Real-Time Financial Monitoring: A 3x Return

In this market, it is anyone’s guess as to where credit is heading. The recent volatility has dramatically increased credit, interest rate and liquidity risk. To mitigate this potential impact, banks should consider technology enabling the real-time financial monitoring of their customers. In this article, we will make a case for why your bank should prioritize this initiative, what technology to use and how it can help in several areas.

The Challenge

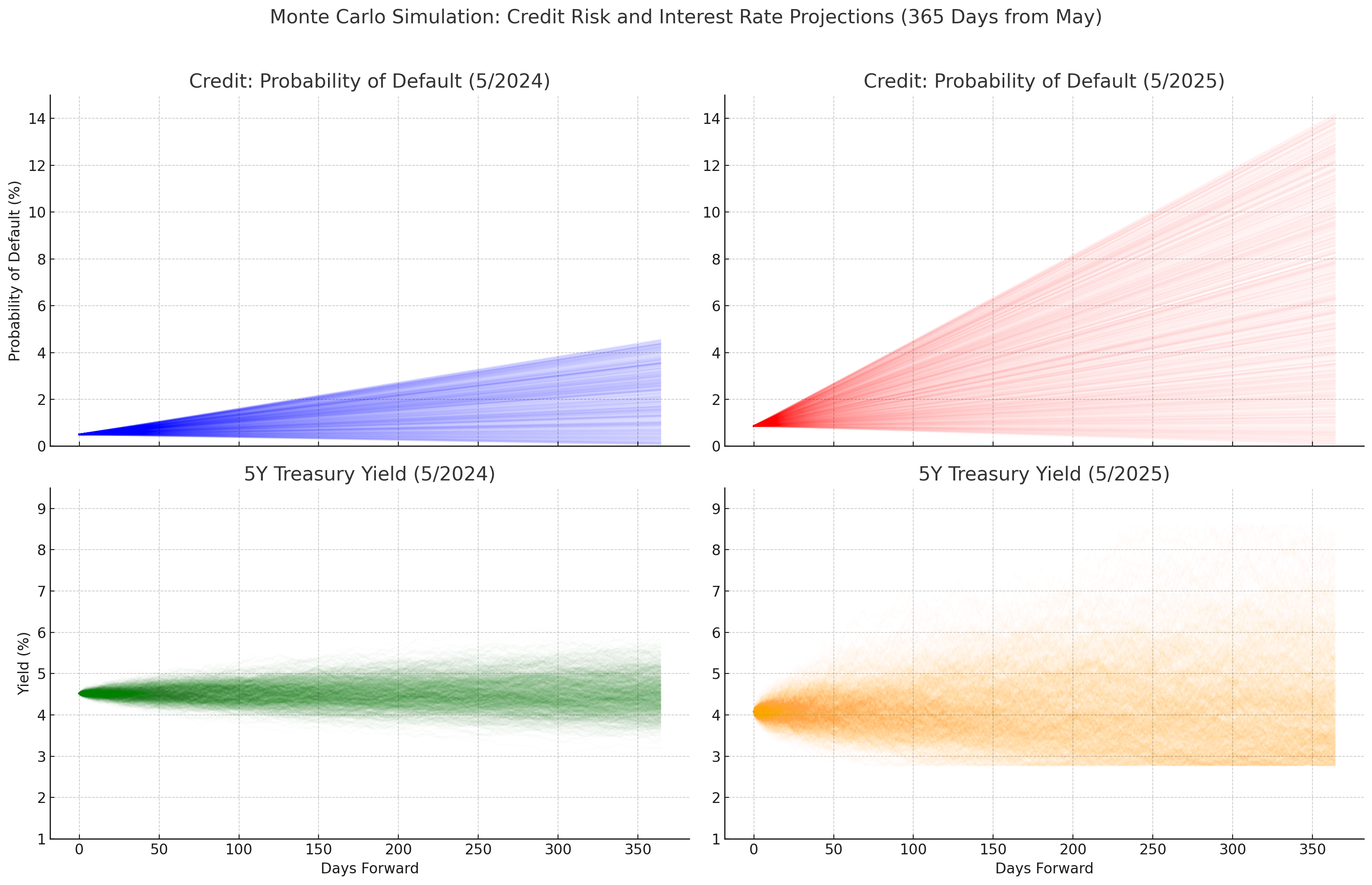

Over the last year, the world has become more volatile. Below are graphs of last year’s projected movement in credit, denoted by the average community bank probability of default, and the potential paths of the five-year Treasury as an indicator of interest rate risk. As can be seen, two standard deviations in now much wider for both credit and interest rate risk. As such, banks have many more scenarios to prepare for and more capital at risk.

