Utilizing Agentic AI For Account Opening

Account opening is one of banking’s most important moments: it’s where a new relationship begins, where trust is earned (or lost), and where the bank sets the foundation for profitability and risk management. In this article, we look at how generative AI is being employed within teams of agents that is serving to make the process smoother for the customer, more efficient for the banker and safer for all parties.

The Importance of Account Opening

If there is a single piece of technology to invest in, it’s account opening. In addition to being the gateway of a relationship, strategically it opens digital marketing and operating leverage to a bank. Any bank that has tried to market digitally for a customer only to have to transition that prospect to an analog or clunky digital process, knows firsthand the inefficiencies and leakage that can occur.

Getting the account opening process right is critical to a bank’s success.

Today’s state-of-the-art account opening processes are moving beyond standalone chatbots and simple OCR. Modern platforms are deploying AI agents with each agent being managed by an orchestrator agent and each agent having a specialty. These purpose-built assistants can converse, extract, and validate information, plus route work to humans when confidence is low.

Because of its customer-centric design, open APIs, and AI-first architecture, one of our favorite account opening platforms is Enable. We showcase the technology today to show other bankers where AI might fit into an enterprise account opening and onboarding strategy.

What Agentic AI Really Gets You In The Account-Opening Journey

We wrote a piece last year on the 10 Capabilities Every Account Opening Platform Should Have when AI was starting to emerge for account opening. Now, we are happy to report that financial technology has made progress both with generative AI and with agentic AI.

Account opening products such as Prelim, Enable, nCino, Abrigo, and Mantl/Alkami do a wonderful job at automating data ingestion to make an application fairly seamless for the customer. Leveraging AI, and agentic AI, now takes it to the next level.

Not only does AI make it easier and faster for the customer/bank, but it also makes it safer, and, of new importance, makes for a more flexible system. Any banker that has installed a modern account opening system in the last five years has spent time designing workflow by product and by use case. A single signer retail DDA account would have one workflow, while a CD would have another, another workflow would have to be designed for a commercial account, and another for a 1033 exchange account.

By utilizing a set of AI agents, now banks can quickly adapt to a variety of workflows and handle onboarding much quicker and more effectively than ever before. Onboarding for Treasury Management is no more difficult than onboarding for a stablecoin or for a mortgage. Now, a bank can use a single application for a variety of use cases.

Agentic AI for Account Opening – What Is In Production Today

When it comes to account opening, AI is currently helping in four specific areas:

- Product selection and bundling: helping the customer choose the right checking, savings, card, or credit product—plus add-ons—based on needs and eligibility.

- Identity capture: collecting personal or business identity information accurately and quickly.

- Document collection and verification: requesting the right documents (which varies by product, state, and entity type), verifying they match what was requested, and confirming consistency with the application.

- Exception handling: routing edge cases to bankers or operations teams with a clear summary of what needs attention.

Each area is assigned to an orchestration agent that then analyzes the task and disperses that task to a specialty agent. The composition of the agent team is as follows.

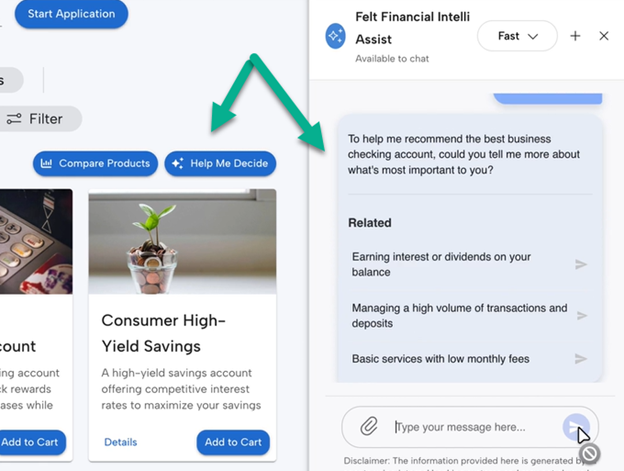

Agent 1: “Help Me Decide”

For many new-to-bank customers, especially small businesses, the hardest part of account opening isn’t the form. It’s understanding which product is the right fit. A needs-based conversation typically requires a seasoned banker who can translate goals (cash flow, payments, savings, borrowing) into the right account structure.

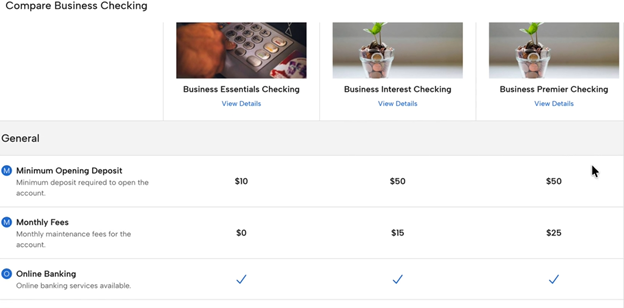

Banks have traditionally achieved this by enabling customers to create a comparison matrix like the example below.

The “Help Me Decide” agent addresses this by engaging the customer, or a banker, in a guided conversation that recommends the right product based on responses to need questions. It works across business and consumer products, across deposits and loans, and can be used in-branch or digitally so the experience is consistent. In Enable’s catalog, as an example, this needs analysis is paired with a conversational agent so that specific questions can be asked and answered in plain English (or any language) and those answers will then prompt the agent team to suggest a product or products. When the customer agrees, key details from the interview are pre-filled thereby saving time and improving accuracy.

