to climb. What the administration wants and what the Federal Reserve may need to deliver to reach its dual mandate may broadly diverge in 2026 and 2027. Banks would be wise not to repeat mistakes made just a few short years ago by increasing volume and duration of fixed-rate loans.