When it comes to managing credit risk, one challenge banks have is that they are often looking in the rear-view mirror. We wait for borrower financials that could come 30 days to 18 months in arrears. By this time, it is often too late to restructure or manage troubled debt.

The Solution – Real-Time Financial Monitoring

Backed by five years of cross-regional, empirical evidence drawn from transactional records, compliance audits, and financial institution interviews recent research (HERE), highlights, traditional systems are too slow to detect and respond to risks in real time, leaving institutions vulnerable to surprise default. Static assessments fail to identify liquidity crunches, deteriorating cash flow, or suspicious activity that may emerge days after the last statement date.

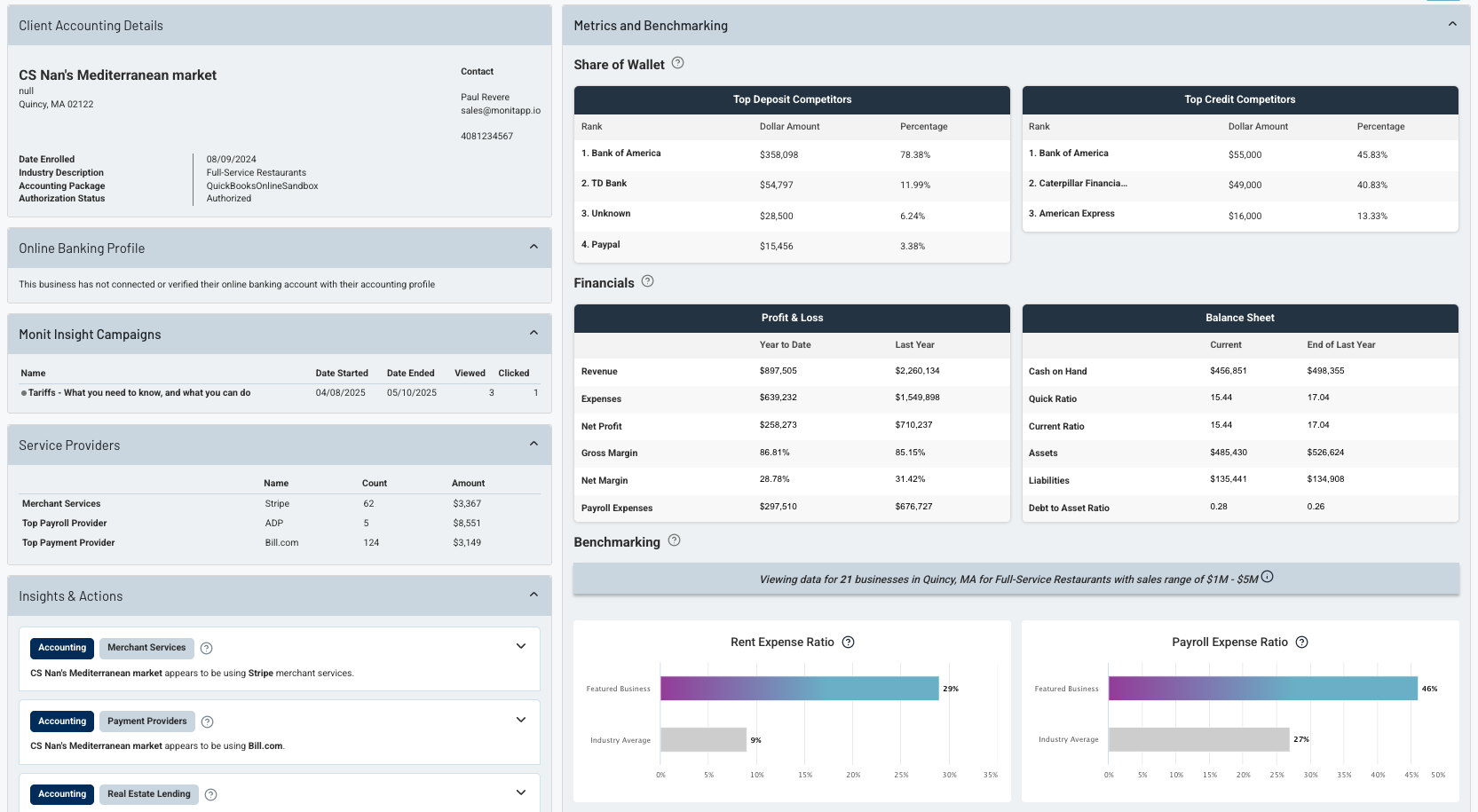

To combat this risk, banks can leverage a handful of vendors, such as Monit and others, to integrate cash flow reporting directly from borrower’s enterprise resource planning (ERP) and accounting systems. Banks can take this data and leverage these vendor’s data warehouse and/or pipe this data into data lakes or CRM systems. Having a real-time connection to clients provides a deep set of rich data to better anticipate the customer’s needs while enhancing the safety of the bank.