What this looks like in practice: A new business owner asks, “I just incorporated, what accounts do I need to separate my business finances, and can I also get a line of credit?” The agent can ask a small set of clarifying questions (expected monthly deposits, cash versus card sales, number of users, international wires, planned borrowing) and then suggest a best-fit package. It is notable in the process that the agent shows clearly the reasoning and trade-offs, so both the customer and the banker feel confident proceeding.

You can go HERE to see a complete demo of this technology in action.

Agent 2: Identity Document Prefill

Online onboarding and account opening applications have gotten fantastic at pulling information from first- and third-party sources, including uploaded documents and prefilling the required fields.

However, this functionality has limits, and a data collection agent goes beyond the basics. An agent can now pull information from email exchanges, articles of incorporation, partnership agreements, board resolutions, and non-integrated data repositories within the bank. Before an agent, a bank application required some integration to a data source to include a data model. Now, an agent makes it easier as it can search files and databases to look for the required customer and meta data (past account use, logins, credit scores, etc.).

Not only does this save time for customers and employees, but this also reduces costs of banks utilizing third-party data pulls, drops abandonment rates while lowering risk due to an additional set of automated validation checks.

You can go HERE to see a complete demo of this technology in action.

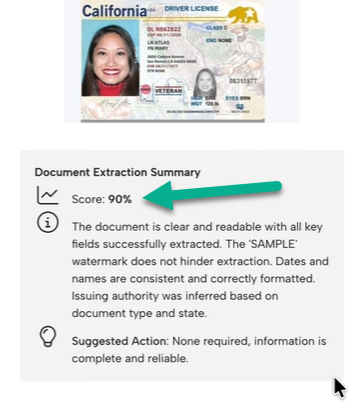

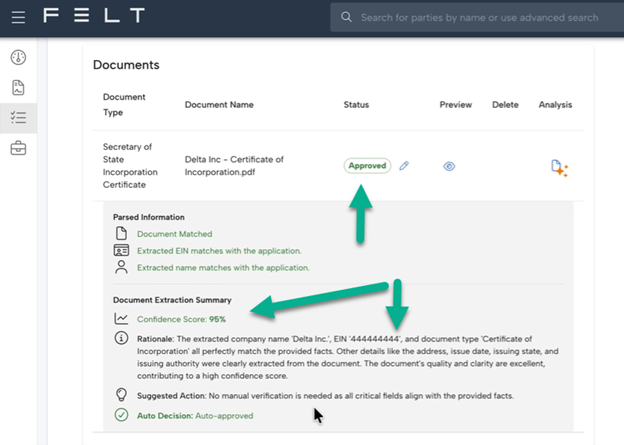

Agent 3: Document Parsing

Business account opening can require a shifting set of documents: EIN letters, certificates of incorporation, beneficial ownership attestations, signer authority documents, and more. Requirements vary by product, customer type, and state—so static checklists often create unnecessary friction (requesting too much) or downstream delays (requesting too little).

A Document Parser Agent dynamically determines the right set of documents to request based on context (such as product type and state). After upload, it reads each document, confirms the document type matches what was requested, and verifies that key fields align with the application. It generates an overall confidence score and, based on that score, either auto-approves the document set or routes the case to an operations officer for review. This approach significantly reduces manual document verification and allows operations teams to scale by focusing on exceptions.

You can go HERE to see a complete demo of this technology in action.

Why confidence scoring matters: Instead of a binary “pass/fail” rule, the agent can express how certain it is and why. That enables banks to set pragmatic thresholds (auto-approve high-confidence matches, review low-confidence cases) and to create a consistent audit trail of what was checked and what triggered escalation.

Using An Agent Ecosystem for Onboarding

As banks mature their onboarding journeys, these three agents often become the foundation for a broader agent ecosystem. For example, Enable also lists agents for business document parsing, financial document parsing (extracting data from tax returns, pay stubs, balance sheets), due diligence summarization (summarizing KYC/KYB checks and surfacing exception areas), and credit decision summarization (condensing credit policy outcomes so staff can focus on what needs attention).

Deploying AI safely: Risk Management

In account opening, “move fast” can’t mean “skip controls.” The most effective deployments treat AI agents as decision support and workflow automation with clear guardrails: show the source data used for prefill, explain mismatches, and keep humans in the loop for exceptions and edge cases. In practice, the goal is not to remove people from onboarding—it’s to reserve human attention for the moments that require judgment.

- Explicit confidence thresholds: define what can be auto approved, what must be reviewed, and what requires re-collection.

- Explainability by design: capture which fields were extracted, which documents were used, and what mismatches were detected.

- Channel consistency: ensure the branch and digital experiences apply the same policies, while allowing banker overrides when appropriate.

- Exception-first operations: route only low-confidence or high-risk cases to operations, along with a summary of what needs attention.

The Takeaway

AI has already reshaped account opening by tackling the three biggest drivers of friction and cost: choosing the right product, capturing identity accurately, and verifying documents efficiently. By using specialized agents such as “Help Me Decide,” Identity Document Prefill, and Document Parser, banks can streamline onboarding for customers and boost their efficiency by focusing only on exceptional cases.

If you are looking to upgrade your current account opening and onboarding workflow, banks MUST now include requirements for the use of agentic AI teams and swarms. Choose a company that is dedicated to adding more agents and more complex agent orchestration and a bank will find that they can use a single onboarding flow to handle every product or service a bank sells. Making the right choice now can dramatically lower your efficiency ratio closer to the 40% goal in the near future.