Our ARC Lending Tactic For Quality Loan Growth

In our article last week (HERE), we discussed how the yield curve is currently flat between the three and 20-year points. This makes term loan pricing between three years and 20 years virtually identical. Banks that cannot offer competitively priced term loans out to 20 years may be at a significant disadvantage when competing or retaining top-quality customers. However, we are at the bottom of an interest rate cycle, and the Federal Reserve is expected to raise rates for the next few years. Booking long-term fixed-rate loans on-balance-sheet may not make sense for many banks. At SouthState, we use a program called ARC (Assumable Rate Conversion) that allows borrowers to pay a fixed rate of interest for as long as 20 years, but the bank retains a floating rate asset. ARC enables community banks to take advantage of a flat yield curve, differentiate the bank from market competitors, provide a higher level of service to better customers, and instill more relationship business – all of this leads to more loans and more profitable customers.

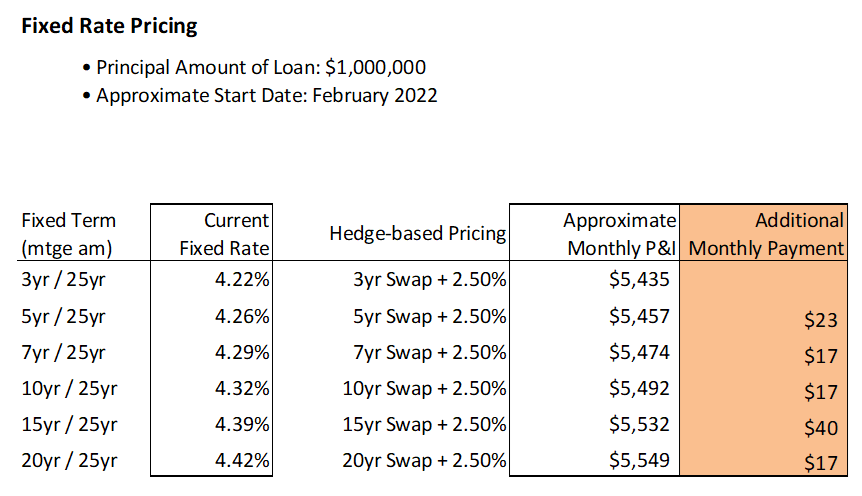

Current ARC Pricing

The table below shows current fixed-rate pricing and P&I payment using a 25-year amortization schedule on a $1mm loan for 3 years out to 20 years. The borrower’s interest rate and the monthly P&I payments (in the highlighted column on the far right) show the small incremental cost of the current term structure.

Current Risk in Term Lending

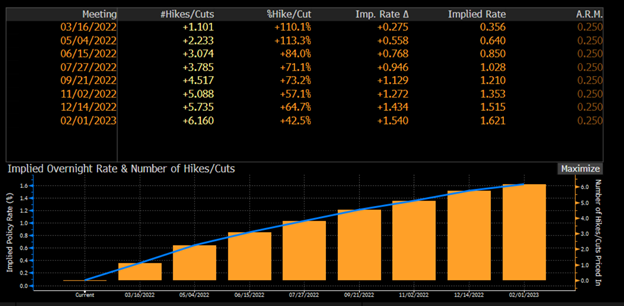

While community banks may want the ability to offer longer-term fixed-rate loans, the interest rate risk is too significant for most banks’ balance sheets. Inflation is at a 40-year high, credit spreads are compressed, cost of funding is the lowest in history, but the Federal Reserve is expected to start raising interest rates this month. The table below shows the implied Fed Funds rate for the next year and the number of expected hikes for each FOMC meeting. The market expects the FOMC to raise short-term rates over six times in the next 12 months and the Fed Funds rate to reach over 1.60% by February of 2023.

Why ARC Makes Sense

Since many community banks do not want interest rate risk on the balance sheet but want to offer borrowers the ability to lock a fixed rate of interest on a term loan, the ARC program provides a timely solution. ARC is custom designed to allow community banks to compete anywhere on the yield curve. The design of the ARC program and the current structure of interest rates allows the following advantages to community banks:

- Differentiate the bank and loan officers from many competitors;

- Provide a higher level of service for customers that have alternative competitors’ options; and

- Create longer, deeper, and more profitable relationships.

The table below summarizes the benefit of the ARC program for borrowers and lenders.

| ARC Program Summary | |||

|

|

Differentiate |

Service | Relationship |

| For Borrower |

Simple four-page addendum, no ISDA documents, no hedge accounting, one fixed-rate billing statement |

The borrower can choose their preferred term of rate stability instead of being dictated by the bank’s balance sheet needs |

Borrower benefits from rate portability as the loan is assumable by other borrowers, and collateral can be substituted (with the bank’s approval) |

| For Bank | With no additional reporting, no additional accounting, and no capital or collateral costs, the bank retains the full relationship | Lenders can create solutions best suited for the borrower instead of being constrained by the bank’s ALCO |

Lenders compete for the borrower’s credit needs less frequently, and the credit is tied to the borrower’s business versus collateral (that is frequently sold) |

|

Value Proposition |

Compete against fewer lenders and offer a superior platform, and charge the borrower accordingly | Sell what the borrower needs instead of what the bank’s balance sheet dictates |

Extend lifetime value of the customer, cross-sell more business, and act as a trusted advisor instead of the lowest cost provider |

Conclusion on ARC

The ARC program may be an excellent solution for better quality customers in the current interest rate environment (a flat curve from 3 years and out, but the Fed is expected to raise short-term rates for the next few years). ARC allows a more sophisticated commercial borrower the option to fix term loans out to 20 years. We find that the program enables us to differentiate our loan offering from most banks, we show customers that we can provide a service that some others cannot offer, and we compete less frequently for that same borrower’s business.