According to the study, real-time systems significantly outpace legacy models in both accuracy and speed. These systems use continuous data feeds from borrowers accounting software, transaction histories, and dynamic borrower profiles to maintain a live snapshot of financial health.

From the study, banks using this technology have demonstrated:

- Credit: A 25% gain in credit assessment accuracy, thanks real-time and historical inputs. Real-time financial information enhances the bank’s ability to forecast covenant breaches or deteriorating cash flow up to 90 days BEFORE a breach or delinquency occurs. This means fewer surprise defaults, better portfolio performance, and higher confidence in pricing risk accurately.

- Fraud: Real-time monitoring of transactions and balance flow provides a baseline profile for banks. This helps both detect fraud and create a richer profile to validate non-fraudulent request by reducing false positives. By comparing a borrower’s real-time position, banks can reduce fraud by 35% by continuously flagging anomalies like:

- Spikes in vendor payments,

- Unusual customer refund patterns, and

- Anomalous transaction requests.

Real-Time Cash Flow Forecasting Improves Liquidity Management

One of the most valuable but underutilized tools in the banking risk arsenal is proactive cash flow forecasting. This current economic environment underscores how liquidity often shifts rapidly due to supply chain disruptions, economic dislocations, or market volatility.

Real-time financial monitoring tools pull daily revenue, expense, and receivables data to generate continuously updated cash flow forecasts for both the client and the bank. This allows banks to leverage this technology to:

- Monitor in real-time debt service coverage shortfalls before they become crises,

- Offer timely credit line increases or covenant modifications where appropriate,

- Maintain better capital planning across commercial portfolios.

In addition to reducing defaults by 25%, there is a substantial increase in bank delinquency forecast accuracy allowing banks to make more accurate assessments of delinquency forecasting for shareholders and analysts.

Bridging the Gap Between Banks and Fintechs

This technology also offers another advantage. As the research identifies, fintech firms are outpacing banks in their use of real-time analytics. Real-time integration makes banks more competitive to help better retain customers and lower the cost of customer acquisition.

Real-Time Financial Monitoring is a Compliance Upgrade

Integration with ERP systems also helps with growing regulatory demands for operational resilience and financial transparency. Specifically,

- Automated audit trails and credit regulatory reports,

- Run more accurate stress tests,

- Continuous documentation of risk exposures with low latency, and,

- Faster responses to supervisory inquiries and reporting requirements.

The Economics

The pricing of these integrated systems varies but an average price might be an all-in cost of approximately $90 per customer per year to include amortized integration, API calls and integration time. This provides banks with at least a monthly account view.

It takes a collective minimum of 60 minutes of banker time to request, receive, process and report a set of financials from a single customer. We will put this value at $73 per customer.

Let’s assume that the average loan size for the bank is $500,000 and the term is five years. Let’s also assume that the loan would normally have a 1.25% reserve in this market. Reducing that amount by the 25% the study found is 31 basis point lower credit risk, or $1,563. This equates to an annual credit savings of $313 per annum. Fraud risk is approximately 0.12% for the life of the loan (assuming there is an operating account tied to the loan) which is a savings of $625, or $125 per year.

On a per unit basis, it costs the bank $90 per year to reduce cost and risk by $511 per year per account. That is a 5.68x conservative return.

The Risk – Adoption

The risk for this product is one of execution and operation. The largest risk banks face is a low adoption rate of between 5% and 15% with an estimated 9% average. How do you get more than that? Active marketing and promotions are the answer. To move adoption north of 20%, banks need to offer a 0.05% per annum reduction in interest cost to the borrower to share in the lower risk profile. In our example above, that still leaves the bank with almost a 3x return.

Putting This into Action

In this article, we just focused on managing credit risk. In the future, we will discuss the marketing and sales advantages that this technology brings. Seeing a customer’s real-time financials and transaction activity provides banks with a set of additional data that can generate multiple new product leads and increase cross-sell.

Ultimately, the goal is not just real-time visibility but real-time foresight. By combining real-time data integration with analytics, banks can transform credit risk management from a reactive to a preemptive practice.

With demonstrated fraud reduction of 35%, improved credit accuracy of 25%, and superior forecasting capabilities, the shift from periodic to perpetual oversight is the new gold standard for credit portfolio management.

Vendor Solutions

Below are the top vendors that provide real-time financial monitoring integration that should be considered when choosing a partner to solve this solution. Click the graphic below to compare vendors and learn more within Compass.